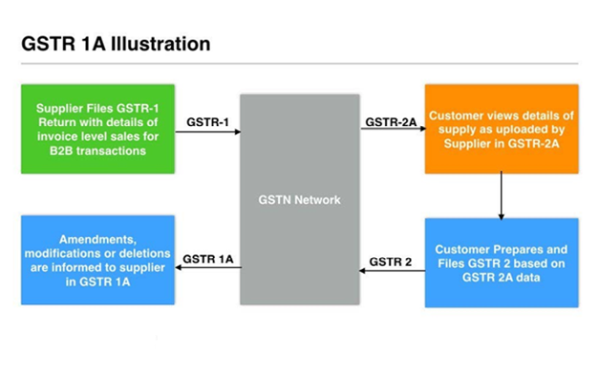

Introduction: GSTR 1A return shows the amendments, modifications or deletions made by the recipient in GSTR 2 return. In this article, we look at details to be provided in GSTR 1A return in detail.

GSTR-1A is an addendum to GSTR-1- Outward supplies statement of the supplier. It is always generated on the basis of details added/ modified/ deleted by the counterparty (B2B Transactions) in GSTR- 2/4/6. The details so created in the system are then auto-populated to the supplier on submission of GSTR- 2/4/6.

GSTR-1A is generated after the end of tax period and only if the supplier has filed his GSTR-1 before the receiver files his GSTR-2/4/6.

All normal taxpayers and casual taxpayers are required to file GSTR-1A.

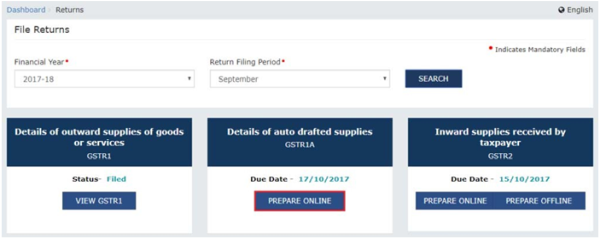

GSTR-1A can be filed from the returns section of the GST Portal. In the post login mode, you can access it by going to Services > Returns > Returns Dashboard. After selecting the financial year and tax period, GSTR-1A in the given period will be displayed.

Supplier can file GSTR-1A only from 16th till 17th of the month succeeding the tax period. (For July date is 6TH December).

Supplier can take actions (including filing) in GSTR-1A only from 16th till 17th of the month succeeding the tax period.

GSTR-1A can be filed before filing of GSTR-2.

GSTR-1A is generated when the recipient in GSTR-2/4/6 takes any of the following action:

- Rejects the details added by the supplier and submits the return

- Modifies the details added by the supplier and submits the return

- Adds any new details missed by the supplier and submits the return

All the above details get auto-populated to the supplier in the Form GSTR- 1A only if the following conditions are met:

- Recipient submits GSTR- 2/4/6 on or before 17th of the month succeeding the M tax period

- The supplier has not yet generated GSTR-3 for M tax period.

- The supplier has not yet submitted GSTR-1A of M tax period

If any one of the above mentioned conditions are met, then all such modifications/ additions/ rejections will flow to the suppliers' GSTR-1 of the subsequent tax period.

Supplier cannot add any details in GSTR-1A.

GSTR-1A is not mandatory to be submitted before generation of GSTR-3.

In a case where GSTR-1 has not been filed for M tax period before GSTR- 2/4/6, the details added by the counter party are auto populated to GSTR-1 of the M tax period of the supplier who may include the same for submitting his GSTR-1.

In case, GSTR-1A has been generated by the taxpayer and not submitted and in the meantime some receivers have filed GSTR- 2/4/6, then the supplier has to generate GSTR-1A again before submission.

However, details on which supplier has already taken action will not be impacted due to regeneration of GSTR-1A. If GSTR-1A has been submitted, then all the details which have been kept pending by taxpayer will roll over to GSTR-1 of next tax period. Post 17th of succeeding month of tax period, if GSTR-3 has not been filed, taxpayer will be able to see the GSTR-1A, however, he won't be allowed to take any actions on the same.

