Overview

Effective 1st April 2026, the Income Tax Department has scrapped both 15G and 15H forms under the new Income Tax Act 2025 and replaced them with a single unified self-declaration Form 121.

Transition from Form 15G & 15H to Form 121

| Form 15G & 15H as per IT Rules, 1962 | Form 121 as per IT Rules, 2026 |

| Section 197A (1), 197A(1A) & 197A(1C) of IT Act, 1961 | Section 393(6), 393(7) of IT Act, 2025 |

| Rule 29C of IT Rules, 1962 | Rule 211 of IT Rules, 2026 |

What is Form 121?

Form 121 is a self-declaration form submitted by eligible taxpayers to a payer under Section 393(6) of the Income Tax Act, 2025, read with Rule 211 of the Income Tax Rules, 2026. By submitting Form 121, you declare that:

- Total estimated income for the tax year is not taxable as it is below the basic exemption limit.

- Final tax liability will be nil.

Therefore, TDS should not be deducted from their income.

Looking for the official Form 121 format, then Click Here to view and download the PDF version.

Why Form 121 was introduced?

Form 121 has been introduced to simplify the TDS declarations rules. Earlier, taxpayers had to choose between:

- Form 15G: for individuals below 60 years

- Form 15H: for senior citizens aged 60 years or above

This age classification caused unnecessary confusion.

Now, Form 121 removes this distinction entirely under the new Income Tax Act 2025, creating one simple form for everyone.

For Example

Senior citizen who were previously filing Form 15H now required to submit new Form 121 - no separate form is needed for your age group. The process is the same, only the form has updated.

Are you still confused whether you or your senior citizen parents can file Form 121 when tax is nil but income crosses ₹4 lakh? Clear Your Doubt Here.

Who Can File Form 121?

- Resident Individuals - any age (whether below 60 or above 60)

- Hindu Undivided Families (HUFs)

- Other specified eligible entities

What Income Types Does Form 121 Cover?

Form 121 can be submitted to avoid TDS on the following income types:

| Income Type | Payer / Deductor | Payee / Deductee |

| PF / EPF Withdrawal | EPF Trustees / Authorized Person | Individual (not company or firm) |

| Insurance Commission | Person paying commission | Resident Individual / Other Resident |

| Rent | Specified Person | Resident Individual / Other Resident |

| Mutual Fund / Unit Income | Person responsible for payment | Resident Individual / Other Resident |

| Interest on Securities | Banking company / Cooperative bank / Post office |

Resident Individual / Other Resident |

| Other Interest Income | Specified Person (Non-bank) | Resident Individual / Other Resident |

| Life Insurance Payout | Person responsible for payment | Resident Individual / Other Resident |

| Dividend Income | Domestic Company | Resident Individual |

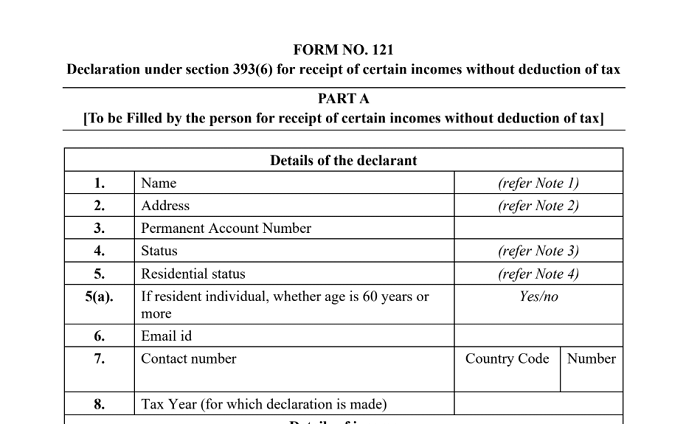

How to fill Form 121?

Download Form No. 121 of income tax in pdf and fill the Part A:

Part A - Filled by Declarant

- Personal details such as Name, Address, PAN, Status, Residential Status, Date of Birth, Contact details and Tax Year.

- Provide income details – Nature of Income, Estimated income, Aggregate amount of Income, Estimated total income of the Tax Year and Details of last two Tax Year’s ITR filed.

Part B - Filled by Payer

- Name, Address, TAN, PAN, Contact details and Tax Year.

- PAN, UIN, Address, Contact details, Estimated income, Estimated total income of the Tax Year, Aggregate amount of Income and Date on which declaration is received.

Submission can be manual or online, depending on payer. The bank/finance company may provide online facility.

Still have doubts about applicability, tax liability or compliance - Ask Here and get answers from the professionals.

What should the Payer do after Receiving Form 121?

When a person submits the declaration, payer needs to verify eligibility (PAN, Status, etc.) and record the form.

The payer assigns a UIN for each Form 121 received. This UIN has multiple components (Sequence Number, Tax Year, TAN of payer).

The payer is required to upload a consolidated statement of all Forms 121 received on a monthly basis through the e-filing portal of the Income-tax Department (via TAN login) even though no TDS is deducted.

Steps:

- Ensure payer has a valid TAN and is registered on e-filing portal.

- Download the CSV utility.

- Login via TAN on Income Tax e-Filing portal → e-File → Fill Form

No. 121 (select applicable Form, Year, Month, Filing Type) → Attach CSV + Signature → Upload.

After upload, status will show “Uploaded”, then after processing “Accepted” or “Rejected”.

Even though no tax is deducted at source because of Form No. 121, the payer must quote the UIN of the declarant in the quarterly TDS statement in Form No. 140 so that records align.

Difference between Form 15G, Form 15H and Form 121

| Feature | Form 15G/15H | Form 121 |

| Basis of Year | Based on Assessment Year (AY) | Based on Tax Year |

| Language | Used technical wording such as "Name of Assessee" | Uses simpler wording like "Name" |

| Age Details | Asked for Date of Birth | Simply asks to select "yes or no" whether you are 60 years or above. |

| Identification number | PAN or Aadhaar allowed | Only PAN is accepted |

| Previous ITR details | Asked whether ITR was filed in the last 6 years | Asks ITR details for last 2 years only |

| TDS sections | Required section references | No technical section inputs |

| Investment account number | Required specific investment account numbers | Not required |

Form Submission Time Limit

Form 121 must be submitted at the beginning of the every financial year. Even if your income situation has not changed.

Consequences of Filing a False Form 121 Declaration

Providing false declaration is a criminal offence under Section 482 of the Income Tax Act, 2025 which can lead to rigorous imprisonment of 6 months to 2 years, along with legal consequences.

FAQs

Who Can File Form 121?

Resident Individuals (whether below or above 60 years), Hindu Undivided Families (HUFs) and other specified eligible entities whose total income is below the taxable limit and no tax liability for the year.

Who Cannot File Form 121?

Companies, Firms and Non-residents are not eligible to submit Form 121.

What are the documents required to file Form No. 121?

PAN of the declarant, TAN of Payer, Proof of age, Details of income/investment for which no TDS is to be deducted, Bank account details.

When is the last date to submit Form 121?

There is no fixed last date, you can submit at the beginning of the tax year or before income is credited.

Where is the declaration data reflected?

The declaration data is reflected in Form No. 168/AIS.

What if I submit Form 121 after TDS is deducted?

The deductor cannot reverse the TDS amount already deducted. You must claim it as a refund in your ITR.

CAclubindia

CAclubindia