It is very important to understand when and how to show cash withdrawals in your ITR, as many income tax cases are filed concerning cash deposits and withdrawals.

Tax Implications of Cash Withdrawals

- Currently, 25% of income tax cases are related to cash deposits or withdrawals which is making a critical area of focus.

- Use of Artificial Intelligence (AI) has been increased by the Income Tax Department to flag cases of large cash withdrawals.

- There is a concern that, Artificial Intelligence is operating mechanically without "application of mind," can disproportionately trouble common and middle-class individuals.

In this article will discuss on the types of cash withdrawals that should be considered and their implications for Income Tax Return (ITR) disclosure.

Categories of Cash Withdrawals and ITR Disclosure

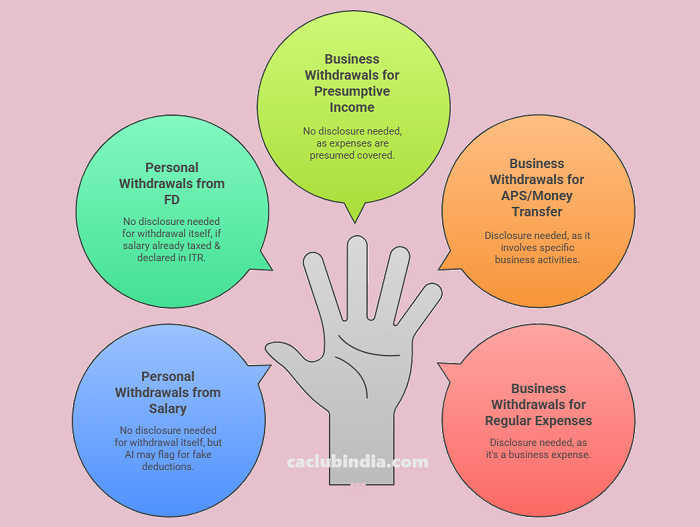

Category One: Salaried Individuals

If a salaried person earns Rs 50 lakh and withdraws a large amount of cash, for example Rs 40 lakh. This withdrawal are generally not required be reported in the Income Tax Return (ITR) as tax has already been paid on the salary.

However, in the era of AI, it may poses questions regarding cash withdrawals and tax reporting, a case might be filed. In such a scenario, the individual can explain that the cash was withdrawn from their taxed salary and can be spent anywhere. But it is important to note that deductions are strictly prohibited, as this can lead to problems if caught.

Category Two: Non-Income/Old FD Withdrawals

This category includes individuals who withdraw cash from old fixed deposits (FDs) for personal expenses like marriage, house purchase, or household expenses. There is generally no need to show these withdrawals in the ITR if the source of the funds (e.g., old FD) is explained and tax has already been paid on the original income that formed the FD.

However, AI may still raise these cases, especially if no ITR or a very small ITR has been filed. While the source of the funds say - old FD might be explained.

Category Three: Business or Professional Income (44AD/44ADA)

Individuals those with business or professional income who file ITR under sections 44AD or 44ADA, cash withdrawals for expenses do not need to be explicitly shown in the ITR. This is because these sections assume a certain percentage of profit (44AD, 44ADA) and the government believes that expenses, including cash withdrawals, are already accounted for within this presumed profit.

Category Four: APS or Money Transfer Business

People those who are involved in businesses like Aadhaar Enabled Payment System (APS) or money transfer (MT) act as custodians who is facilitating cash delivery and withdrawal in remote areas where banks are not accessible. But if such person withdraws a large amount like Rs 1 crore and shows an income of only Rs 1 lakhs, AI might flag it.

In these cases, it is crucial to disclose the nature of the business (money transfer or APS) with the proper code and description in the ITR as proper disclosure can help to win cases.

Category Five: Business Income with Cash Expenses

This category applies to businesses that receive online payments but need to make cash payments for their expenses, such as a cotton trader who receives Rs 2 crore online but pays farmers in cash Rs 1.5 crore. In this scenario, the cash withdrawal must be shown in the ITR because the business is taking the benefit of these cash expenses in their balance sheet and Profit & Loss (PNL) statement.

Conclusion

Disclosing cash withdrawals properly in your ITR is crucial to avoid income tax cases, especially with the increasing role of AI in flagging suspicious transactions. Understanding the specific rules for different income categories and maintaining proper documentation for cash expenses can help individuals and businesses navigate tax compliance effectively.

CAclubindia

CAclubindia