Major changes were made in CA Act 1949 in year 2006 to improve quality of services given & punish CAs who indulges in professional misconduct. One of the very important change was introduction of Chapter VIIA, Sec 28A to 28D dealt with very powerful body “Quality Review Board”. 5 Members + Chairman are appointed by Central Government & 5 by ICAI council, So majority is with CG. This amendment was inserted in November 2006 but body was constituted after 6 years in 2012 , that will surely raise many eye brows.

As on today composition is 1 person from IRS / 1 person from IAS (Joint Secretary MCA) / 1 person from SEBI / 1 person (DG from C&AG) / 1 Person from law ministry + 1 more reputed person are appointed by central government. And 5 members are from council including 3 past presidents of ICAI. From this we can understand strength and importance of this Board.

As per Sec 28B functions of this board are

(a) to make recommendations to the Council with regard to the quality of services provided by the members of the Institute;

(b) to review the quality of services provided by the members of the Institute including audit services; and

(c) to guide the members of the Institute to improve the quality of services and adherence to the various statutory and other regulatory requirements.

After lot of pressure from international bodies like IMF Quality Review Board (QRB) started functioning. This body conducted REVIEW of “175 audits” conducted by CA Firms of listed companies during 3 years from 2012 to 2015 and report was issued after 3 years of constitution on 5th June 2015. Selection was done on random basis which represent 63% market cap of the stocks listed on Bombay Stock Exchange (BSE). In first ever report by Quality Review Board they have indicated that around 60% of auditors of “listed companies” need improvement and 25 firms are referred to council of ICAI for further action.

Some key findings from report. These reviews were conducted by 78 technical reviewers who are CA with more than 15 years of experience.

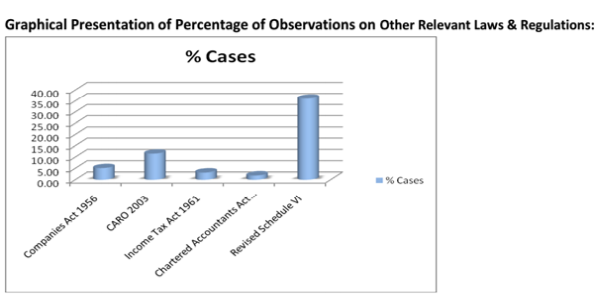

1. Percentage Analysis of Non Compliances various LAWS applicable.

In 35% audits under non compliance format & disclosures were not as per Sch VI (Now Schedule III)

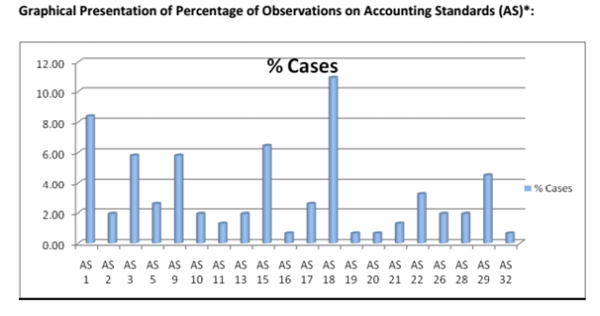

2. Percentage Analysis of Non Compliance of Accounting Standards

In 11% audits under non compliance AS 18 Related Party was not followed.

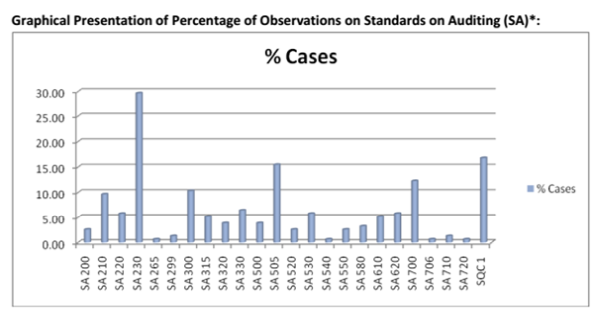

3. Percentage Analysis of Non Compliance of Standards on Auditing.

In 29% audits under non compliance SA 230 “Audit Documentation” was not followed.

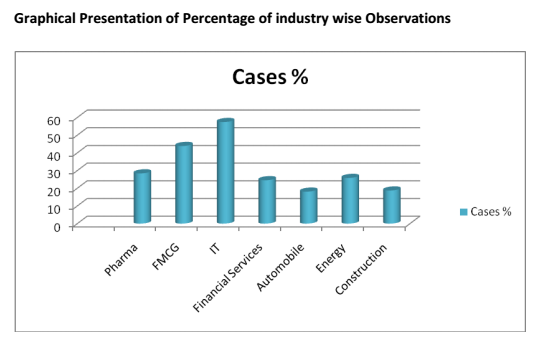

4. Percentage Analysis of Non Compliances in various industries.

More than 50% non compliances in IT industry followed FMCG.

These results does not appear good for overall quality of audit services even at level of listed companies. QRB cannot start disciplinary action against any CA Firm, neither it can recommend any disciplinary action. But it surely calls for better audit procedures in compliance with various professional pronouncements.

To enrol for the class on Advanced Auditing of the author: Click here

To enrol for the class on Auditing & Assurance of the author: Click here

CAclubindia

CAclubindia