Impact of amendments on ‘Rent-A-Cab Service’ (A REVERSE GEAR)

Rent-A-Cab Service is not defined under Negative list regime. However as per the earlier definition it means any service provided or to be provided to any person, by a ‘rent-a-cab scheme operator’ in relation to the renting of a cab.

Tax impact prior to Finance Act, 2014

Negative List

As per section 65D (O) ‘service of transportation of passengers, with or without accompanied belongings by metered cabs, radio taxis or auto rickshaws’ is covered under negative list. Therefore, these services are not liable for payment of service tax.

Mega Exemption

1. As per entry no. 22 of mega exemption Notification No. 25/2012-ST dated 20-06-2012, services by way of giving on hire - (a) to a state transport undertaking (as defined in section 2(42) of Motor Vehicle Act, 1988), a motor vehicle meant to carry more than twelve passengers; (b) to a goods transport agency, a means of transportation of goods is exempted.

2. As per entry no. 23 of mega exemption Notification No. 25/2012-ST dated 20-06-2012, service of transport of passengers, with or without belongings, by a contract carriage for the transportation of passengers, excluding tourism, conducted tour, charter or hire is exempted.

Reverse Charge

As per notification no.30/2012-ST dated 20.06.2012 effective from 01.07.2012, service of renting of a motor vehicle designed to carry passengersto any person who is not in the similar line of businessprovided or agreed to be provided by an individual, HUF or firm or AOPto a business entity registered as body corporate, then the receiver of such service has to pay service tax on specified percentage of amount.

Abatement

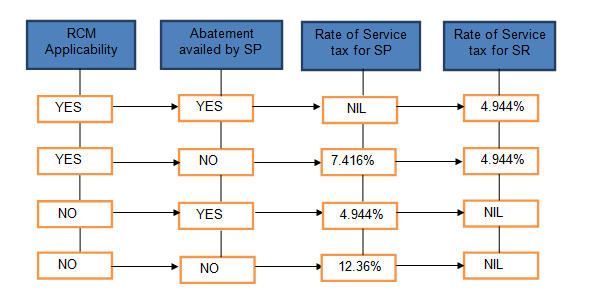

As per Serial No. 9 of Notification No. 26/2012-ST dated 20-06-2012, abatement of 60% is available on Rent-A-Cab service i.e. service of renting of any motor vehicle designed to carry passengers. It means service tax is payable on only 40% of the value of Rent-A-Cab service. The abatement is subject to the condition that the Cenvat Credit of inputs, capital goods and input services, used for providing the taxable service, has not been taken under the provisions of Cenvat Credit Rules, 2004. If the service provider avails cenvat credit on any input, capital good or input service, used for providing rent a cab service, then abatement is not available.

Effective rate of service tax applicable is provided in the following chart. Service receiver has to pay service tax @ 4.944% when he is liable to pay tax under reverse chargemechanism as per Notification no.30/2012 irrespective of the option chosen by service provider.

In the above chart

RCM = Reverse Charge Mechanism

SP = Service Provider

SR = Service Receiver

Tax impact post Finance Act, 2014

Negative List

W.e.f. 06.08.2014 (on enactment of Finance Act 2014), the provision under negative list as per section 65D (O) is ‘service of transportation of passengers, with or without accompanied belongings by metered cabs or auto rickshaws’.

As per section 65B (32), "metered cab" means any contract carriage on which an automatic device, of the type and make approved under the relevant rules by the State Transport Authority, is fitted which indicates reading of the fare chargeable at any moment and that is charged accordingly under the conditions of its permit issued under the Motor Vehicles Act, 1988 and the rules made thereunder but does not include radio taxi.

Impact of Amendment:

The entry in the negative list and the consequent definition of metered cab has been amended to bring the services of “Radio taxi” under the service tax net. Radio taxi has not been defined in the Finance Act, but the same has been defined in the mega exemption notification, which means a taxi including a radio cab, by whatever name called, which is in two-way radio communication with a central control office and is enabled for tracking using Global Positioning System (GPS) or General Packet Radio Service (GPRS).

Mega Exemption

As per entry no. 23 of mega exemption Notification No. 25/2012-ST dated 20-06-2012 amended by Notification No. 06/2014-ST dated 11-07-2014 w.e.f. 11-07-2014, service of transport of passengers, with or without belongings, by non-air conditioned contract carriage other than radio taxi, for transportation of passengers, excluding tourism, conducted tour, charter or hire is exempted.

Impact of Amendment:

It was amended to reduce the scope of exemption by restricting the exemption only to non-air conditioned contract carriages other than radio taxis. As a result, transport of passenger by air-conditioned contract carriage including which are used for point to point travel, will attract service tax, with effect from 11.07.2014.

