Ind AS-1 describes the framework for the presentation of the financial statements. In many ways, it is an accounting guideline written with the intent of paving way for the harmonisation of the accounting standards and the schedule III of the Companies act, 2013. While the ambit of AS-1, the counterpart of the Ind AS-1 in the other set of accounting standards that is applicable to companies for whom Ind-AS is not applicable, is confined to setting out of the principles relating to Fundamental accounting assumptions, nature of accounting policies, considerations for selection of accounting policies and their disclosures, the Ind AS-1 covers several other aspects with respect to Preparation and presentation of General purpose financial statements. The following is the illustrative list of the significant matters covered by the Ind AS-1:

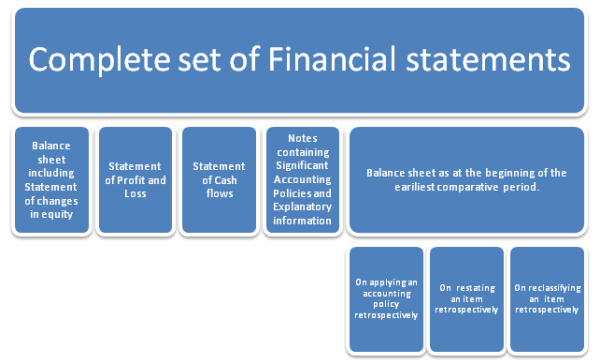

- Components of complete set of financial statements.

- Compliance with Ind-ASs.

- General features.

- Structure and content of the financial statements.

- Disclosure requirements.

Components of Financial statements

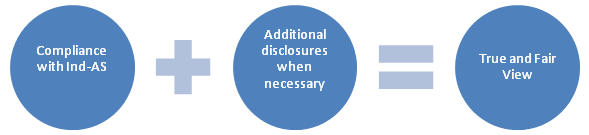

Compliance with Ind-AS

Presumption

An entity, whose statement complies with Ind AS-s is required to make an explicit and unreserved statement of such compliance in the notes.

An entity cannot rectify the mistake of following an inappropriate accounting policy either by disclosure of the accounting policy used or by notes or explanatory material. Thus entities cannot circumvent the requirement of adherence to the guidelines prescribed in Ind-AS-8 for choosing policies by disclosing the non-compliant accounting policy deployed.

|

Para 19 - Departure from the Standards |

Para 20 - Disclose the following on departure |

|

If the management concludes that compliance with Ind-AS will result in a misleading presentation of financial information it can depart from the standards as set out in Para 20. |

|

|

Where an entity departs from the requirement of a standard in a prior period and the departure has its effect in the current period, the disclosures specified in Para 20 (c) and (d) shall be made in the financial statements for the current period also. |

|

General principles to be followed in the preparation of financial statements

- Going Concern

- Entity shall make an assessment of its ability to continue as going concern as at the end of the accounting period.

- If material uncertainties exist on its ability to continue as a going concern, those uncertainties shall be disclosed.

- An entity shall prepare its financial statements, except for cash flow information, using the accrual basis of accounting.

- Each material class of similar items shall be disclosed separately.

- An entity shall not offset items of income and expenditure or assets and liabilities unless required or permitted by an Ind-AS.

- An entity shall present comparative information for the previous period.

- When an entity reclassifies items in the current financial period, it shall also reclassify those items in the comparative information and it shall disclose the nature of reclassification, the amount of each item that is reclassified and the reason for reclassification.

- An entity shall follow a presentation and classification of items consistently unless

- there is a change in nature of operation or

- there is a review of financial statements, which indicates that according to Ind AS-8 that a revised classification would be appropriate or

- an Ind AS requires a change in the presentation.

Structure and Content of Financial statements

- An entity shall clearly identify the financial statements in the published document, which contains the financial statements (E.g.: Annual report). The following information shall be displayed to facilitate understanding:

- Name of the reporting identity.

