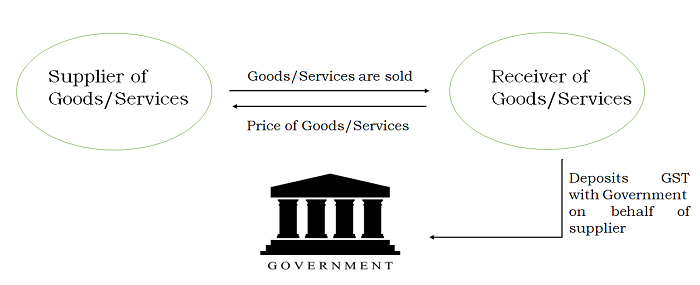

Normal GST Payment Process

BACKGROUND OF REVERSE CHARGE MECHANISM

- Reverse Charge Mechanism was first introduced in the Service Tax Law.

- Now, the Government has incorporated RCM in GST.

- The government has notified not only the supply of certain services but also the supply of certain goods under RCM.

OBJECTIVE OF THE REVERSE CHARGE MECHANISM

- Safeguard the interest of Revenue

- Administrative convenience of the Government

GST Payment in case of Reverse Charge

Statutory Provision

Section 2(98) of the CGST Act, 2017

"reverse charge" means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under sub-section (3) or sub-section (4) of Section 9, or under sub-section (3) or sub-section (4) of Section 5 of the Integrated Goods and Services Tax Act.

Section 9(3) of the CGST Act, 2017

The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

Section 5(3) of the IGST Act, 2017

The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

Comprehend the two types of reverse charge scenarios in GST

|

|

To read the full article: Click Here

CAclubindia

CAclubindia