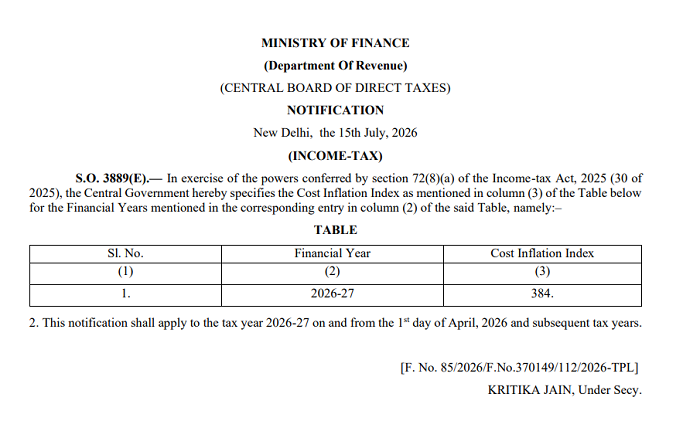

The Central Board of Direct Taxes (CBDT) has officially notified the Cost Inflation Index (CII) for the Financial Year 2026-27 at 384, providing clarity for taxpayers and professionals dealing with capital gains computations under the new Income-tax Act, 2025. The notification was issued by the Ministry of Finance on 15 July 2026 through Notification No. S.O. 3889(E).

for FY 2026-27 Under Income Tax Act, 2025")

Cost Inflation Index for FY 2026-27

According to the notification, the Cost Inflation Index specified for the Financial Year 2026-27 is:

| Financial Year | Cost Inflation Index (CII) |

|---|---|

| 2026-27 | 384 |

The index has been notified under Section 72(8)(a) of the Income-tax Act, 2025 , which empowers the Central Government to specify the Cost Inflation Index for relevant financial years.

Applicability

The notification clarifies that the notified Cost Inflation Index will apply to the Tax Year 2026-27 beginning from 1 April 2026 and to subsequent tax years, wherever relevant under the provisions of the Income-tax Act, 2025.

Why the Cost Inflation Index Matters

The Cost Inflation Index has traditionally been used to adjust the purchase cost of certain capital assets for inflation while calculating long-term capital gains. Although the taxation framework for capital gains has undergone significant changes in recent years, the notification of CII remains an important compliance and reference point under the Income-tax Act, 2025.

Tax professionals, chartered accountants, and taxpayers should take note of the newly notified index while evaluating transactions and understanding the impact of inflation adjustments under applicable provisions of the law.

Key Takeaway

With this notification, the CBDT has fixed the Cost Inflation Index at 384 for FY 2026-27, effective from 1 April 2026. The notification provides an important reference for capital gains taxation and other provisions linked to inflation indexing under the Income-tax Act, 2025.

Official copy of the notification is as follows

CAclubindia

CAclubindia