The Ministry of Corporate Affairs, on 10th April, 2015, notified the Companies (Auditor’s Report) Order, 2015 (CARO, 2015).

The text of the Order is available on the following URL

http://www.mca.gov.in/Ministry/pdf/Companies_Auditors_Report_Order_2015.pdf

The governing law for CARO 2015 is the Companies Act, 2013. This Order has been issued and notified pursuant to the powers granted to the Central Government in terms of the provisions of Section 143(11) of the Companies Act, 2013.

Let us look at some of the frequently asked questions on CARO, 2015 (hereinafter referred to as CARO)

Frequently Asked Questions on CARO, 2015

Which companies are exempt from the applicability of CARO?

CARO is not applicable to the following companies:

1. Banking Company

2. Insurance Company

3. Section 8 (formerly Section 25) Company

4. Small Company within the meaning of Sec 2(85) of the Companies Act, 2013

5. One Person Company and

6. Select class of Private Company

Which are the select class of private companies to which CARO is not applicable?

CARO is not applicable to private limited companies which fulfils all the following conditions throughout the reporting period covered by the audit report :

(i) its paid-up capital and reserves are Rs 50 lacs or less;

(ii) its outstanding loan from any bank or financial institution are Rs 25 lacs or less; and

(iii) its turnover does not exceed Rs 5 crores

A private limited company, in order to be exempt from the applicability of CARO, must satisfy all the conditions mentioned above cumulatively. In other words, even if one of the conditions is not satisfied, a private limited company’s auditor has to report on the matters specified in the Order.

What is the definition of Small Company under the Companies Act, 2013?

Sec 2(85) of the Companies Act, 2013 defines a small company. As present, It is a private company whose paid-up share capital does not exceed Rs 50 lacs and turnover as per its last profit and loss account does not exceed Rs 2 crores

Provided that nothing aforesaid shall apply to (A) a holding company or a subsidiary company; (B) a company registered under section 8; or (C) a company or body corporate governed by any special Act;

Has ICAI issued any guidance on reporting under CARO 2015?

Yes, the ICAI has issued guidance note. The same may be accessed using the following link: http://resource.cdn.icai.org/37394aasb26880new.pdf

Is the Statement on CARO, 2003, issued by the Institute of Chartered Accountants of India still relevant?

Yes. ICAI in para 2 of its document for guidance on reporting under CARO 2015 states as follows:

“Members would have noted that, inter alia, the exemption criteria applicable to private companies as laid down in the paragraph 1(v) of the CARO, 2015 is same as that in the Companies (Auditor’s Report) Order, 2003 (CARO, 2003). Also, it is noted that the twelve reporting clauses given in paragraph 3 of CARO, 2015 are similar in their requirements to the corresponding clauses in paragraph 4 of the CARO, 2003. Further, the requirement to state reasons for unfavourable or qualified answers as given in paragraph 4 of the CARO, 2015 is also similar to that contained in paragraph 4 of the CARO, 2003. Accordingly, members are advised to continue to draw in principle guidance from the relevant paragraphs of the Statement on the Companies (Auditor’s Report) Order, 2003, issued by the Institute of Chartered Accountants of India.”

The statement on the CARO, 2003 issued by ICAI can be accessed using the following link: http://resource.cdn.icai.org/18798announ10264a.pdf

Has the term “paid up capital” been defined in Companies Act, 2013?

Yes, Sec 2(64) of the Companies Act, 2013 defines the expression paid-up share capital or share capital paid-up to mean such aggregate amount of money credited as paid-up as is equivalent to the amount received as paid up in respect of shares issued and also includes any amount credited as paid-up in respect of shares of the company, but does not include any other amount received in respect of such shares, by whatever name called;

Paid-up share capital would include both equity share capital as well as the preference share capital. While calculating the paid-up capital, amount of calls unpaid should be deducted from and the amount originally paid-up on forfeited shares should be added to the figure of paid-up capital. Share application money received should not be considered as part of the paid-up capital. One may also refer Para 17 of the Statement on CARO 2003 for further clarification.

Has the term “reserves” been defined in the Companies Act, 2013?

No, the term “reserves” has not been defined under the Companies Act, 2013. However, the Guidance Note on Terms Used in Financial Statements issued by ICAI defines the term “reserve” as, “The portion of earnings, receipts or other surplus of an enterprise (whether capital or revenue)appropriated by management for a general or specific purpose other than provision for depreciation or diminution in the value of assets or for a known liability. The reserves are primarily of two types: capital reserves and revenue reserves”. One may also refer Para 18 of the Statement on CARO 2003 for further clarification.

Has the term “turnover” been defined in the Companies Act, 2013?

Yes, the term “turnover” has been defined in Section 2(91) of the Companies Act, 2013 to mean the aggregate value of the realisation of amount made from the sale, supply or distribution of goods or on account of services rendered, or both, by the company during a financial year. One may also refer Para 23 of the Statement on CARO 2003 for further clarification.

Will CARO be applicable to a small company which has a loan outstanding exceeding 25 lacs from any bank or financial institution?

Small Companies are generally exempted from the applicability of CARO, 2015. In my view, it shall not attract the applicability of CARO, so long as it remains a small company as defined under Section 2(85) of the Companies Act, 2013.

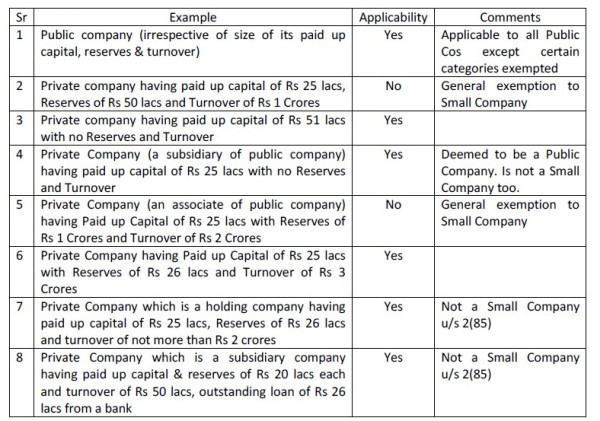

Can the applicability of CARO 2015 be illustrated through some examples?

While reporting on the requirements of CARO, 2015, is a reference thereto also needs be added to the main audit report?

Yes, while reporting on the requirements of CARO, 2015, a reference thereto also needs be added in the main audit report under the “Report on Legal and Other Regulatory Matters” paragraph

Is there any specimen format for the aforesaid reporting?

Yes, the Auditing and Assurance Standards Board of ICAI has issued the following illustrative format in terms of its recent guidance on reporting under CARO, 2015. The same is reproduced as follows:

“Report on Other Legal and Regulatory Requirements

As required by the Companies (Auditor’s Report) Order, 2015 (“the Order”), issued by the Central Government of India in terms of sub-section (11) of section 143 of the Companies Act, 2015, we give in the Annexure a statement on the matters specified in paragraphs 3 and 4 of the Order, to the extent applicable.

As required by Section 143 (3) of the Act, we report that:

.............................

……………………………”

By CA Sumit Binani,

sumit_binani@hotmail.com

Disclaimer by the Author

Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of the Companies Act and Rules. The user of the information agrees that the information is subject to change without notice. I assume no responsibility for the consequences of use of such information. IN NO EVENT SHALL I SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM, ARISING OUT OF OR IN CONNECTION WITH THE USE OF THE INFORMATION.

CAclubindia

CAclubindia