SHORT SUMMARY

The MSME Form 1 is a half-yearly compliance requirement under Section 405 of the Companies Act, 2013, introduced to monitor and ensure timely payments to Micro and Small Enterprises. Companies having outstanding dues exceeding 45 days to registered MSME suppliers are mandatorily required to file this form, as per the MCA notification issued in 2019. This initiative aligns with the provisions of the MSMED Act, 2006 and aims to safeguard the liquidity and sustainability of small businesses

Purpose of MSME 1 Form

To ensure transparency and timely payments to Micro and Small Enterprises (not Medium), in line with the MSME Development Act, 2006 which mandates payment within 45 days of acceptance of goods/services.If payments are delayed beyond this period, the form serves as a declaration of such dues.

Legal Provisions

Section 405 of the Companies Act, 2013

This is the primary section that empowers the Central Government to direct companies to furnish information or statistics.

Section 405(1): "The Central Government may, by order, direct any company or class of companies to furnish such information or statistics as may be specified in the order within such time and in such form and manner as may be specified therein."

MSME Form 1 is notified under this section via the Companies (Furnishing of Information about payment to micro and small enterprise suppliers) Order, 2019 dated January 22, 2019.

Related Provisions from the MSME Development Act, 2006

Although the Companies Act does not directly define MSMEs or their payment timelines, the MSME Act, 2006 supplements the framework.

Section 15 of the MSMED Act, 2006 - Obligation to Make Payment

A buyer must make payment to the supplier within 45 days from the date of acceptance or deemed acceptance of goods/services.

Section 16 of the MSMED Act - Interest on Delayed Payment

If a buyer fails to make payment within 45 days, they are liable to pay compound interest with monthly rests at three times the bank rate notified by the RBI.

A. WHO IS REQUIRED TO FILE MSME FORM 1?

Any company (public or private), regardless of its size or nature, is required to file MSME Form 1 if it meets both of the following conditions:

1. The company has received goods or services from suppliers who are registered as Micro or Small Enterprises (MSEs) under the MSMED Act, 2006; and

2. The payment to such MSME suppliers is outstanding for more than 45 days from the date of acceptance or deemed acceptance of such goods or services.

3. The payment made to MSME suppliers after 45 days from the date of acceptance or deemed acceptance of such goods or services during the half year.

Who is Not Required to File?

- Companies that have no dealings with Micro or Small Enterprises.

- Companies that have made all payments to MSMEs within 45 days.

- Medium Enterprises are not covered under this reporting requirement - only Micro and Small enterprises.

Note: Changes in MSME 1 form due to transfer of form from V2 version to V3 person:

Requirement of Filing as per V2 Version

Previously, when Form MSME-1 was available on the V2 portal of the MCA, companies submitting this form were mandated to provide details of outstanding payments at the end of the half-year, specifically for vendors registered as micro and small enterprises, which remained unpaid for more than 45 days from the date of receipt of goods or services. Consequently, all companies that made payments to vendors after 45 days of receiving goods or services, but before the conclusion of each half-year, were exempt from filing this form, as there would be no outstanding dues to vendors classified as micro or small enterprises at the end of the half-year.

Additions to revised form MSME-1 in V3 portal

The new V3 version of Form MSME-1 asks for below additional details regarding payments to vendors registered as micro and small enterprises: -

1. Micro and Small vendors to whom payment has been done during the half year and within 45 days

2. Micro and Small vendors to whom payment has been done during the half year but after a period of 45 days

3. Micro and small vendors whose payment is outstanding as of the end of half year, but 45 days are not yet over (o/s for less than 45 days)

4. Micro and small vendors whose payment is outstanding as of end of half year, and 45 days are over (o/s for more than 45 days)

As v2 version asked for information of transaction which paid after 45 days or pending more than 45 days at end of half year i.e. mentioned at point no 2 and 4. But MCA has added new point no 2 and 3 in the form without modification of the provisions/ section/ circular.

B. TIME PERIOD

Every company on which this form applicable shall file MSME-1 with ROC every half year.

i. April to September, Due Date is 31st October

ii. October to March, Due Date is 30th March

C. FEES FOR MSME-1

There are no ROC fees for filing of this form. This form shall be file free of cost. Even if any company file this form after due date there is no additional fees prescribed for this form. Even after due date there is no consequences of additional fees, However, there are consequences of Penalty under Compounding.

I. If payment is made to an MSME vendor within 45 days during the half-year period or payment is pending at the end of half year but 45 days is not completed is MSME Form 1 still required?

Answer: No, MSME Form 1 is NOT required to be filed in such cases as per the above-mentioned provisions:

Explanation:

As per the Companies (Furnishing of Information about payment to micro and small enterprise suppliers) Order, 2019, issued under Section 405 of the Companies Act, 2013, the requirement to file MSME Form 1 arises only if:

- The company has outstanding payments exceeding 45 days (from the date of acceptance or deemed acceptance),

- To Micro or Small Enterprises, and

- Such dues are unpaid as on the reporting date (i.e., 31st March or 30th September).

Note: However, as mentioned above about V3 form these days in V3 excel sheet form is asking to file form in the case company has made payment within 45 days or payment outstanding less than 45 days. MCA should give some clarification on the same. As the form is over riding the Circular/ provisions.

