Retirement benefits include gratuity, provident fund (PF) money etc. are received along with the salary at the time of retirement or voluntary retirement scheme (VRS).

Tax Treatment of Retirement Benefits

Retirement benefits are initially taxable as part of salary and it in Form 16 and 26AS.

However, under Section 10 exemptions, these amounts are exempt from tax.

Despite being exempt, these benefits must be declared in the Income Tax Return.

Importance of Showing Retirement Benefits in ITR

If retirement benefits are not shown in the ITR, the Income Tax Department can impose a penalty tax up to 60%.

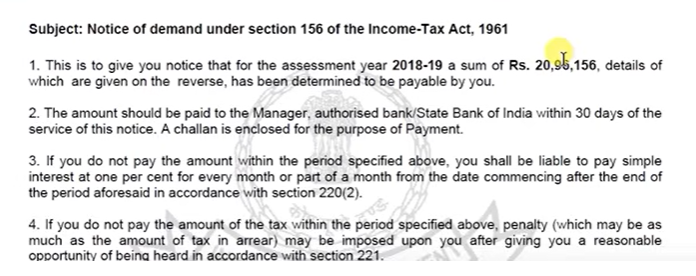

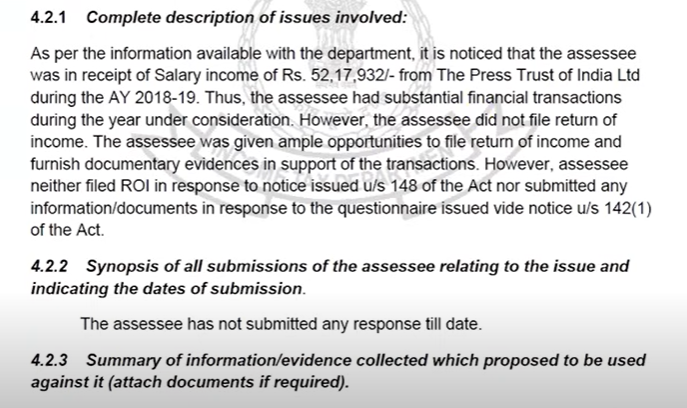

Example case:

A senior citizen who did not show retirement benefits faced a demand of approx. Rs. 21 lakh penalties, despite full tax deduction at source (TDS) being done.

Reason:

A retired individual received ₹52.5 lakh including retirement benefits.

₹9 lakh TDS was already deducted by the employer.

He didn’t file his ITR, assumed that TDS meant nothing further was required.

Consequence

The department issued notices under Section 148 for non-filing.

Key Points To Remember

- Retirement benefits are part of salary and taxable initially.

- Exemptions apply but disclosure in ITR is mandatory.

- Non-disclosure can lead to heavy penalties and tax demands.

Practical Advice for Retirees

Always file ITR and disclose retirement benefits even if fully exempted.

Keep all related documents such as:

- Form 16 showing salary and retirement benefits

- Retirement letter

- Bank statements showing credit of retirement funds

- Proof of gratuity and other retirement credits

This documentation can help you to avoid unnecessary tax demands.

CAclubindia

CAclubindia