How do we determine what rate of interest is adequate for an investment instrument? To determine this, we need to know various components and types of interest rates.

Types of Interest rates and components of interest rates:

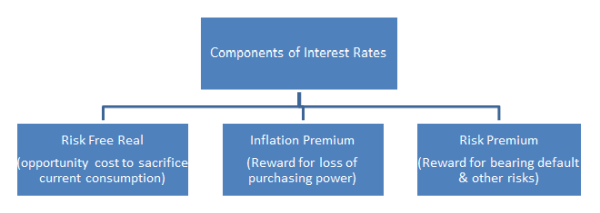

If we break down the interest rate we can get 3 components as below:

Let’s understand the terms in detail one by one:

1) Risk Free Real (Rf Real): This component is for the reward for sacrificing current consumption of the capital. Let’s say you are willing to invest $ 1m, for 2 years which means you will not be able spend this amount for 2 years for which you must be rewarded. The reward that you get for sacrificing current consumption is risk-free real rate of interest (say 3%).

2) Inflation Premium: Continuing with the above example, you will not be able to buy same qty. of any goods/services after 2 years with same amount as the purchasing power of the currency would have reduced because of inflation. The reward that you get for bearing the loss in the purchasing power of the currency is the inflation premium. Higher the inflation rates, higher the inflation premium (say 5%).

3) Risk Premium: Whenever one invests there is a risk that the invested amount may not be repaid (say the company goes bankrupt) which is called default risk. The reward that one gets by taking this risk is termed as risk premium. Risk premium depends on the security cover that is offered; financial ratios of the issuer, etc (say 2%).

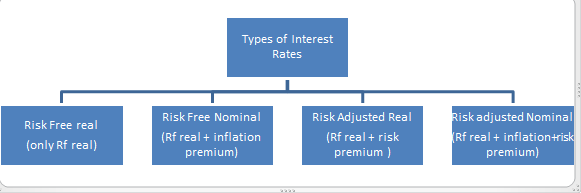

No default risk when the issuer is government (Sovereign Paper). In any of the fixed income securities the total interest would be made up by addition of one or more of the above components depending on who the issuer is and whether it is inflation protected or not and on this basis, 4 types of interest rates can be listed,

Let’s look at applicability of the interest rates in different types of securities:

Risk Free Real (Rf Real,3%): Treasury Inflation Protected Securitiy These are government securities that are inflation protected and as are sovereign paper, default risk is 0. Hence the reward that the investor gets by investing in these securities is only Rf real i.e. 3%. These are annually adjusted for inflation hence no loss of purchasing power. Total return = 3% + inflation adj.

Risk-Adjusted Real (Rf real + risk premium (3%+2%)) Corporate Inflation Protected Security: These are corporate securities that are inflation protected. As these are issued by a corporate, it carries default risk as well. The total reward that an investor gets by investing in these securities is Rf real, risk premium (as it is not a sovereign paper). These securities also are adjusted for the inflation hence no loss of purchasing power. Total return = 5% + inflation adj.

Risk-Free Nominal: (Rf real + inflation premium (3%+5%): Treasury security: These are government securities that are not inflation protected. The total reward that an investor gets by investing in these securities is Rf real and inflation premium, as these are not inflation protected. (risk premium is 0 as no default risk). Total return = 8%.

Risk-Adjusted Nominal (Rf real + inflation premium + risk premium 3%+5%+2%): Corporate security: These are corporate securities say corporate bonds. The total reward that an investor gets by investing in these securities is Rf real, inflation premium (as these are not inflation protected) and risk premium (as there is a risk of default as it is not a sovereign paper). Total return = 10%.

Disclaimer: This document is for general guidance and informational purposes only, and does not constitute professional advice. You should not act upon the information contained in this communication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this communication, and, to the extent permitted by law, author accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this article or for any decision based on it.

The author is a Chartered Accountant and has an exposure of 5 years in the field of Finance, Taxation, Management Consultancy and can also be reached at hariyaniyash8085@gmail.com.

CAclubindia

CAclubindia