II. If there is an outstanding due to a vendor registered as a Medium Enterprise, is filing of MSME Form 1 required?

Answer: No, MSME Form 1 is NOT required to be filed in such case.

Explanation:

The MSME Form 1 filing requirement is applicable only in respect of dues payable to suppliers who are:

- Micro Enterprises, or

- Small Enterprises,

and not to Medium Enterprises.

This is clearly reflected in the language of the MCA Notification dated 22nd January 2019 (Companies (Furnishing of Information about payment to micro and small enterprise suppliers) Order, 2019), which states:

"Every specified company shall file a return in MSME Form 1 providing details of all outstanding dues to Micro or Small enterprises suppliers..."

III. Is MSME Form 1 required if there were transactions with MSME vendors during the half-year, but no outstanding dues at the end of the half-year?

Answer: No, MSME Form 1 is NOT required to be filed in such case.

Explanation:

The requirement to file MSME Form 1 arises only when the following two conditions are simultaneously satisfied:

1. The company has procured goods or services from Micro or Small Enterprises (registered under MSMED Act), and

2. Payment is outstanding for more than 45 days from the date of acceptance or deemed acceptance, as on the last day of the reporting period(i.e., 31st March or 30th September).

Note: But due to changing version of MSME 1 on V3. In case of NIL outstanding at end of half year and all payment made within 45 days during the half year still it is required to file MSME 1.

IV. If a company itself is registered as an MSME (Micro or Small), is it required to file MSME Form 1?

Answer: Yes, it may be required to file MSME Form 1 - but only if it meets the criteria mentioned above in this article as a buyer, not as a supplier.

D. CONSEQUENCES OF NON-FILING

i. Consequence - Additional Fees: As e-form MSME-1 doesn't having any fees. It's file with ROC with NIL fees. Further, CG has not prescribed any additional fees on MSME-1. Therefore, even if company has filed its MSME-1 after the due date it is not required to pay any additional fees.

ii. Consequence - Penalty: As Section 450 prescribed penalty in case of default of section 405 of Companies Act, 2013.

Penalty on Company

A penalty of ten thousand rupees, and in case of continuing contravention, with a further penalty of one thousand rupees for each day after the first during which the contravention continues, subject to a maximum of two lakh rupees in case of a company

Penalty to Director:

Fifty thousand rupees in case of an officer who is in default or any other person

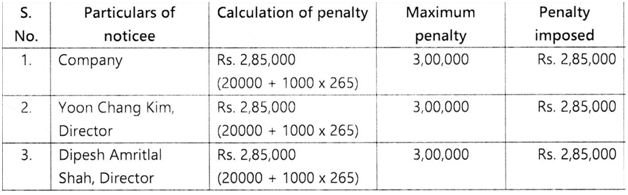

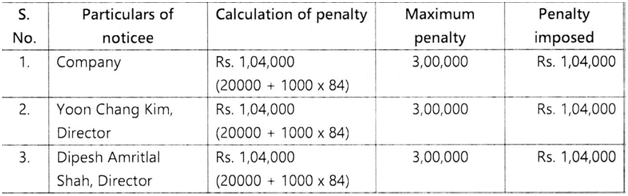

ADJUDICATION ORDER IN THE MATTER OF SAMSUNG R&D INSTITUTE-INDIA-BANGALORE PRIVATE LIMITED

I. FACTS OF THE CASE

a. The company was required to file MSME-1 for the period April 2022 to September 2022 by October 31, 2022, and October 2022 to March 2023 by April 30, 2023, with ROC.

b. On July 25, 2023, the company filed both durations MSME-1 by making a default of 266 days and 85 days respectively.

c. Non-compliances of section 405 are calculated from November 01, 2022, to July 25, 2023 and May 01, 2023 to July 25, 2023 respectively for both delayed return filed.

II. ORDER

Having considered the facts and circumstances of the case, and after taking into account the factors above, I hereby impose a penalty as under:

Default Instance I: November 01, 2022, to July 25, 2023 - Delay of 266 days.

Default Instance II: May 01, 2023 to July 25, 2023-Delay of 85 days

Quick Bites

1. If a company made payment to MSME vendors beyond 45 days, but the dues are not outstanding as of 31st March or 30th September, is MSME Form 1 filing required?

Answer: No, MSME Form 1 is NOT required to be filed in this case as per provision of the Law

|

Scenario |

MSME Form 1 Required? |

|

Payment was made after 45 days, but before 31st March / 30th Sept |

No |

|

Payment is still outstanding as on 31st March / 30th Sept and delay > 45 days |

Yes |

|

Payment made within 45 days (irrespective of date) |

No |

Conclusion

Issuing preference shares through rights issue under Section 62(1)(a) read with Section 55 of the Companies Act, 2013, offers companies a strategic means to raise capital while maintaining shareholder equity participation. Though commonly associated with equity shares, rights issue provisions are equally applicable to preference shares, provided the Articles permit such issuance and all prescribed conditions are met.

From a compliance standpoint, it is essential for companies to adhere to the procedural requirements, including clear disclosure of terms, proportionate allotment, proper documentation, and timely statutory filings. This method avoids the complexities of private placement while ensuring transparent and equitable capital restructuring.

CAclubindia

CAclubindia