Hello friends, sorry for delay in my last part of Section 9 'Levy & Collection' in case of E Commerce Operator. And I am really very thankful such a great and positive feedback on my third Article "Section 9 of CGST Act, 2017: Levy and Collection (Reverse Charge)" Friends in my third Article I have discussed second part of Section 9 "Levy & Collection" in case of Reverse Charge.

Today we will discuss Section 9: Levy & Collection" in case of E Commerce Operator" In this article we will cover our last part i.e. Levy & Collection in case of E Commerce Operator.

In this article we will discuss the term 'E COMMERCE OPERATOR' to that extent it is relevant for this article. The detail discussion about E Commerce Operator will be done in my upcoming articles.

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017

CHAPTER III

LEVY & COLLECTION OF TAXES

Levy and Collection

PART 1 - Section 9(1) and Section 9(2) already discussed in last article

PART 2 - Section 9(3) and 9(4) "Levy & Collection" in case of Reverse Charge

PART 3 - Section 9(5) 'Levy & Collection&' in case of E Commerce Operator.

9(5). The Government may, on the recommendations of the Council, by notification, specify categories of services the tax on intra-State supplies of which shall be paid by the electronic commerce operator if such services are supplied through it, and all the provisions of this Act shall apply to such electronic commerce operator as if he is the supplier liable for paying the tax in relation to the supply of such services:

Provided that where an electronic commerce operator does not have a physical presence in the taxable territory, any person representing such electronic commerce operator for any purpose in the taxable territory shall be liable to pay tax:

Provided further that where an electronic commerce operator does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

Understanding of the words 'E- Commerce Operator'

Electronic commerce means 'commercial transactions conducted electronically'. In our day to day life we do a lot of shopping through online websites like Flipkart, Amazon, Alibaba etc. even we take many services through these portals like hiring of cab from OLA and Uber. what is this? This is all E Commerce transactions. As simple as it may seem in above definition, electronic commerce began traditionally as online retail shop (by selling own stock on internet) , but has now transformed the entire way of doing business and in a better and more profitable manner when compared to the traditional business.

According to Section 2 (44), 'Electronic Commerce' means the supply of goods or services or both, including digital products over digital or electronic network.

The success of companies like Flipkart, Myntra, Paytm, Amazon, MakeMyTrip and eBay has fascinated all from traditional businessman to the newcomers as start-ups and not to forget even governments. The online solutions, as they should better be called, have evolved new models of supply of goods and services. They have made the entire world a smaller place without compromising on the quality of their products.

According to Section 2 (45), 'Electronic Commerce Operator' means any person who owns, operates, or manages digital or electronic facility or platform for electronic commerce.

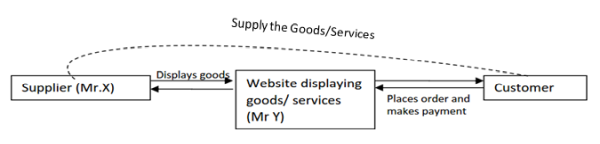

In simple words, ECO is any person who provides an electronic platform between the actual supplier and buyer and charges the fee or commission for providing such platform. In below image, Mr. Y is an Electronic Commerce Operator (like Flipkart, Amazon) who is providing the platform facility between the actual supplier (Mr. X) and buyer.

Do you know: 'Uber, the world's largest taxi company, owns no vehicles! Facebook, the world's most popular media owner, creates no content! Alibaba, the most valuable retailer, has no inventory!. And Airbnb, the world' largest accommodation provider, owns no real estate'

Friends, I will see this in more detail while discussing section 52 i.e. 'Collection of tax at source' in my upcoming articles.

2. Whether on all the Supplies supplied through ECO, the ECO is liable to pay the tax?

No, only in case of INTRASTATE SUPPLIES supplied through ECO, the ECO is liable to pay tax. In case of INTERSTATE SUPPLY the provision of section 9(5) shall not be applicable.

3. Whether on All the goods or services supplied through ECO, the ECO is liable to pay the tax?

No, only in case of SERVICES supplied through ECO, the ECO is liable to pay the tax and such service should be notified by the Government and such services should be notified on the recommendation of the council. You may conclude that provision of section 9(5) is not applicable in case of Goods and Services other than notified services by the Government on the recommendation of the council.

4. Understanding of the words 'all the provisions of this Act shall apply to such Electronic Commerce Operator as if he is the supplier liable for paying the tax in relation to the supply of such services'

Friends, we have already discussed above generally supplier is liable for paying the taxes in case of a supply and since he is the person liable to pay taxes and in case of any default he will be penalized with the relevant provisions of this act. But here ECO is neither a supplier nor a recipient of services he is only providing a platform for actual supplier and buyer. In above Mr. X is the actual supplier the tax liability should be of Mr. X. Since the Government has made Mr. Y (ECO) as the person liable to pay the tax instead of Mr. X. Just like in case of reverse charge supply is made by supplier in case of reverse charge but recipient is liable to pay taxes and in case of any default the provisions of relevant act should be applicable to the recipient instead of the supplier. Same provision has been made in case of ECO. That's why the words are used 'all the provisions of this Act shall apply to such ECO as if he is the supplier liable for paying the tax in relation to the supply of such services'.

What will be the implications if such ECO has no physical presence in taxable territory?

In case, ECO has no physical presence in taxable territory, ANY PERSON representing such ECO for ANY PURPOSE in the taxable territory shall be liable to pay the tax. It is not necessary that such person should represent such ECO for taxation purpose even if he is representing such ECO for marketing purpose even then such person shall be liable to pay the tax.

5. What will be the implications if such ECO has no physical presence in taxable territory and also does not have a representative in the said territory?

Where an electronic commerce operator does not have a physical presence in the taxable territory and also, he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such appointed person shall be liable to pay tax.

Friends, in the end of this article I want to know from you, if you have read my all three article on Section 9 'LEVY AND COLLECTION OF TAX', please give me some feedback.

I am in confusion from last few months whether a book on GST is to be written which can cover all the aspects of the GST from every angle in a very simple language like my all articles on CAclubindia and must subscribe my Youtube channel ALL ABOUT TAXES by clicking on this link below -

https://www.youtube.com/channel/UCl2Wqe5TZXnnd1SBjl3Ve8A/videos.

CAclubindia

CAclubindia