CBDT vide Notification No. 33/2018 amends Form no. 3CD in respect of tax audit under section 44AB

Introduction:

The Central Board of Direct Taxes (CBDT) vide Notification No. 33/2018/F.No. 370142/9/2018-TPL dated 20 July 2018 has amended the Income-tax Rules, 1962 (the Rules), under the powers conferred by section 44AB read with section 295 of the Income-tax Act, 1961 (the Act). Following are key new reporting requirements incorporated in Form no. 3CD and the same are effective from 20 August 2018:

1. Income chargeable from other sources [section 56(2)(ix)] [Clause 29A] and section 56(2)(x) [Clause 29B]

If any amount is chargeable under the head 'income from other sources' under section 56(2)(ix) and section 56(2)(x), then the nature of the income and the amount are required to be disclosed.

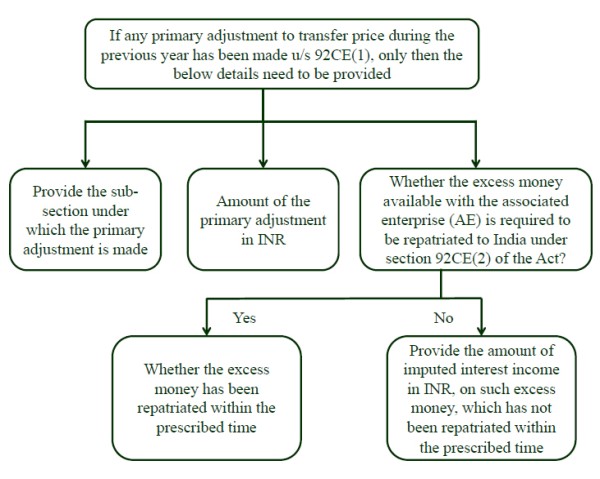

2. Secondary adjustments in certain cases [section 92CE] [Clause 30A]:

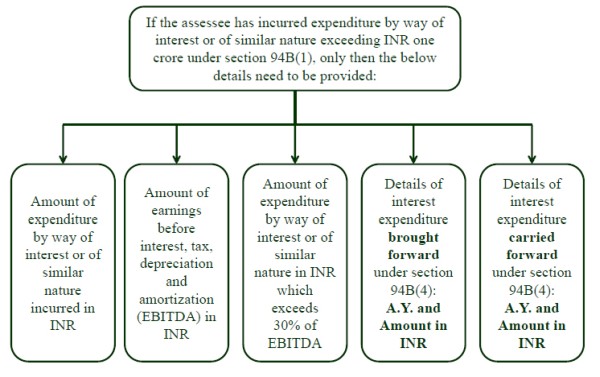

3. Limitation on interest deduction in certain cases [section 94B] [Clause 30B]

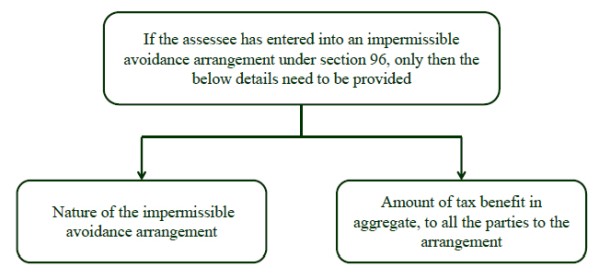

4. General Anti-Avoidance Rule [section 96] [Clause 30C]

5. Disclosure requirements for amounts exceeding limit prescribed under section 269ST [Clause 31(A)(ba),(bb),(bc) and (bd)]

The notification prescribes certain disclosure requirements, if the amount of specified transactions exceeds the limits prescribed under section 269ST, that is, name, address and PAN of the party.

6. Details to be furnished regarding tax deducted or collected [Clause 34(b)]

If the assessee is required to furnish statement of tax deducted or tax collected at source, as per the provisions of Chapter XVII-B or Chapter XVII-BB, then the following details would be required to be reported:

- Tax deduction and collection Account Number (TAN),

- Type of form,

- Due date for furnishing and date of furnishing, if already furnished,

- List/ details of all transactions which were required to be reported but not disclosed by the assessee

7. Deemed dividend under section 2(22)(e) [Clause 36A]

If the assessee has received any amount in the nature of dividend under section 2(22)(e), then the amount received and the date of receipt are required to be disclosed.

8. Furnishing of statement in Form 61, Form 61A or Form 61B [Clause 42]

The assessee is required to report the details regarding entity identification number, form type, date, list/ details of transactions which were required to be reported in form 61, form 61A, and form 61B, but not disclosed by the assessee.

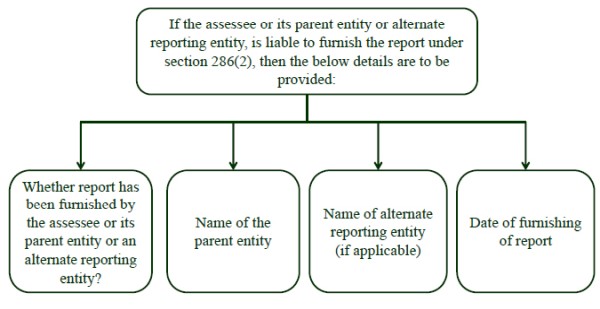

9. Furnishing of report in respect of international group [section 286] [Clause 43]

10. Break-up of expenditure [Clause 44]

The assessee is required to disclose break-up of total expenditure incurred during the year, in relation to the entities registered and not registered under GST.

Our Comments:

The new reporting requirements of Form no. 3CD seem to be very onerous and obligatory on taxpayers and chartered accountants.

Further, one may have to evaluate whether the reporting requirements for Country-by-Country report under section 286 may not only create more transparent information to be provided by multinational enterprises to the tax authorities, but will also entail more onerous compliance and documentation requirements on such enterprises.

Moreover, due to the new reporting requirement prescribed by the Notification, the multinational enterprises will also have to evaluate the applicability of Country-by-Country report under section 286, before filing of Form no. 3CD, whereas under section 286 r.w. Rule 10DB, the reporting requirements are to be completed latest by, 31 March 2019.

CAclubindia

CAclubindia