Overview

TDS under section 194J of the Income Tax Act 1961 is deducted on payments made for professional services, technical services and director fees but with the implementation of the Income Tax Act, 2025, TDS deduction rules on professional and technical services has been revised with new section, updated payment codes and changes in reporting requirements. Taxpayers are now need to ensure compliance using the new section, updated challan codes, and revised TDS return forms while depositing and reporting TDS.

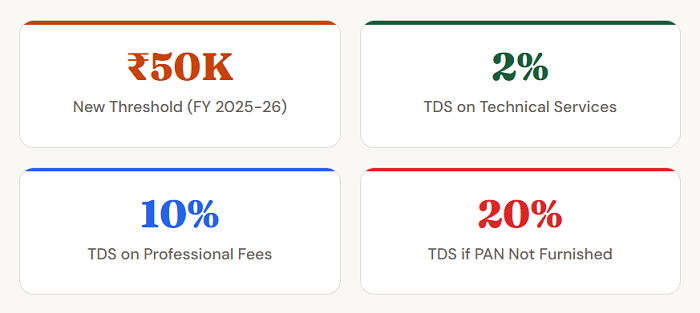

Budget 2025 update: From 1st April 2025, the threshold for TDS u/s 194J has been raised from ₹30,000 to ₹50,000.

Who Must Deduct TDS Under Section 194J?

Section 194J requires any person (excluding individuals/HUFs not liable for audit under section 44AB) to deduct TDS when making specified payments such as:

- Any sum by way of - (a) fees for technical services (not being a professional services); or (b) royalty in the nature of consideration for sale, distribution or exhibition of cinematographic films; or (c) payee, engaged only in the business of operation of call centre.

- Any sum by way of - (a) fees for professional services; or (b) any sum referred to in section 26(2)(h).

- Any sum by way of remuneration or fees or commission by whatever name called, other than those on which tax is deductible under section 392, to a director of a company.

However, the below persons are not liable to deduct TDS under section 194J on such payments:

Threshold Limit and TDS Rate

Also read - TDS Rate Chart For Tax Year 2026-27

Section 194J TDS: Latest Update As per Income Tax Act 2025

| Payment Type | Old Section (Act 1691) | New Section (Act 2025) | New Payment Code | Rate |

| Technical Services | 194J(a) | 393(1)[Sl.6(iii).D(a)] | 1026 | 2% |

| Professional Services | 194J(b) | 393(1)[Sl.6(iii).D(b)] | 1027 | 10% |

| Director Fees | 194J(b) | 393(1)[Sl.6(iii).D(b)] | 1028 | 10% |

Payments Covered Under Section 194J

Professional Services

- Medical practitioners, doctors, surgeons, hospitals

- Lawyers, advocates, legal consultants

- Chartered Accountants, Cost Accountants, Company Secretaries

- Architects, interior designers, engineers (consulting)

- Management consultants, HR consulting firms

- Film artists, authors, journalists, news anchors

- Publicity company payments by film artists

Technical Services

- IT professionals, software consultants, system integrators

- Engineering services

- Data exchange services

- Call centre operators

Also Covered

- Royalty: copyrights, patents, trademarks, licences, technical/commercial knowledge.

- Non-compete fees: payments to restrict competition or sharing of proprietary info.

- Director's remuneration: sitting fees, commission, professional charges (non-salary).

TDS Deposit Due Date

TDS to be deposited by the 7th of the following month. For March deductions, due date is 30th April.

TDS Return Due Date

| Month | Due Date | Reported in Form | Issue Form to Payee |

| Q1 (Apr-Jun) | 31st July | Form 140 | Form 131 |

| Q2 (Jul-Sep) | 31st October | Form 140 | Form 131 |

| Q3 (Oct-Dec) | 31st January | Form 140 | Form 131 |

| Q4 (Jan-Mar) | 31st May | Form 140 | Form 131 |

Penalties & Interest for Non-Compliance

| Failure to Deduct TDS | TDS Deducted but Not Deposited |

| 1% per month | 1.5% per month |

FAQs

What is the TDS threshold limit u/s 194J for FY 2026-27?

Threshold limit has been increased from ₹30,000 to ₹50,000 effective April 1, 2025.

What form is used to file TDS u/s 194J in FY 2026-27?

Form 140 is used for quarterly filing of TDS on payments other than salary. After filing, deductors must issue Form 131 to the payee as a TDS certificate.

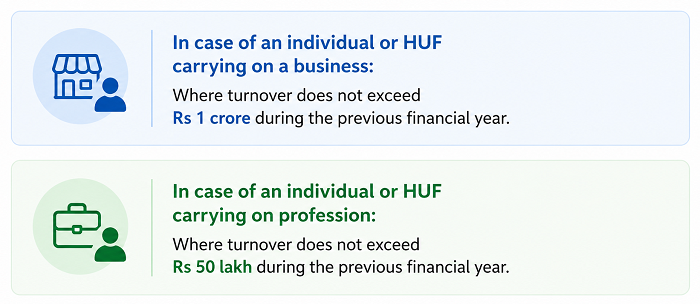

Is an individual required to deduct TDS under Section 194J?

Generally no TDS is applicable u/s 194J unless the individual or HUF had business turnover exceeding ₹1 crore or professional receipts exceeding ₹50 lakh in the immediately preceding financial year (i.e., was liable for tax audit under Section 44AB). Even then, payments for personal purposes are exempt.

CAclubindia

CAclubindia