What are Auditing Standards?

The Standards on Auditing is an area which requires greater focus of CA in practice as well as our administrative bodies who are updating our members. The Companies Act 2013 has discussed it in detail which was absent in erstwhile act.

As per Sec 2 (7) “auditing standards” means the standards of auditing or any addendum thereto for companies or class of companies referred to in sub-section (10) of section 143.

Sec 143 (9) reads “Every auditor shall comply with the auditing standards.”

As per Sec 143 (10) The Central Government may prescribe the standards of auditing or any addendum thereto, as recommended by the Institute of Chartered Accountants of India, constituted under section 3 of the Chartered Accountants Act, 1949, in consultation with and after examination of the recommendations made by the National Financial Reporting Authority:

Provided that until any auditing standards are notified, any standard or standards of auditing specified by the Institute of Chartered Accountants of India shall be deemed to be the auditing standards.

Sec 147 (2) If an auditor of a company contravenes any of the provisions of section 139, section 143, section 144 or section 145, the auditor shall be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees:

Provided that if an auditor has contravened such provisions knowingly or wilfully with the intention to deceive the company or its shareholders or creditors or tax authorities, he shall be punishable with imprisonment for a term which may extend to one year and with fine which shall not be less than one lakh rupees but which may extend to twenty-five lakh rupees.

Sec 147 (3) Where an auditor has been convicted under sub-section (2), he shall be liable to—

1. refund the remuneration received by him to the company; and

2. pay for damages to the company, statutory bodies or authorities or to any other persons for loss arising out of incorrect or misleading statements of particulars made in his audit report.

The Sec 143 (9), (10) read with Sec 147 of the act clearly describes the importance of Standards on Auditing but many practicing CA has not dealt with it in detail and in most of the cases across mid-sized firm it has been noticed that Audit report are being drafted by articles and in small clients by the client itself. There are gap in documentations as required by Standards on Auditing.

In the Independent Auditors Report issued by the auditor, all the CA colleagues state that we have complied with Standards on Audit but many of us are not even aware the number of standards which are issued by our supreme body by which we had to comply earlier also and now mandated by the Companies Act 2013.

To clear the air there are 43 standards in all and one Standard on Quality Control which is SQC 1 for the Firm providing Assurance Service. These standards are based on International Standards on auditing and are divided in following Series and broad Categories.

|

Series

|

Category

|

Number

|

|

200-299

|

General Principles and Responsibility

|

9

|

|

300-499

|

Risk Assessment and Response to the Risk

|

6

|

|

500-599

|

Audit Evidence

|

11

|

|

600-699

|

Using work of Others

|

3

|

|

700-799

|

Audit Conclusion & Report

|

5

|

|

800-899

|

Specialised Areas

|

3

|

|

SRE

|

Standard in Review Engagement

|

2

|

|

SRA

|

Standard in Assurance Engagement

|

2

|

|

SRS

|

Standard in Related Services

|

2

|

There are many question which is enquired about how to comply with these standards in case of Small Entity but Companies Act 2013 does not differentiate between small entities and big entities.

The Audit Procedure to be followed should be as shown below diagrammatically.

Mapping of Process

We should know the process in which company is working, we would not be able to comment on Internal Financial Control of the company if we don’t map the process by flow chart with major areas being.

-

Sales

-

Purchase

-

Banking

-

Cash Management

-

Human Resource

Test of Control

Test of Control (TOC) is a walk through from point of initiation to point of completion of the samples selected on basis of statistical sampling as explained in standards on auditing. TOC has to been done for areas such as Purchase, Sales, Fixed Assets, HR etc, whereby we identify the weakness in control and thereby it helps to understand the extend of sample to be selected for substantial compliance.

Test of Details

Test of Details has been done for top 100 Expenses whereby the sample has been selected on materiality basis as defined in standards on auditing.

We should document whatever we do, AS 230 discusses in detail the audit documentation and few examples are as follows

-

Audit Program – Before visiting client

-

Analyses- Before visiting client

-

Issue Memorandum-Issues noted at client place

-

Summary of Significant matters – Summary of unadjusted entries

-

Letter of Confirmation and representation

-

Checklist – CARO, Schedule III, Inventory Count, Standards on Auditing, Last invoice number

-

Correspondence and minutes of meeting

Advantages of Documentation

- Assist in Planning & Performing Audit

- Enabling Review of Senior Managers and Partners

- Control of Rectification entries past by client

- Quality Control Reviewer Partner to review

- Proper takeover of work from person leaving the assignment

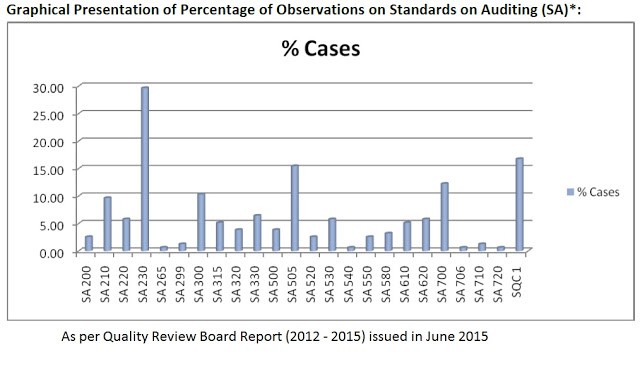

Action initiated by Quality Review Board

As per report published by Quality Review Board (QRB) on 31st July 2015, the QRB had done 216 reviews between August 2012 - June 2015, a total of 175 review reports reviewing audits of top listed entities in India were finalized by the Board, 25 cases were recommended to the ICAI Council for consideration and in 74 cases appropriate advisories were issued to the concerned audit firms for improvement in future.

So, a total of 99 reviews out of 175 i.e., about 57% reviews indicated need for improvement in diverse areas.

In the said report, a summary of some of the observations noticed by the Technical Reviewers in respect of 155 reviews completed by QRB till 31 March, 2015 were provided and it is stated that number of issues were common to more than one of these audits mainly in the areas of

(a) compliance with accounting standards;

(b) compliance with standards on auditing mainly relating to, agreeing the terms of audit engagement, audit documentation, materiality in planning and performing an audit, audit evidences, communication with those charged with governance, responsibility of joint auditors, planning an audit of financial statements, identifying and assessing the risk of material misstatement through understanding the entity and its environment, auditor’s response to assessed risks, audit sampling, written representation letter, external confirmations, using work of another auditor, forming an opinion and reporting on financial statements;

(c) compliance with the Revised Schedule VI of the Companies Act, 1956 in relation to proper presentation of the financial statements and disclosure of amounts under respective heads in the balance sheet;

(d) compliance with relevant laws and regulations; and

(e) quality control. In most of such cases, the audit firms have represented that they will take actions to address such deficiencies in future.

For detail report refer http://www.qrbca.in .

Therefore in my personal view, audit is no more an ancillary service, it requires special attention and it’s the time we wake up and accept the change and start the journey of “learning, unlearning and relearning.”

The author can also be reached at vivek@cavivek.in

CAclubindia

CAclubindia