I. Brief Background:-

The government had introduced "Income Declaration Scheme, 2016" which came into force from 1st June, 2016 and ended on 30th September'2016. The scheme provided for an opportunity to persons who have not paid taxes in the past in respect of undisclosed income, to come forward and declare such undisclosed income and pay tax, surcharge and penalty totalling in all to 45% of such undisclosed income so declared.

Though the scheme has gathered fairly good response, however one provision under the scheme namely Section 197(c) of the Finance Act'2016 has raised significant ambiguity and controversy so far as to whether the Income Declaration Scheme in itself supersedes the law of limitation applicable under the Income Tax Act u/s 142/143(2)/148/153A/153C.

The current Union Budget 2017-18 announced on 1st February' 2017 by the Hon'ble Finance Minister, Sh. Arun Jaitley resolved the ambiguity and controversy so raised by the Section 197(c) of the Finance Act' 2016 to a great extent which is elaborated in the shape of this article.

II. Implications of not declaring the undisclosed under the erstwhile Income Declaration Scheme'2016

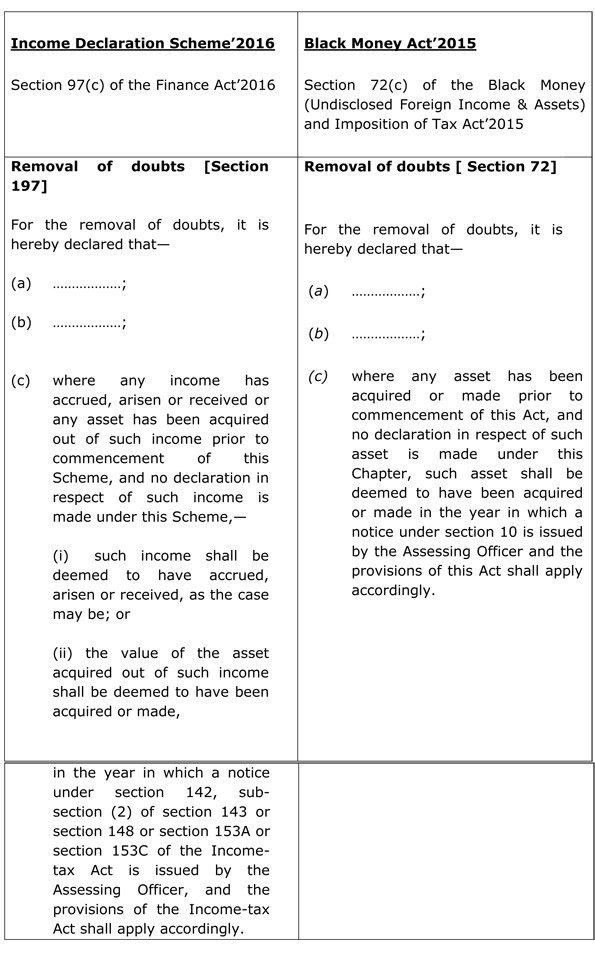

Relevant Statutory Provisions as contained in Chapter IX of the Finance Act' 2016 [Section 197(c)]

"Removal of doubts.

197. For the removal of doubts, it is hereby declared that -

(a) …………………..

(b) …………………..

(c) where any income has accrued, arisen or received or any asset has been acquired out of such income prior to commencement of this Scheme, and no declaration in respect of such income is made under this Scheme,-

(i) such income shall be deemed to have accrued, arisen or received, as the case may be; or

(ii) the value of the asset acquired out of such income shall be deemed to have been acquired or made, in the year in which a notice under section 142, sub-section (2) of section 143 or section 148 or section 153A or section 153C of the Income-tax Act is issued by the Assessing Officer, and the provisions of the Income-tax Act shall apply accordingly."

Analysis:-

In case no declaration is made in respect of the undisclosed income relating to earlier years prior to commencement of the scheme, Clause (c) of section 197 of the Finance Act, 2016 introduced a deeming fiction. It stated that where any undisclosed income [which has accrued or arisen or received prior to commencement of this scheme] and no declaration in respect of such income is made, such income shall be deemed to have accrued or arisen or received in the year in which a notice under section 142/143(2)/148/153A/153C is issued by the Assessing Officer, and the provisions of the Income Tax Act'1961 shall apply accordingly.

A bare perusal of the Section 197(c) of the Finance Act' 2016 suggests that a person should make declaration of all the undisclosed income generated or undisclosed assets acquired in any year prior to commencement of the scheme even if such year is a year which is beyond the limitation period. This is due to the fact that Section 197(c) provides that in case no declaration in respect of undisclosed income relating to earlier years is made under the scheme, such undisclosed income shall be deemed to be the income of the year in which a notice u/s 142 or u/s 143(2) or u/s 148 / 153A / 153C of the Income Tax Act is

issued by the Assessing Officer.

It is pertinent to mention here is that the wording under Section 197(c) of the Finance Act' 2016 is on the similar lines with that of Section 72 (c) of the Black Money (Undisclosed Foreign Income & Assets) and Imposition of Tax Act' 2015. The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 was brought under the statute books to report the undisclosed offshore assets.

