Taxpayers may choose to withdraw from the Simplified Registration Scheme under Rule 14A of the CGST Rules, 2017 which was effective from 1st November 2025 and move to normal GST compliance.

Option to withdraw from Rule 14A is available on GST portal via Form REG-32.

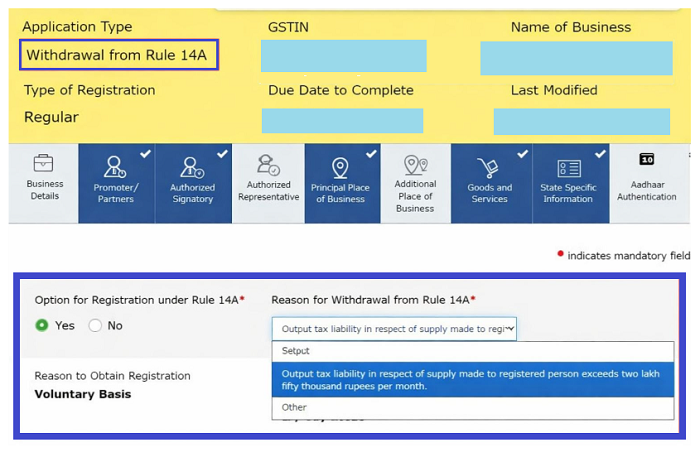

When To Withdraw the Simplified Registration Scheme?

A taxpayer may withdraw if:

- The total output tax liability on supplies made to registered persons exceeds ₹2.5 lakh per month.

Features of the Simplified Registration Scheme

Automatic Electronic Registration

Eligible applicants will receive auto-approved GST registration within 3 working days of submission of FORM GST REG-01

Aadhaar Authentication

Aadhaar authentication is compulsory for:

- The Primary Authorised Signatory

- At least one Promoter or Partner of the entity.

Single Registration Restriction

Only one registration per State or Union Territory under one PAN. This means - taxpayer must not hold more than one GST registration per State or Union Territory

Application Procedure

Applicants must select ‘Yes’ for Rule 14A in FORM GST REG-01 for registration under Rule 14A.

Mandatory Return Filing Before Withdrawal

Before withdrawal, the taxpayer must:

- File all the pending returns from the date of registration till the date of withdrawal.

Minimum Return Filing Period

The minimum return filing requirement depends on timing:

| Period of Withdrawal | Minimum Returns Required |

| Before 1st April 2026 | At least 3 months’ returns |

| On or After 1st April 2026 | At least 1 tax period return |

Restriction on Withdrawal Process

Withdrawal will not be permitted if any of the following are pending:

- Application for amendment of registration,

- Application for cancellation, or

- Department-initiated cancellation proceedings

All such proceedings must be completed first.

Effective Date of Changes from Rule 14A

Once withdrawal under Rule 14A is approved, changes become effective from the next month.

The taxpayer will thereafter be governed by normal GST compliance provisions.

CAclubindia

CAclubindia