If GSTR-1A has not been filed by taxpayer till 17th of the subsequent month of the tax period, then on generation of GSTR-3 by taxpayer, all the details will roll over to GSTR-1 of next tax period.

In case of non-filing of GSTR-1A, roll over of details will happen on generation of GSTR-3, whether GSTR-3 has been filed after 17th or before 17th.

Post 17th of succeeding month of tax period, if GSTR-3 has not been filed, taxpayer will be able to see the GSTR-1A, however, he won't be allowed to take any actions on the same.

How to file GSTR 1A Return On GST Portal?

Step 1: Login to GST Portal and Select GSTR 1A

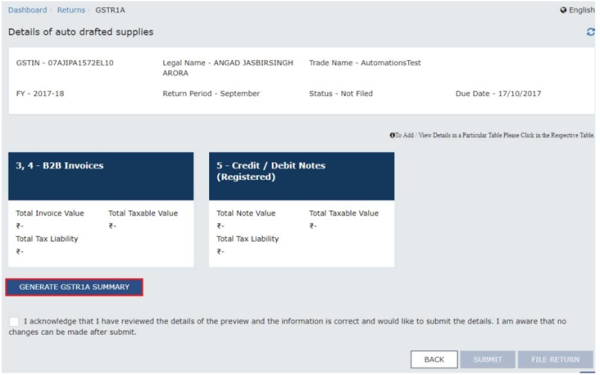

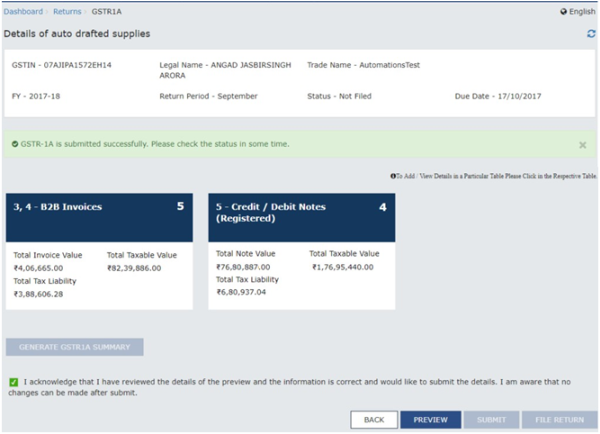

Step 2: View or Download GSTR 1A Summary

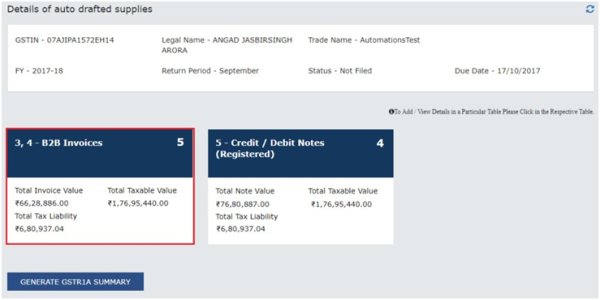

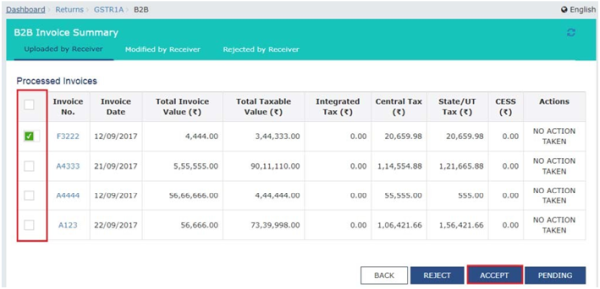

Step 3: View B2B Invoices Summary

Step 4: Take action on amendments, modifications and deletions

Step 5: File GSTR 1A Return

The author is a practicing CA based in Delhi and is registered Insolvency Professional. He can be reached at cavinodchaurasia@gmail.com

Disclaimer: The views expressed in this article are strictly personal. The content of this document are solely for informational purpose. It doesn't constitute professional advice or recommendation. The Author does not accept any liabilities for any loss or damage of any kind arising out of information in this article and for any actions taken in reliance thereon.

CAclubindia

CAclubindia