Central Registry of Securitisation Asset Reconstruction and Security Interest of India

1. Introduction - The Changing Landscape of Secured Lending

India's banking and financial system has undergone a major transformation over the last two decades. Earlier, lending against property or other assets largely depended on physical documents, internal records, and a significant degree of trust. While this system functioned for years, it also had a serious weakness, there was no centralized mechanism to verify whether the same asset had already been pledged elsewhere.

This gap often led to multiple financing on the same property, disputes among lenders, and avoidable financial losses. To address this challenge and bring transparency into the system, the concept of a central registry was introduced. This led to the establishment of CERSAI in 2011, marking a shift from a trust-based system to a verification-based framework.

2. Understanding CERSAI - The Basic Concept

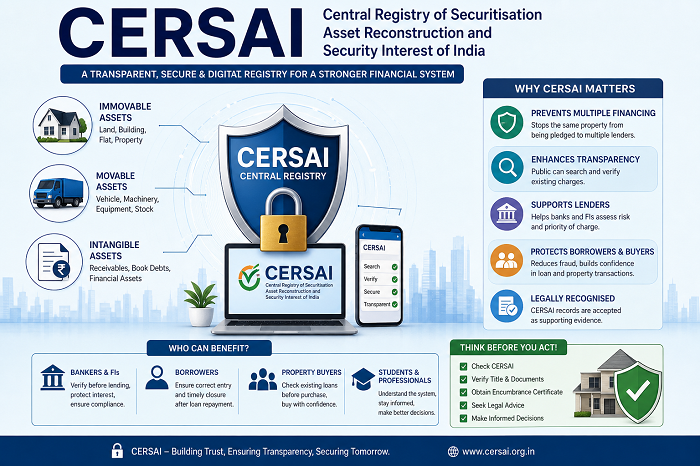

CERSAI stands for the Central Registry of Securitisation Asset Reconstruction and Security Interest of India. In simple terms, it is a centralized electronic database where banks and financial institutions record the security interests created in their favour.

Whenever a borrower takes a loan against an asset such as a house, land, vehicle, or machinery, the lender records that charge in this registry. This creates a public record indicating that the asset is already encumbered.

The concept is similar to a national notice system. Before granting a loan or purchasing a property, any stakeholder can verify whether a charge already exists, thereby reducing the chances of fraud or duplication.

3. Legal Framework and Regulatory Structure

CERSAI operates within the legal framework governing securitisation and enforcement of security interests in India. It functions under the oversight of the Central Government and is supported by regulatory mechanisms applicable to banks and financial institutions.

It is important to note that CERSAI is not a regulator or enforcement authority. It is a registry that records information. The responsibility to create, modify, and close entries lies with the lending institutions.

One of the key compliance requirements is timely registration. Security interests are generally required to be registered within a specified period from their creation. Delays in registration can affect the priority of the lender’s claim and may have implications during recovery proceedings.

4. Scope and Coverage - What Gets Registered

The scope of CERSAI is wide and covers most types of secured lending transactions across India. It includes both movable and immovable assets.

Immovable assets such as land, residential houses, and commercial properties are commonly recorded. In addition, movable assets like vehicles, machinery, equipment, and inventory are also covered. Even intangible assets such as receivables and financial rights may form part of the registry.

This broad coverage ensures that almost every secured transaction is brought under a transparent and searchable system.

5. How CERSAI Works - The Practical Flow

The functioning of CERSAI can be understood through a simple sequence of events:

5.1 Creation of Security Interest: When a loan is sanctioned, the borrower creates a charge in favour of the lender by mortgaging or hypothecating an asset.

5.2 Registration of Charge: The lender records this charge on the CERSAI portal by entering details of the borrower, asset, and loan.

5.3 Generation of Unique Record: A unique identification number is generated, confirming that the asset is registered in the central database.

5.4 Search and Verification: Other lenders or stakeholders can search the registry to verify whether the asset already carries a charge.

5.5 Modification and Closure: Any changes in the loan terms are updated through modification entries, and upon repayment, the lender records satisfaction of charge.

This structured process ensures that the lifecycle of every secured asset is properly documented.

6. Importance of CERSAI in Fraud Prevention

One of the primary objectives of CERSAI is to prevent multiple financing on the same asset. Earlier, borrowers could pledge the same property to different lenders without disclosure, leading to disputes and financial risks.

With the introduction of CERSAI, lenders can verify the status of an asset before sanctioning a loan. This significantly reduces the possibility of fraud and strengthens the overall credit system.

For property buyers as well, it acts as an important safeguard. A simple search can reveal whether the property is under an existing loan, thereby helping buyers make informed decisions.

7. Relevance for Bankers and Financial Institutions

For bankers, CERSAI has become an integral part of the lending process. It is both a compliance requirement and a risk management tool.

Before sanctioning a loan, lenders are expected to conduct a search to verify existing charges. This helps in assessing the borrower’s exposure and ensures that the asset offered as security is free from prior encumbrances.

Timely registration is equally critical. Delays can affect the lender’s priority of charge and weaken its position in recovery scenarios. Proper updating of modifications and closure entries ensures accuracy and reliability of records.

8. Significance for Borrowers

Borrowers often remain unaware that their property or asset is being recorded in a central registry. However, this record has practical implications.

It is advisable for borrowers to verify that the charge has been correctly recorded after availing a loan. More importantly, once the loan is repaid, they should ensure that the lender has filed the satisfaction of charge.

Failure to update the closure can create difficulties in future transactions such as sale of property or obtaining fresh finance. Awareness and timely follow-up can help avoid such issues.

9. Usefulness for Professionals and Students

For professionals such as chartered accountants, advocates, and financial advisors, CERSAI serves as an important due diligence tool. It provides valuable information about the secured status of assets and helps in advising clients effectively.

For students, especially those studying banking, finance, or law, understanding CERSAI is essential. It offers practical insight into how modern lending systems function and how transparency is maintained in financial transactions.

10. Practical Limitations

While CERSAI is a powerful system, it is not a complete solution by itself. It depends on the accuracy and timeliness of data entered by lenders. Incorrect or delayed entries can affect reliability.

Additionally, it does not replace traditional verification methods such as title search, encumbrance certificates, or legal due diligence. It should always be used as a supplementary tool rather than the sole basis for decision-making.

11. Conclusion

CERSAI has significantly strengthened India's secured lending ecosystem by introducing transparency, accountability, and discipline. It has reduced the risk of fraud, improved credit assessment, and created a reliable system for verifying security interests.

For bankers, it is an essential compliance and risk management tool. For borrowers, it is a record that must be monitored. For professionals and students, it is a valuable learning and advisory resource.

The shift from trust to verification is one of the most important developments in modern banking, and CERSAI stands at the centre of this transformation.

Disclaimer: This article is intended solely for general educational and awareness purposes. It does not constitute legal, financial, or professional advice. The information presented is based on general understanding and may be subject to change in line with amendments in laws, rules, or regulatory guidelines. Readers are advised to consult qualified professionals before taking any decisions based on this information.

Message to Readers: In today's financial environment, informed decisions are the key to safety. Whether you are lending, borrowing, advising, or investing, always verify the facts before proceeding. Awareness of systems like CERSAI is not just useful—it is essential.

(In today’s financial environment, verification is more important than trust. Always check before you act.)

The author is a seasoned professional with over four decades of experience in banking, law, and financial advisory. He is an Advocate, Insolvency Professional, and Former Banker with expertise in credit, recovery, and financial regulations. Through his platform, Kakkar Wisdom Hub, he focuses on simplifying complex legal and banking concepts for professionals, students, and the general public.

CAclubindia

CAclubindia