Abatement

As per Serial No. 9 of Notification No. 26/2012-ST dated 20-06-2012 amended by Notification No. 08/2014-ST, w.e.f. 01.10.2014 abatement of 60% is available on Renting of motor cab. It means service tax is payable on only 40% of the value of Rent-A-Cab service. The abatement is subject to the following conditions.

i. Cenvat Credit of inputs, capital goods and input services, used for providing the taxable service, has not been taken under the provisions of Cenvat Credit Rules, 2004.

ii. Cenvat credit on input service of renting of motor cab has been taken under the provisions of the Cenvat Credit Rules, 2004, in the following manner:

a. Full Cenvat credit of such input service received from a person who is paying service tax on 40% of the value; or

b. Up to 40% CENVAT credit of such input service received from a person who is paying service tax on full value.

iii. Cenvat credit on input services other than those specified in (ii) above, has not been taken under the provisions of the CENVAT Credit Rules, 2004

And also as per Serial No. 9A inserted by Notification No. 08/2014-ST in Notification No. 26/2012-ST w.e.f.11.07.2014 in case of transportation of passengers with or without accompanied belongings, by a contract carriage other than motor cab and radio taxi (in case of radio taxi w.e.f. 06.08.2014), abatement of 60% is availablesubject to condition that Cenvat credit on inputs, capital goods and input services used for providing the taxable service has not been taken under the provisions of the Cenvat Credit Rules, 2004.

Impact of Amendment:

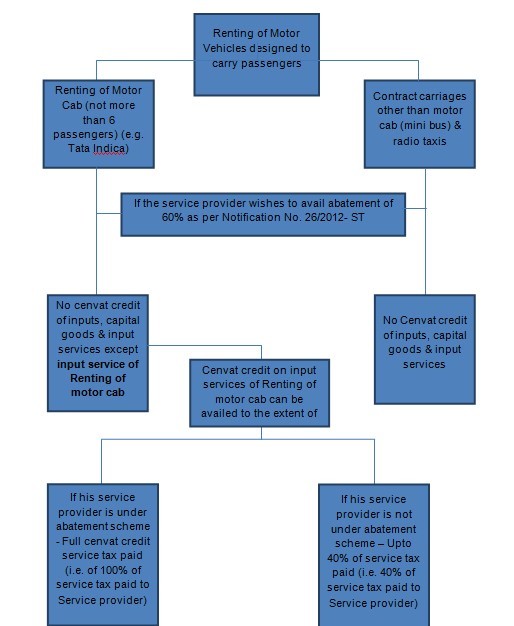

Upto Finance Act, 2014 (From 01.07.2012), all provisions of abatement & reverse charge applicable to ‘renting of motor vehicles designed to carry passengers.’ It means it includes renting of motor cars, motor cabs, maxi cabs, mini buses, buses and all other motor vehicles which are designed to carry passengers, irrespective of its passenger carrying capacity. However,w.e.f. 11.07.2014 (06.08.2014 in case of radio taxis), separate provisions applicable to ‘Renting ofmotor cab’& ‘any contract carriage other than motor cab and radio taxis’.

i. ‘Motor Cab’ has not defined under Negative List Regime. Hence as per the earlier definition under section 65 (71) read with Section 2(25) of Motor Vehicle Act, 1988, “Motor cab means any motor vehicle constructed or adapted to carry not more than six passengers excluding the driver for hire or reward.”

ii. Hence in case of Motor cab i.e. a vehicle capable of transporting not more than 6 passengers, serial number 9 of Notification No. 26/2012- ST applicable from 01.10.2014. However for all other vehicles (in case of maxi cabs, mini buses, and buses) and radio taxies serial number 9A of Notification No. 26/2012 – ST is applicable. For our easy understanding it is explained in the following chart.

Reverse Charge

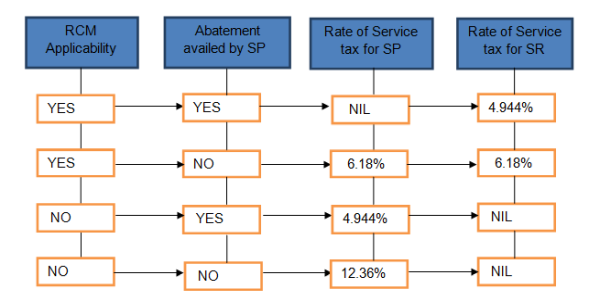

Notification 30/2012 is being amended vide Notification 10/2014 ST dated 11.07.2014, with effect from 01.10.2014. As per the amendment, in case service provider has not opted for any abatement scheme, the percentage of service tax payable by the service provider and service receiver has been changed to 50% (Service Provider)/50%(Service Receiver) instead of 60%/(Service Provider) 40% (Service Receiver).

Impact of Amendment:

Impact of such amendment has been provided as a chart as follows.

Moral: It is easy to purchase a car than to take it on hire.

For further clarifications/views/suggestions/comments mail to carajeshmaddi@gmail.com

CAclubindia

CAclubindia