The language under both the section of the respective acts is tabulated herein under:-

As can be seen from above, under both the laws, the intention of the legislature was amply clear to overrule the law of limitation and thereby the timeline for reopening of the earlier year and bring the undisclosed income of earlier years to the tax net. However one must note that both the Sections under different statutes, play differently.

Section 72(c) of the Black Money (Undisclosed Foreign Income & Assets) and Imposition of Tax Act' 2015 provides that if no declaration has been made prior to the commencement of the Act in respect undisclosed foreign assets, such asset shall be deemed to have been acquired or made in the year in which a notice under section 10 is issued by the Assessing Officer and the provisions of this Act shall apply accordingly.

Now Let us go through the Provisions of Section 10 of Black Money (Undisclosed Foreign Income & Assets) and Imposition of Tax Act' 2015, which are reproduced herein under:-

"Assessment

10. (1) For the purposes of making an assessment or reassessment under this Act, the Assessing Officer may, on receipt of an information from an income-tax authority under the Income-tax Act or any other authority under any law for the time being in force or on coming of any information to his notice, serve on any person, a notice requiring him on a date to be specified to produce or cause to be produced such accounts or documents or evidence as the Assessing Officer may require for the purposes of this Act and may, from time to time, serve further notices requiring the production of such other accounts or documents or evidence as he may require.

(2) The Assessing Officer may make such inquiry, as he considers necessary, for the purpose of obtaining full information in respect of undisclosed foreign income and asset of any person for the relevant financial year or years.

(3) The Assessing Officer, after considering such accounts, documents or evidence, as he has obtained under sub-section (1), and after taking into account any relevant material which he has gathered under sub-section (2) and any other evidence produced by the assessee, shall by an order in writing, assess the undisclosed foreign income and asset and determine the sum payable by the assessee.

(4) If any person fails to comply with all the terms of the notice under sub-section (1), the Assessing Officer shall, after taking into account all the relevant material which he has gathered and after giving the assessee an opportunity of being heard, make the assessment of undisclosed foreign income and asset to the best of his judgment and determine the sum payable by the assessee."

From the perusal of Section 10 of Black Money (Undisclosed Foreign Income & Assets) and Imposition of Tax Act' 2015, there is no time limit for issuing notices for assessment or reassessment under Section 10. Therefore the Black Money (Undisclosed Foreign Income & Assets) and Imposition of Tax Act'2015 stipulates no time limit for issuing statutory notice for bringing to tax any income from foreign sources both by way of assessment and reassessment. Therefore even if section 72(c) would not have been there under the Black Money Act, the Assessing Officer could have issued notices u/s 10 without any fetters of time limit. However, to the contrary, Section 197(c) of the Finance Act'2016 is in conflict with Section 143(2), 148, 153A and 153C of the Income Tax Act' 1961.

Section 143(2) of the Income Tax Act, 1961, for issue of a notice, stipulates a time limit of 6 months from the end of the financial year in which the return is furnished. Section 149 read with Section 148 of the act, for issue of notice for reassessment of domestic income, stipulates a maximum time limit of 6 Years from the end relevant assessment year. Likewise Section 153A and 153C provides for assessment /reassessment of Income of six assessment years immediately preceding the assessment year relevant to the previous year in which such search is conducted u/s 132 of the Income Tax Act'1961 or in that case requisition is made u/s 132A is made.

Therefore, if section 197(c) would not have been brought in the Finance Act' 2016, the Assessing Officer was barred by limitation to go beyond the period of limitation u/s 143(2)/149/153A or 153C, as the case may be.

To illustrate, let us assume some undisclosed income is detected by the Assessing Officer for A.Y. 2001-02 after the closure of the scheme (i.e. after 30-09-2016). After the incorporation of section 197(c) of the Finance Act' 2016, the Assessing can brought the undisclosed income to tax in the year in which notice u/s 142/ 143(2)/ 148/ 153A/ 153C is issued.

The CBDT have also clarified the aforementioned contention as under:-

(i) Vide FAQ No.4 of Circular No. 24 of 2016 dated 27th June' 2016

Question No.4 : If undisclosed income relating to an assessment year prior to A.Y. 2016-17, say A.Y. 2001-02 is detected after the closure of the Scheme, then what shall be the treatment of undisclosed income so detected?

Answer: As per the provisions of section 197(c) of the Finance Act, 2016, such income of A.Y. 2001-02 shall be assessed in the year in which the notice under section 148 or 153A or 153C, as the case may be, of the Income-tax Act is issued by the Assessing Officer. Further, if such undisclosed income is detected in the form of investment in any asset then value of such asset shall be as if the asset has been acquired or made in the year in which the notice under section 148/153A/153C is issued and the value shall be determined in accordance with rule 3 of the Rules.

