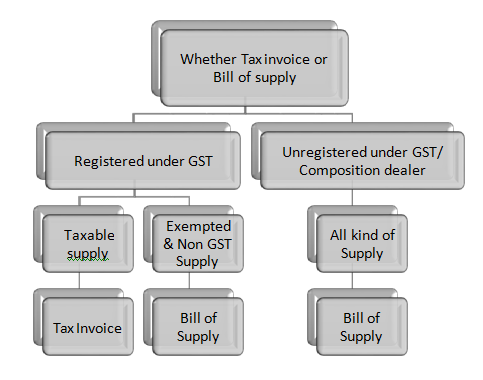

What is the meant by Tax invoice?

As per Section 2(64) of CGST Act Invoice or tax invoice means the tax invoice referred to in section 31 of CGST act.

Who has to the raise the Tax invoice?

A registered taxable person should raise the tax invoice.

Who has to raise the Bill of supply?

In the following cases bill of supply needs to be raised,

- Unregistered person

- Registered taxable person under composition scheme.

Whether Tax invoice needs to be raised for Exempted and NON GST supplies also?. If not what document needs to be raised?

Tax Invoice should not be raised in case of supply of Exempted and NON GST supply. Bill of Supply needs to be raised while supplying the Exempted and NON GST supply.

Exceptions:

1. Registered taxable person can issue a single 'tax invoice cum bill of supply', when he is supplying taxable as well as exempted goods or services or both to an unregistered person.

2. Registered taxable person can issue a consolidated tax invoice at the closer of the day against all supplies made during the day, provided following conditions needs to be satisfied

- Value of goods or services supplies should not exceed Rs. 200

- The recipient is not a registered person and

- The recipient doesn't require such invoice.

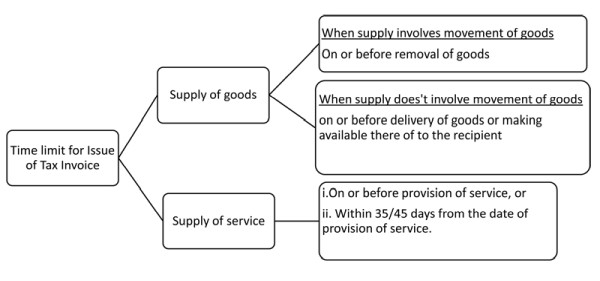

When the invoice should be raised?

a) Incase of supply of goods: The Tax invoice needs to be raised before or at the time of,

• Removal of goods for supply to the recipient, where supply involves the movement of the goods or,

• delivery of goods or making available thereof to the recipient, in any other case

b) Incase of Supply of Services: The Tax invoice needs to be raised at earliest of,

• Before the time of provision of service or

• Within 30 days from the date of the supply of service. However the banking companies or insurer or financial institutions including non-banking financial company can raise the invoice within 45 days from the date of provision of service.

Exceptions:

1. Insurer or a banking company or a financial institution, including a non- banking financial company, or a telecom operator, making the taxable supplies of services between distinct persons as specified in section 25, may issue the invoice before or at the such supplier records the same in his books of accounts or before expiry of the quarter during which supply was made.

2. Continuous supply of goods or services:

I. Incase of goods: Tax invoice needs to be raised before or at the time when the statement of accounts is raised or payment is received against the continuous supply of goods.

II. Incase of services: Tax invoice needs to raised as followed

• Where the due date for payment is ascertainable from the contract, Invoice needs to be raised on or before the due date.

• Where the due date for payment is not known then, invoice needs to be raised on or before the receipt of payment

• Where the payment is linked to completion of an event then, invoice needs to be raised on or before the completion of event.

3. Goods sent on sale on approval basis: Tax invoice needs to be raised before or at the time of supply or six months from the date of removal whichever is earlier.

How to raise the Tax invoice ?

As per the rule 48 of CGST rule the tax invoice needs to be raised in the following manner:

a. Incase of goods: the invoice needs to be prepared in triplicate as follows. Original copy should be marked as 'Original for recipient'. Duplicate copy should be marked as 'Duplicate for transporter' Triplicate copy should be marked as 'Triplicate for supplier'.

b. Incase of service: The invoice needs to be prepared in duplicate as follows. Original copy should be marked as 'Original for recipient' Duplicate copy should be marked as 'Duplicate for supplier'.

What document needs to be raised on the receipt of advance against the supply? Registered taxable person should raise the receipt voucher on receipt of advance against the supply.

How to pay GST on receipt of advance when the supplier doesn't know the nature of supply or rate of GST?

If the supplier doesn't know the GST rate on receipt of advance then he has to pay GST at 18%. If the supplier doesn't know the nature of supply i.e. whether Intra or Interstate supply then, it shall be treated as Inter-state supply.

What is meant by self-invoice?

Registered taxable person should raise the self-invoice against the purchases from un-registered persons. Even persons registered under composition scheme also need to raise the self-invoice against the URD purchases.

What is the difference between refund voucher & payment voucher?

Refund voucher needs to be raised when the supply is not made and the advance amount is given as refund to the customer on which tax has been paid. Payment voucher needs to be raised when payment is made by the registered taxable person to the supplier against the URD purchases.

The author can also be reached at cavinod111@gmail.com

CAclubindia

CAclubindia