Part I - Law(s) Governing the eForm

EForm MSME FORM-I is required to be filed pursuant to Order dated 22 January, 2019 issued under Section 405 of the Companies Act, 2013 and which are reproduced for your reference:

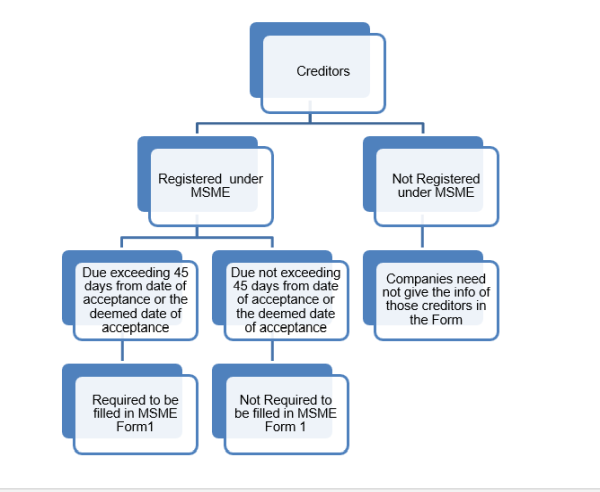

1. Specified Companies (Furnishing of information about payment to micro and small enterprise suppliers) Order, 2019, all companies, who get supplies of goods or services from micro and small enterprises and whose payments to micro and small enterprise suppliers exceed forty five days from the date of acceptance or the date of deemed acceptance of the goods or services as per the provisions of section 9 of the Micro, Small and Medium Enterprises Development Act, 2006 (27 of 2006) (hereafter referred to as “Specified Companies”), shall submit a half yearly return to the Ministry of Corporate Affairs stating the following:

a. the amount of payment due and

b. the reasons of the delay;

2. Every specified company shall file in MSME Form I details of all outstanding dues to Micro or small enterprises suppliers existing on the date of notification of this order within thirty days from the date of publication of this notification.

3. Every specified company shall file a return as per MSME Form I annexed to this Order, by 31st October for the period from April to September and by 30th April for the period from October to March.

Part II - Purpose to file the eForm

All Companies, who get supplies of goods or services from micro and small enterprises and whose payments to micro and small enterprise suppliers exceed forty-five days from the date of acceptance or the date of deemed acceptance of the goods or services as per the provisions of section 9 of the Micro, Small and Medium Enterprises Development Act, 2006 shall submit a return to the Ministry of Corporate Affairs in the interval mentioned below

a. Initial return (For Amounts due for more than 45 days to the creditors as on 22.01.2019 )

b. Regular half yearly return ( For Amounts due for more than 45 days to the creditors as on 31.03.2019)

Understanding the Terms: -

- Date of Acceptance: - It is the date when the goods or the services are accepted by the company from its suppliers.

- Deemed date of Acceptance: - In case any dispute arises after the goods or services are received by the company, then the date when the dispute is resolved will be the deemed date of acceptance.

Part III - Steps to be taken by the companies

1. All the companies shall confirm from their creditors whether any of them are having the registration under the MSME Development act,2006.

2. It is to be noted that only Micro and Small enterprise Creditors are covered with in the provision and Medium enterprise creditors are not covered herewith.

3. In case if their creditors are not having MSME Registrations then the said companies are not required to file this form.

4. In the other case i.e. if any of their creditors are having the MSME Registrations then the companies have to extract those creditors list who are due to be paid exceeding 45 days from the date of acceptance and are still due as on 22.01.2019.

5. If in case any objection is raised within 15 days of acceptance of goods and services then the deemed date of acceptance of goods or services will be from the date from which the dispute is resolved between the company and the vendors.

6. Due Date to fill this Form: - Presently the revised due date to file the Initial return is 30.05.2019.

Attachment:

a. Notification of the above is available here: http://www.mca.gov.in/Ministry/pdf/MSMESpecifiedCompanies_22012019.pdf

b. MSME help kit by MCA is available for download in the MCA Website.

Source: MCA MSME Help Kit

CAclubindia

CAclubindia