Like input tax credit reversal on input and input service, there is a requirement to reverse the Input Tax Credit taken on the capital goods.

ITC reversal on capital goods does not arise in the following case when Capital Goods used:

- Exclusively for affecting exempt supplies.

- Exclusively for the non-business purpose.

- Exclusively for affecting taxable supplies.

Hence the input tax credit reversal requirement arises when capital goods used for affecting different kind of supplies like:

- Used cumulatively for business and non-business purpose.

- Used cumulatively for affecting exempt and taxable supplies.

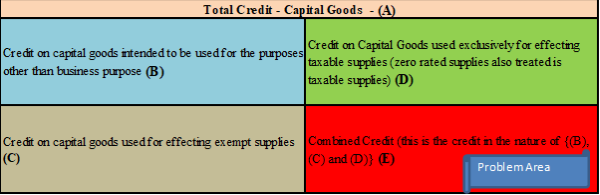

The total credit on capital good can be bifurcated in the following table:

Total credit on capital goods will be the combination of ((B)+(C)+(D)+(E))

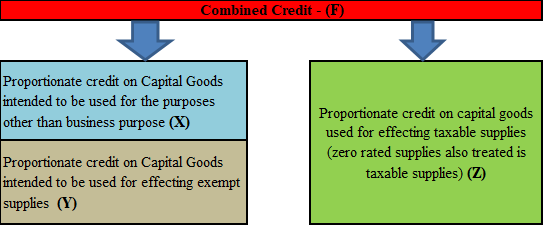

Combined credit can be bifurcated in the following way:

Following are the treatment of different type of credit mentioned in the invoice of the capital goods in the form GSTR-2:

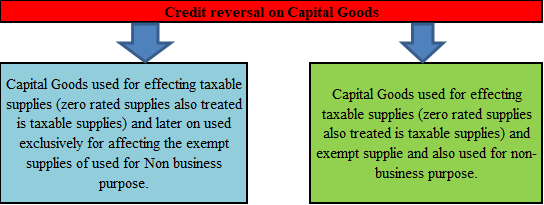

Reversal of Input Tax Credit on the capital goods required in the following two circumstances:

Case-1: Capital Goods used for effecting taxable supplies (Zero-rated supplies also treated is taxable supplies) and later on used exclusively for affecting the exempt supplies used for the non-business purpose.

- Assume the useful life of assets as 5 years (60 months).

- Determine the remaining useful life of the asset out of the period of 60 months.

- The amount of credit reversal shall be as per the following:

(Total credit on the capital goods X remaining useful life)/total useful life (5 years/60 months)

Case-2: Capital Goods used for effecting taxable supplies (Zero-rated supplies also treated is taxable supplies) and exempt supplies and also used for the non-business purpose.

- Determine the total turnover (T).

- Determine the turnover of exempt supplies (E).

- Input Tax Credit on commonly used capital goods attributable to the tax period (C).

Reversible Input tax credit = (C X E)/T

The reversal of credit must be done for each tax period i.e. on monthly basis. And also on yearly basis.

This calculation shall be done for each tax component i.e. CGST, SGST, and IGST for each tax period.

CAclubindia

CAclubindia