- Whether the financial statements are of an individual entity or a group.

- Date of the end of the reporting period.

- Presentation currency as defined in Ind AS 21.

- Level of rounding of amounts.

Balance Sheet

- The standard has prescribed the minimum items to be presented in the financial statement. Most of the prescribed items are the same as the items set out in the Schedule III of the Companies Act, 2013. Apart from those common items, few additional items are also prescribed namely:

- Financial assets other than investments accounted using equity method, trade receivables and cash and cash equivalents.

- Financial liabilities other than trade payables and other provisions

- Liabilities and assets for current tax

- Non-controlling interest presented within equity

- Issued capital and reserves attributable to the owners of the parent

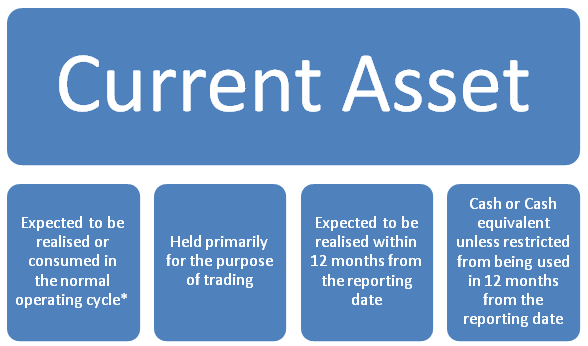

Current assets

*When the normal operating cycle of an entity is not clearly identifiable it is assumed to be 12 Months.

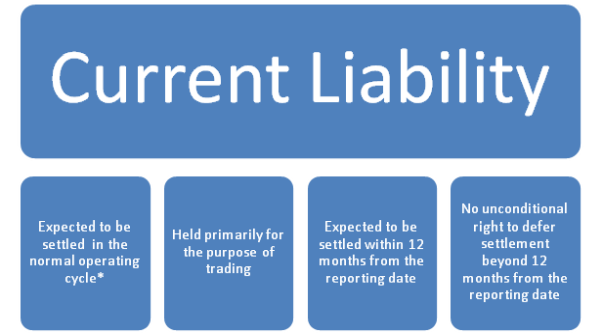

Current liabilities

*When the normal operating cycle of an entity is not clearly identifiable it is assumed to be 12 Months.

Statement of Profit or Loss

- The Statement of Profit and Loss shall in addition to normal items of income and expenditure shall contain a component called as ‘Other comprehensive income’. This is a major Carve-in that has been introduced to the Indian GAAP from the IFRS.

- Other comprehensive income has been explained in the standard as income that comprises items of income and expenditure that are not recognised in the Statement of profit or loss as required or permitted by other Ind AS-s. An illustrative list of other comprehensive income that is given in the standard is as follows :

(a) Changes in revaluation surplus as per Ind AS 16and Ind AS 38 -

(b) Actuarial gains and losses on defined benefit plans recognised in accordance with paragraph 92 and 129A of Ind AS 19- .

(c) Gains and losses arising from translating the financial statements of a foreign operation as per Ind AS 21-T

(d) Gains and losses on re-measuring available-for-sale financial assets as per Ind AS 39 -

(e) The effective portion of gains and losses on hedging instruments in a cash flow hedge as per Ind AS 39-

- Income tax and reclassification adjustments relating to the each component of other comprehensive income shall be disclosed.

