Overview

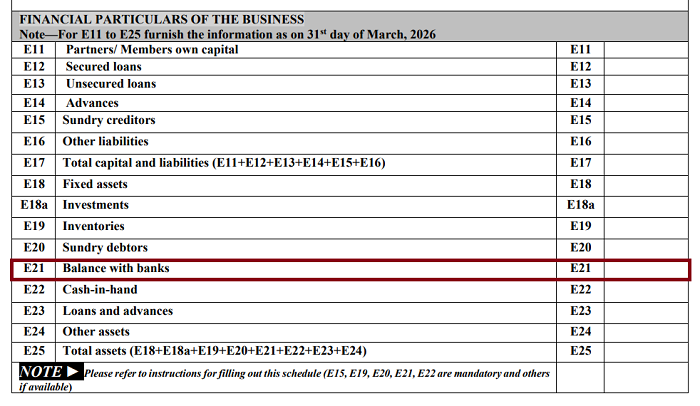

Starting from AY 2026-27, the Income Tax Department has made bank balance reporting mandatory in ITR-4 for taxpayers with business or professional income, including those opting for presumptive taxation. Earlier, people filing ITR-4 have to report only four basic items like Sundry Debtors, Sundry Creditors, Inventory and Cash in Hand, bank balance reporting was optional but now reporting of bank balance as on 31 March has become mandatory in new field E21.

Who Is Affected with this Bank Balance Disclosure Rules in ITR-4?

Taxpayers who are filing ITR-4 under presumptive taxation:

| Section | Covers |

| 44AD | Small business owners |

| 44ADA | Professionals (doctors, CAs, etc.) |

| 44AE | Transporters |

Which Bank Balances to Report in Field E21?

You need to report all the closing balances of business bank accounts as on 31 March 2026. You just need to add all balances together and enter the single combined figure in Field E21 in ITR-4.

Balances to Include

- Savings or Current accounts (account using for business purpose)

- Overdraft accounts or cash credit (if positive balance). Note - If overdraft and cash credit account shows negative balance - do not deduct it from your bank balance (E21), instead you can show the negative amount separately as an secured loan or liability under field E12.

- UPI-linked bank balances (Google Pay, PhonePe etc.).

Do Not Include:

- Fixed Deposits (FDs), Recurring Deposits (RDs): Report under Investments

- Wallet balances (such as Paytm, Phone pe etc.): Report under Other Assets

- Credit card outstanding as of 31st March: Report under Other Liabilities (E16)

- Credit Card Payment made before 31st march 2026: if fully then reporting not required.

- Credit card limit: Do not report (it’s not an actual asset or liability)

- Personal bank accounts (not used for business): Do not include. If mixed use, then safer to include proportionately or full.

- Cash in hand: Report separately under E22

- Dormant/inactive accounts: Generally not required to disclose.

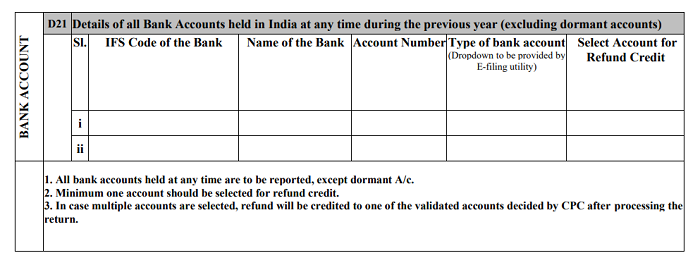

Separate Bank Account Disclosure

You must report all bank accounts separately that were active during the FY 2025–26 (1 Apr 2025 to 31 Mar 2026) even if the account is zero balance or rarely used account.

For each account, you need to provide details:

- Bank name

- Account number

- IFSC code of Bank

- Account type (savings/current/OD/Joint)

- Select Account for Refund Credit

Note : Missing any active account may lead to a penalty of ₹10,000.

Do Not Confuse About Reporting "Balance with banks under field (E21)"

Under field E21 (Balance with banks) - Report only the total of all business bank account balances as on 31 March.

Penalty for Non-Compliance

If mismatch found between declared amount and actual bank balance then it may trigger tax notices with penalties.

| Violation | Consequence |

| Misreporting | Up to 200% penalty |

| Not disclosing a bank account | ₹10,000 fine |

Conclusion

From FY 2025-26, ITR-4 filers must mandatorily report their bank balance as on 31 March 2026 in field E21. This applies to all taxpayers under presumptive taxation (44AD, 44ADA, 44AE). A mismatch between declared income and bank balance can trigger tax notices with high penalties.

CAclubindia

CAclubindia