Introduction:

The two foremost facets of ‘Decisions’ for a company are “Investment” & “Financing” Decisions. Investing Decisions determines Companies ‘Assets’ while Financing Decisions determines Companies ‘Liabilities’.

Wealth Maxim:

Investment decisions affect the wealth of the company through ‘Return on Investment’ (IRR) whereas Financing decisions affect the wealth of company through Cost of Capital (Ko). When IRR > Ko wealth increases and when IRR < Ko wealth decreases. Thus maximization of wealth is achieved by proper combination of above decisions. The company raises funds through various Sources of Finance, Invest in diverse ventures considering the forecasts and thereby earns Profit. These Profits are used to service the various finance providers i.e. Financial Institutions, Stakeholders, Suppliers, Customers etc. Out of these service providers, amount financed by the Shareholders plays a pivotal role as their contribution is significant and their expectation on return increases, particularly when the growth prospects increase. The predominant shareholders for the companies are Preference Holders, Debenture Holders, & Equity Holders.

A Contracted amount has to be paid as Consideration for Debenture and Preference holders, whereas for Equity Shareholders it is at the disposal of the company to discharge the profits or retain it (i.e. It is at the Option of the company whether to ‘Pay Dividend or Not’) If the company had decided to pay the Equity holders a return by dividend, the onus is on the dividend policy and the quantum of amount to be paid. If paid, the next question arises is that will payment of dividend have impact on shareholders wealth apart from companies wealth and its subsequent impact on share prices.

Dividend Policy Theories – A Phenomenon

Based on the above parameters, two theories have been postulated by Strategic Financial Analysts and are below:

Theory of Relevance was propagated by Walter & Gordon. They suggested that Issue of Dividend erodes the Wealth of the company and there will be a decline in the Share Price of the company. On the contrary, ’Theory of Irrelevance’ was formulated by Modigliani & Miller suggesting that issue of dividend has no relevance with share price or wealth of the company.

Lets us discuss the various propositions in detail:-

WALTER’S MODEL:

This Model suggests payment of dividend to the stakeholders considering certain key parameters. According to Walter, Companies Profit has two options

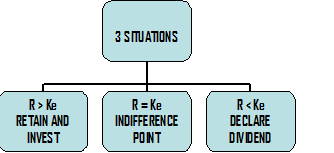

If it is to be distributed as Dividend, then Investor can invest on its own @ Ke (Cost of Equity). But if the profit is retained, the company will invest it on behalf of the investors at ‘r’ (IRR of new projects). He formulates three situations based the share value on which the decision can be taken

SITUATION I: The First Situation is defensive on the part of company to retain and invest the profits so that the company can earn more profits, which is far from the expectation of investors.

SITUATION II: Second situation is indifference between retaining and declaring the profits.

SITUATION III: The third alternative is to declare the profits as dividends to stakeholders. This occurs when the company forecasts itself that it will not be able to satisfy investor expectations by venturing into new projects

VALUATION OF SHARE UNDER WALTER MODEL:

D+R/KE [E-D] / KE

Where,

E-D = Retained Earnings (which will be company investments)

Ke - Cost of Equity (Investor expectation i.e. What Investor wants)

D/Ke - Present Value of Perpetual Dividends

E= 1-b/Ke-br (br- Growth rate)

GORDON APPROACH

Gordon’s Model too suggests payment of dividend to the stakeholders. But unlike Walter, Gordon suggests Payout (Dividend) either at 100% or Nil %. He contemplates that if dividend is declared there will be no growth, since no growth EPS will be stagnant, i.e. Level at which profit is constant. Furthermore Current Dividend is safer than future profits which are uncertain and risky. Investor prefers such company as a good investing opportunity. He classifies Dividend policy into two angles ‘RISK & RETURN‘

RETURN:

Growth in Return is possible, only if new investments are made, and such exploring is possible only when profit is retained hence thereon two situations arises:

LOW DIVIDEND PAYOUT & HIGH RETENTION - LEADS TO HIGH GROWTH AND INCREASES IN COMPANY SHARE PRICE

HIGH DIVIDEND PAYOUT & LOW RETENTION – LEADS TO LOW GROWTH AND DECREASES IN COMPANY SHARE PRICE

RISK:

Investors feel Current Dividend is safer than the promised Capital Gain in future through Growth in Share Price. The two situations under Risk angle thereon:

LOW PAYOUT & HIGH RETENTION – MORE RISK, HIGH DISCOUNT RATE, LOW SHARE PRCE

HIGH PAYOUT & LOW PAYOUT – LESS RISK, LOW DISCOUNT RATE, HIGH SHARE PRIOCE

VALUATION OF SHARE UNDER GORDON MODEL:

Po=E(1-b)/Ke-br

Where, E=Earnings, b = Retention Ratio, 1-b = Payout,

br = growth rate; r =IRR of new Projects

Gordon concludes the model by suggesting that every Payout has Growth & Risk aspect and by using above formula whichever alternative as aforesaid listed gives highest share price, it can be considered as Optimal Payout

MODIGILANI & MILLER:

The only theory which suggests that issue of dividend doesn’t affect the wealth of Shareholder as well as company is M&M Approach. They contend that the issue of dividend has no impact on the share price of the company. Their view is that only Investment Decisions will affect the wealth of the company and good Investment Opportunities will increase the Wealth of the Company.

Let’s analyze their proposition in detail:

Eg: Profits $ 10000

The Company can utilise the same in following two ways:

Option 1: Company can invest $ 10000 in the shares of a company

Option 2: Or distribute it as Dividend to the shareholders and thereon raise money from the shareholders by making a fresh issue of Equity shares thereby creating a scope for new investments.

Benefit for shareholders is Dividend

Cost to the company is more shareholders participation in the wealth of the company. Numerically,

Share Price before Issue of Dividend = 10000/1000 = 10 per Share

Share Price Post Issue of Dividend = 9000/1000 = 9 per Share

New shares – 111;

Wealth on Declaring Dividend – 1111 Shares * 9 per share = 10000

It is explicit that there’s no erosion in the wealth of shareholders as well as to the company irrespective of issue of dividend. Thus Dividend benefit is offset by the capital loss.

VALUATION OF SHARE UNDER M&M:

NPO= P1(N+M-I+M)/1+KE

Where, N= Existing Shares, M= New Shares (By investments), E=Earnings, Ke=Discount Rate, P1=Price at End of the year.

Thus M&M under this model suggests that there will be indifference between Dividend & Retention.

CAclubindia

CAclubindia