- Given below is the extract of the statement of Profit or Loss from the exposure draft of the Ind-AS compliant Schedule III of the Companies Act, 2013 released by the Institute of Chartered Accountants of India.

|

|

X |

Profit/(loss) from Discontinued operations (after tax) (VIII-IX) |

xxx |

Xxx |

||

|

XI |

Profit/(loss) for the period (VII+ X) |

xxx |

Xxx |

||

|

XII |

Other Comprehensive Income A (i) Items that will not be reclassified to profit or loss (ii) Income tax relating to items that will not be reclassified to profit or loss B (i) Items that will be reclassified to profit or loss (ii) Income tax relating to items that will be reclassified to profit or loss |

xxx xxx xxx xxx Xxx |

xxx |

xxx xxx xxx xxx Xxx |

xxx |

|

XIII |

Total Comprehensive Income for the period (XI + XII) (Comprising Profit (Loss) and Other Comprehensive Income for the period) |

xxx |

xxx |

||

|

XIV |

Earnings per equity share (for continuing operation): (1) Basic (2) Diluted |

xxx xxx |

xxx xxx |

||

|

XV |

Earnings per equity share (for discontinued operation): (1) Basic (2) Diluted |

xxx xxx |

xxx xxx |

||

|

XVI |

Earnings per equity share(for discontinued & continuing operations) (1) Basic (2) Diluted |

xxx xxx |

xxx xxx |

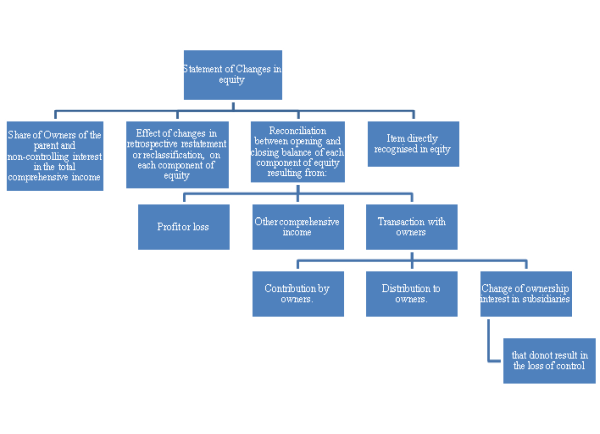

Statement of Changes in equity

It shall be presented as part of the balance sheet containing the following information.

Statement of Cash flows

- Ind AS-7 sets out requirements for the presentation and disclosure of cash flow information.

Notes to accounts and Disclosure of accounting policies

- Notes shall present information about:

- Specific accounting policies adopted and the measurement bases for preparation of the financial statements.

- Information required to be disclosed as per Ind-AS, but not presented elsewhere.

- Information relevant to understanding not presented elsewhere.

Sources of estimation uncertainty

An entity shall disclose information about the assumptions it makes about the future and other major sources of estimation uncertainty at the end of the reporting period, that have a significant risk of resulting in a material adjustment to the carrying amounts of assets and liabilities within the next financial year. In respect of those assets and liabilities, the notes shall include details of:

- their nature

- their carrying amount as at the end of the reporting period.

Capital disclosures

An entity shall disclose information that enables users of its financial statements to evaluate the entity’s objectives, policies and processes for managing capital.

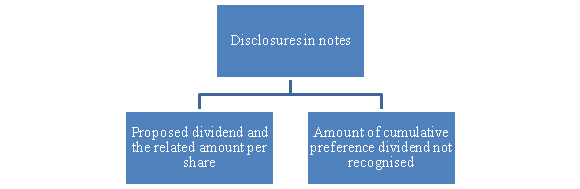

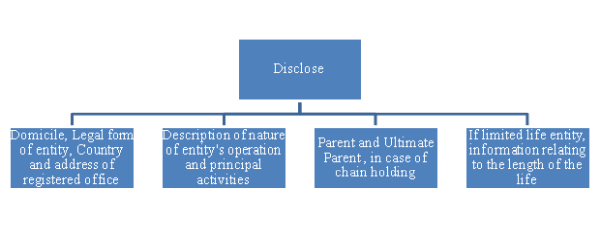

Other disclosures

Disclosures in notes

It shall also disclose the following, if they are not disclosed elsewhere.

Thus, through its encompassing guidelines, Ind AS-1 has established a holistic protocol for the preparation and presentation of the general purpose financial statements.

CAclubindia

CAclubindia