(ii) Vide FAQ No.2 of Circular No. 27 of 2016 dated 14th July' 2016

Question No.2: If an undisclosed income represented in the form of an asset or otherwise pertains to a year falling beyond the time limit allowed under section 149 of the Income-tax Act, 1961 and the said undisclosed income is not declared under the Scheme, then as per the provisions of section 197(c) of the Finance Act, 2016, the said undisclosed income shall be treated as the income of the year in which a notice under section 148 of the Income-tax Act has been issued. The said provision is inconsistent with the existing time lines provided under the Income-tax Act for reopening a case. Please clarify?

Answer: Question No. 4 of Circular No. 24 of 2016 may be referred where the tax treatment of such income has been clarified. Since the Scheme contained in Chapter IX of the Finance Act, 2016 is a later law in time, the provisions of the Scheme shall prevail over the provisions of earlier laws.

III. The Controversy:-

Section 197( c) read with the clarifications so issued by the CBDT so far as to overrule the fetters imposed on the issuance of notice u/s 143(2)/148/153A,153C has raised a controversy as to how such statutory notices u/s 143(2)/149/153A or 153C can be issued after the expiry of limitation period. The Principle of limitation and time-barring of cases has all along been recognized under the Income Tax Act for the reason that the underlying jurisprudence has dictated that there has to be finality of the assessment and stale issues should not be reactivated beyond a specified period & that lapse of time must induce repose in and set at rest judicial and quasi judicial controversies as it must in other sphere of human activity. A useful reference may be made to the decision of Hon'ble Supreme Court in the case of Parashuram Pottery Works Co. Ltd. vs. ITO 106 ITR 1, 10(SC).

Let us analyze this issue from an another angle. By virtue of deeming provision, income becomes taxable in 2 years i.e. the year in which it actually accrues or is received as the case may be and in the year in which it is deemed to have been accrued or received by virtue of section 197(c). It is because the income escaped assessment and under the existing law cannot be brought to tax, the Government came out with the deeming provision u/s 197(c). There were plethora of judgments to the point that once an income belongs to a particular year and it went untaxed in that year, department cannot tax the same income in other year. However, by virtue of section 197(c), income is now deemed to accrue or arise or received in the year in which notice is issued. However, if an income belongs to a year in respect of which a notice u/s 148 can be issued, will it be taxed in the year in which notice is issued as per section 197(c) or in the year to which it actually belongs. Now, let us also analyze the implications of Section 197(c) of the Finance Act'2016 from the revenue's perspective.

Section 197(c) provides that where any undisclosed income [which has accrued or arisen or received prior to commencement of this scheme] and no declaration in respect of such income is made, such income shall be deemed to have accrued or arisen or received in the year in which a notice under section 142/143(2)/148/153A/153C is issued by the Assessing Officer, and the provisions of the Income Tax Act'1961 shall apply accordingly.

To understand the implication from the revenue's perspective, let us assume, that some undisclosed income pertaining to A.Y. 2014-15, of say 10 crores, is detected by the department in F.Y. 2016-17 ( say in December’2016). Under normal provisions of Income Tax Act' 1961, as per Section 149, notice u/s 148 can be issued for A.Y. 2014-15 up to 31-03-2021. Assessment u/s147 shall be made for A.Y. 2014-15 and interest u/s 234B and 234C shall be levied, beginning from A.Y. 2014- 15.

However, following a strict interpretation of Section 197(c) of the Finance Act' 2016, it appears that the Income so escaped for assessment for A.Y. 2014-15 shall be deemed to be the Income of A.Y. 2017-18. Pursuant to it, department will lose significant interest since u/s 194(c) , the income is deemed to be the income of the current year as thus there is no question of levying interest w.e.f from the year in respect of which the Income escaped assessment.

Therefore, by incorporating the above provision i.e. 197(c) under this scheme, the mechanism of limitation prescribed under the Act seems to be erased by the legislature.

IV. Addressing the controversy in the Union Budget 2017-18:-

In view of the aforementioned legal position and the various representations received from stakeholders citing genuine hardships if Section 197(c) of the Finance Act'2016 is made applicable, the Hon'ble FM proposed to omit clause (c) of section 197 of the Finance Act, 2016. This amendment will take effect retrospectively from lst June, 2016.

However, in order to protect the interest of the revenue in cases where tangible evidence(s) are found during a search or seizure operation (including 132A cases) and the same is represented in the form of undisclosed investment in any asset, it is also proposed that section 153A relating to search assessments be amended to provide that notice under the said section can be issued for an assessment year or years beyond the sixth assessment year already provided up to the tenth assessment year if -

(i) the Assessing Officer has in his possession books of accounts or other documents or evidence which reveal that the income which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more in one year or in aggregate in the relevant four assessment years(falling beyond the sixth year);

(ii) such income escaping assessment is represented in the form of asset;

(iii) the income escaping assessment or part thereof relates to such year or years.

Necessary enabling amendment to this effect is also proposed u/s 153A and 153C of the act. It is however proposed that the amended provisions of section 153A shall apply where search under section 132 is initiated or requisition under section 132A is made on or after the 1st day of April, 2017.

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice or a formal recommendation. While due care has been taken in preparing this document, the existence of mistakes and omissions herein is not ruled out.

By: CA Mohit Gupta

The author can also be reached at

ca.mohitgupta@icai.org

CAclubindia

CAclubindia