Warehousing provisions relaxed for EOUs, STPIs, EHTPs etc.

1. Introduction

Chapter 6 of the Foreign Trade Policy (FTP) provides for manufacture of goods and supply of services, including repair, re-making, reconditioning, re-engineering by Export Oriented Units (EOUs), Electronics Hardware Technology Park Units (EHTPs), Software Technology Park Units (STPIs) and Bio-Technology Park Units (hereinafter referred to as ?units?). These units are meant to export their entire production of goods and services, except when permitted to cater customers in DTA.?

In the said chapter, it was also provided that an EOU which intends to set up warehousing facilities outside the EOU premises and outside the jurisdiction of DC, at a place near to the port of export, to reduce lead time for delivery of goods overseas and to address unpredictability of supply orders, is permitted to do so subject to the provisions related to export warehousing as per terms and conditions of Notifications issued by the Department of Revenue.

Notification 52/2003-Customs dated 31.03.2003, as amended from time to time, exempts specified goods when imported for use in the units, from payment of Customs duties, subject to various conditions stated therein.

- The notification provides for warehousing of imported goods, to be used for manufacture of goods or other operations as well as their ex-bonding under certain circumstances.

- The Units, therefore, obtain a license as a warehouse under Section 58 of the Customs Act, 1962 and permission under Section 65 of the Act, as a manufacture-in-bond facility.??

2. Difficulties which were faced by EOUs for warehousing

Warehouses are facilities set up to avail the benefit of customs duty deferment and in the case of EOU, warehouse was a facility to manufacture and export and fulfill the obligations as per Foreign Trade Policy. Imported goods can be stored in a warehouse without payment of duty, and the applicable duty is required to be paid only at the stage of their clearance from the warehouse. In case of the above-referred units, the need for duty deferment is obviated as the goods procured by them are exempt from duties of customs, under Notification 52/2003-Customs, subject to certain conditions, such as:

- The manner of usage of the procured inputs and capital goods;

- Their end use including the removal of the said goods;?

- Maintenance of proper account of receipt, storage and utilisation of imported goods and customs formalities related to such activities;

- Execution of bond with requirement of warehouse licence;

- Sending re-warehousing certificates to the customs station of import;

- Maintenance of Warehouse bond register;

The warehousing requirements added lot of documentation work for EOUs in addition to compliance cost.

3. Amendment in the name of Ease of doing business& Make In India

In order to reduce the time and effort required for warehousing compliance in addition to promote Make in India concept for easing business, the Government has decided to do away with the need to comply with warehousing provisions. The warehousing provisions were governed by Chapter IX of the Customs Act, 1962 by these units.

For this purpose, customs notification no.44/2016 dated 29th July 2016 has been issued (effective from 13th August 2016) amending the principal notification 52/2003-Customs dated 31st March 2003 relaxing warehousing provisions. With effect from 13th August 2016, these units would stand de-licensed as warehouses under Customs Act, 1962. However, these units should adhere to other provisions of notification 52/2003.

4. Way forward from 13th August 2016

In view of relaxation of warehousing condition, the warehoused goods register (warehousing bond register) shall not be required to be maintained w.e.f 13th August 2016. It may be noted that the maintenance of B-17 running bond register would continue.

The system of sending re-warehousing certificates to the customs station of import would also stand dispensed.?

However, in order to maintain records of receipts, storage, processing and removal of goods, imported by the units, as required under notification 52/2003-Cus dated 31.3.2003, the Board has prescribed that the units shall maintain records of imported goods, in digital form[1], based upon data elements contained in Form A (format given in the Circular).

The software for maintenance of digital records must incorporate

- the feature of audit trail which means a secure, computer generated, time-stamped electronic record that allows for reconstruction of the course of events relating to the creation, modification, or deletion of an electronic record and

- includes actions at the record or system level, such as, attempts to access the system or delete or modify a record.

While the data elements contained in the Form-A are mandatory, the unit will be free to add or continue with any additional data fields, as per their commercial requirements.

All units are required to enter data accurately and immediately upon the goods being received in or removed from the unit. The digital records should be kept updated, accurate, complete and available at the unit at all times for verification by the proper officer, whenever required.

A digital copy of Form A, containing transactions for the month, shall be provided to the proper officer, each month (by the 10th of month) in a CD or Pen drive, as convenient to the unit.?

The above requirement of maintaining digital records, in the prescribed Form, is applicable from 13th August 2016. Record of imported goods received on or after 13th August 2016 shall be maintained as per the prescribed Form. The information regarding the stock of goods lying with the unit need to be integrated into the digital record prescribed under this circular.

However, data relating to goods already processed and/or cleared need not be updated in the digital records. The warehoused goods register maintained hitherto shall suffice for the purpose.?

5. Procedure in case of Inter-unit transfer of goods

Provisions related to inter-unit transfer of capital goods and manufactured goods are provided in para 6.13 of FTP 2015-20 and involves prior intimation. Additionally, at present, a procedure of bond to bond movement is being followed, whenever capital goods, manufactured goods or inputs are supplied by one unit to another. In place of bond to bond movement, the following procedure shall be followed:

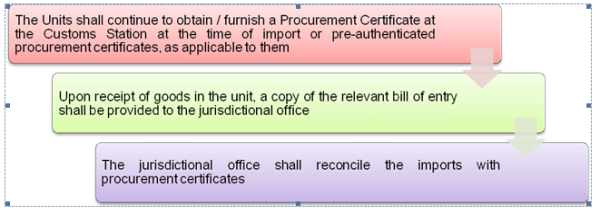

- Any procurement by one unit from another should be supported by a procurement certificate or pre-authenticated procurement certificates, as applicable.

- The supply of the goods from one unit to another shall be based upon the usual commercial documents, such as, invoice & delivery challan.

- Upon receipt of goods, copies of documents shall be provided to the jurisdictional office of the sending and receiving unit by way of intimation.

In place of the re-warehousing certificate procedure, the following is prescribed

7. Summary in a nutshell

- All warehousing units will stand de-licensed w.e.f 13th August 2016

- The system of sending re-warehousing certificates to the customs station of import shall also stand dispensed w.e.f 13th August 2016.?

- Warehouse bond register shall not be required to be maintained.

- EOUs are required to adhere to the provisions of Notification 52/2003-Customs dated 31.3.2003

- However, Form A (Format prescribed by Board) shall be maintained in digital form. Elements of such format are mandatory. Units can add additional columns if required.

- A digital copy of Form A, containing transactions for the month, shall be provided to the proper officer, each month (by the 10th of month) in a CD or Pen drive, as convenient to the unit.?

- The information regarding the stock of goods lying with the unit need to be integrated into the digital record prescribed under this circular. However, data relating to goods already processed and/or cleared need not be updated in the digital records. The warehoused goods register maintained hitherto shall suffice for the purpose.?

8. Conclusion

Hope that this would ease the business in compliance part. It is very relevant for EOUs to understand the crux of this notification and change the method of maintenance of records to digital form. However switching over from hard copy of record to digital form may pose challenge to traditional companies. Please note, above relaxation is provided only for import of goods. However, there is a necessary to provide similar relaxation for domestic procurement under notification no. 22/2003 CE dated 31.03.2003.

The authors can also be reached at Prakash@hiregange.com and Mahadev@hiregange.com.

[1]A?digital form?is an electronic version of a paper?form. Using?digital forms?gives you access to every?form?at any location. You save time and money that others are spending on the pre-printed?forms.

CAclubindia

CAclubindia