For decades, the Indian middle class has viewed a home loan as more than just a path to homeownership—it was a strategic "tax shield." The ability to deduct interest payments from a taxable salary was a financial rite of passage, often making the difference between a stressful EMI and a manageable one.

However, a quiet but profound structural shift has occurred. As the New Tax Regime (Section 115BAC) becomes the default choice for millions, that reliable shield is effectively vanishing. If you are a salaried professional holding a home loan or planning to take one, you are standing at a financial crossroads where the old rules of thumb no longer apply.

The Great Divide: Old vs. New

The Indian tax landscape is currently split into two distinct philosophies. The Old Tax Regime is an "Incentivized Structure." It rewards specific financial behaviors like saving for retirement (Section 80C) or buying a home (Section 24) by allowing you to subtract those costs from your taxable income.

In contrast, the New Tax Regime is a "Simplified Structure." It offers significantly lower slab rates and a higher basic exemption limit (up to Rs 12 lakh effectively tax-free for FY 2025-26), but it demands a steep price: you must forfeit almost all deductions and exemptions.

Section 24(b) and the Disappearing "Loss"

In the traditional tax-saving playbook, Section 24(b) was the star player. For a self-occupied property, you could claim a deduction of up to Rs 2,00,000 per year on the interest paid toward your home loan.

Since a self-occupied home generates no rent, this deduction technically created a "loss" under the head "Income from House Property". Under the Old Tax Regime, you could then use this Rs 2,00,000 loss to "set off" or reduce your taxable salary. If you were in the 30% tax bracket, this meant a direct cash saving of Rs 60,000 in your pocket every year.

The New Regime Restriction: A Quarantine on Losses

Under the New Tax Regime, this "inter-head set-off" mechanism has been dismantled. The restriction works in two primary ways:

1. Self-Occupied Properties: For the house you live in, the interest deduction under Section 24(b) is entirely disallowed. You cannot generate a loss, and therefore, you cannot reduce your salary income by a single rupee using your home loan interest.

2. Let-Out Properties: If you have a rented property, you can still deduct interest from the rental income. However, if the interest paid (say Rs 5 lakh) exceeds the rent received (say Rs 3 lakh), the resulting loss of Rs 2 lakh is "quarantined." You cannot adjust this loss against your salary. Furthermore, unlike the old regime, you are generally prohibited from carrying this loss forward to future years to offset future rental income.

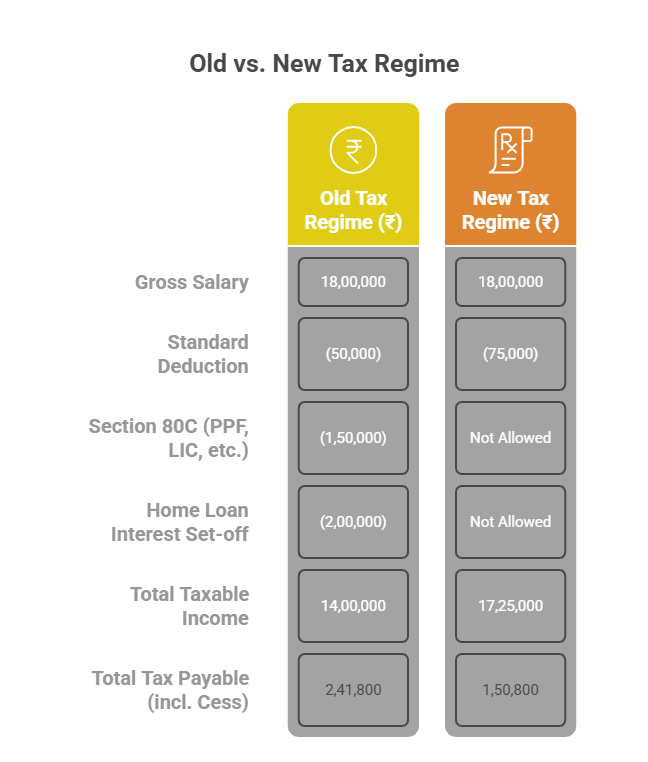

A Tale of Two Taxpayers: The Numerical Reality

To see the impact, let's look at a salaried professional earning Rs 18,00,000 per year, paying Rs 2,00,000 in home loan interest, and investing Rs 1,50,000 in Section 80C.

Sources for methodology:

In this specific scenario, the New Tax Regime actually results in a lower tax outgo by over Rs 90,000 despite losing the home loan benefit. However, the calculation changes drastically if the taxpayer also claims House Rent Allowance (HRA) or health insurance (Section 80D), which are only available in the Old Regime. If your total deductions exceed a "breakeven point"—often around Rs 3.75 lakh to Rs 4.25 lakh for high earners—the Old Regime usually wins.

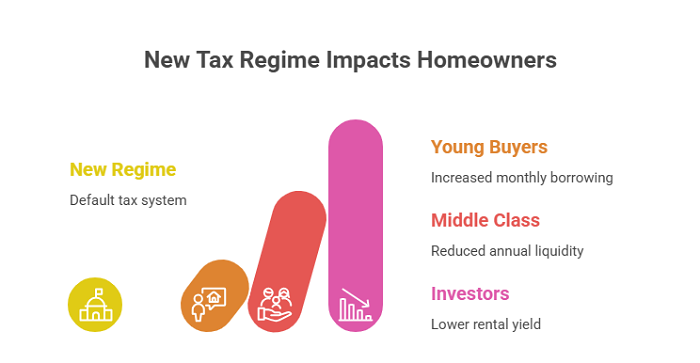

Who Is Most Affected?

The removal of the interest shield hits specific groups the hardest:

- The Young Professional: First-time buyers in expensive metros like Mumbai or Bengaluru often take high-value loans. In the early years of a mortgage, the EMI is almost entirely interest. For these individuals, losing the ability to set off Rs 2 lakh against their salary feels like a direct increase in their monthly borrowing cost.

- The Middle-Class EMI Payer: For families balancing school fees and rising utility costs, the tax refund generated by home loan interest was a vital annual liquidity boost.

- The Real Estate Investor: Those who bought a second home for rental income now find the "yield" lower because they can no longer use the property's "tax loss" to subsidize the tax on their professional income.

Concluding Takeaway: Compute Before You Opt

The New Tax Regime is designed for simplicity, and for many, it is indeed the cheaper option. But for the homeowner, it represents a departure from the "tax-subsidized" housing model we have known for decades.

The most dangerous move you can make is to follow the "default" without doing the math. Since the New Tax Regime is now the default, you must actively opt-out if the Old Regime is better for you.

Before you file your next return, use a tax calculator to find your personal breakeven point. If your home loan interest, combined with 80C and HRA, provides a larger saving than the New Regime’s lower rates, the "Old" way might still be your best way. In a landscape of vanishing shields, arithmetic is your only true protection.

Disclaimer: The views expressed in this article are the personal views of the author and are intended solely for informational and academic purposes. This article does not constitute professional advice, legal opinion, or a substitute for specific consultation. Readers are advised to evaluate the facts of their particular case independently and seek appropriate professional advice before acting on the basis of this article. The author and the firm shall not be responsible for any loss or consequences arising from reliance on the contents of this article.

The author is a FCMA and Practicing Cost Accountant

CAclubindia

CAclubindia