Income from the gain on sale of shares was exempt until FY 2017-18. From the current FY 2018-19 the same has become taxable w.e.f 1st April 2018. Therefore, in the upcoming tax filing, the tax will be calculated according to the revised provisions.

The provisions w.r.t to tax on sale of shares has become a little complex due to the transitioning provisions.

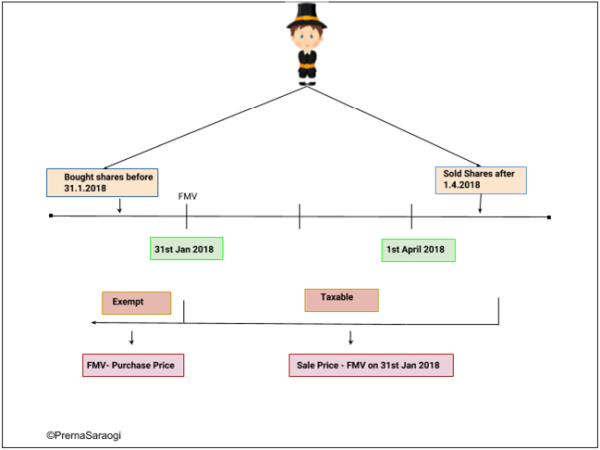

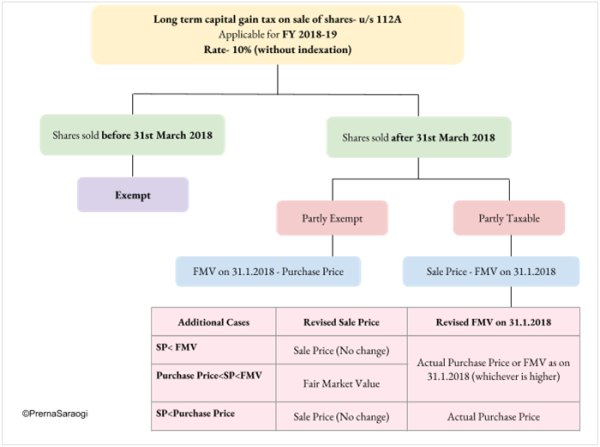

Simply put, it states that if you sell your old shares, by old it means the shares bought before 1.02.2018 before 1.4.2018, then the same shall be exempt under the old provisions. But if you sell it after 1.4.2018 then it shall become taxable at the rate of 10% without indexation.

Revised provisions of Long term Capital Gain Tax on sale of shares u/s 112A

Here, two cases can be seen for the shares bought before 31st January 2018,

- The shares are sold after 31st March 2018

-

The shares are sold before 31st March 2018

We are taking these two cases because the provisions become applicable from 1.4.2018. Let's take up the first case,

1. Shares sold after 31st March 2018

The confusion that usually arises here is when the shares are sold after 1.4.2018, the gain earned from the sale of shares is partially taxable.

What do I mean by partially taxable?

Well, the provision states that, even if you sell an old share after 1.4.2018, the gain that you have earned before the provision was introduced will still remain exempt.

Let's understand it better with an example,

If you see the chart above, it represents a situation wherein if you are holding a share bought before 31st January 2018 and sell it after 31st March 2018, then the entire gain is bifurcated into two sections, part of which is taxable and the other is exempt.

I. Gain until 31st January 2018

The amount of gain earned before 31st January 2018 will be calculated using the Fair Market Value of the share as on date. The amount so arrived at will be exempt from tax.

II. Gain after 31st January 2018 till date of sale

The amount of gain earned after 31st January 2018 till the date of sale will be taxable.

In this case, for taxation purpose, your cost of acquisition is the Fair Market Value as on 31st January 2018, if the shares bought before 31st January 2018 are sold after 31st March 2018.

III. Shares are sold before 31st March 2018

For the shares that are sold before 31st March 2018, but bought before 31st January, there will be no long term capital gain tax, since the provisions haven't been applicable.

Calculation of Long Term Capital Gain Tax on Sale of shares

The long term capital gain on sale of shares is calculated as,

|

Long Term Capital Gain Tax = Sale Price - Purchase Price |

According to the revised provisions, the factors to calculate the gain change based on the date. Let's look at the illustration demonstrated above to understand it better,

Here, the gain is calculated in two parts, one for the exempt part and the other for the taxable part. Now the sale price and purchase price in both the cases is going to be different.

Now, let's have a look at this example,

Case 1:

Say, Mr. X had bought a share worth Rs. 500 on 1st May 2006, and now he wants to sell the same share at Rs. 950 on 1st June 2018. The Fair Market Value of the share as on 31st January was 700

Now, in this case, the gain will be calculated as follows,

Exempt= FMV as on 31st January 2018 (Assumed Sale

Price) - Purchase Price

= 700 - 500 = 200

Therefore, the gain of Rs. 200 is exempt from tax. Let's calculate the taxable

value,

Taxable = Sale Price - FMV as on 31st January 2018

= 950 - 700 = 250

Hence, the taxable amount is Rs. 250

I hope that the calculation part gets a little more clearer here. Now, we will look at the additional provisions of the calculation,

Additional Provisions

Say in the given example above,

Case 2 :

Say, Mr. X had bought a share worth Rs. 500 on 1st May 2006, and now he wants to sell the same share at Rs. 650 on 1st June 2018. The Fair Market Value of the share as on 31st January was 700

Here,

The exempt part would be-

Exempt= FMV as on 31st January 2018 - Purchase

price

= 700 - 500 = 200

And the taxable part would be,

Taxable: Sale Price - FMV as on 31st January 2018

= 650 - 700 = (Loss= 50)

Now, in reality Mr. X is gaining 650-500 = 150

But due to the provisions, he not only gets an exemption of the profit but also books the loss, whereas in actuality there is no loss as the sale price is more than the purchase price.

To curb such a situation, few additional conditions are included in the provisions,

It says, if the selling price is less than the fair market value as on 31st January 2018, then the Fair market value will be assumed as the sale price,

Purchase Price < Sale Price < Fair Market Value as on 31st January 2018 then,

For the purpose of calculating the taxable part, Sale Price = Fair Market Value as on 31st January 2018

Now let's go back to the example above,

Say, Mr. X had bought a share worth Rs. 500 on 1st May 2006, and now he wants to sell the same share at Rs. 650 on 1st June 2018. The Fair Market Value of the share as on 31st January was 700

After this provision,

Although Rs. 200 calculated as the gain becomes exempt, but Rs. 50 will not be booked as loss, Applying the additional provisions,

FMV as on 31st January is less than the sale price, therefore the revised sale price is the FMV, Hence the taxable value is,

Sale Price - FMV as on 31st January 2018

= 700 - 700 = 0

After the revised provision, Mr. X will not be able to book the undue loss.

Similarly, let's assume another case,

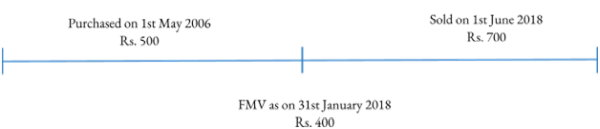

Case 3:

Say, Mr. X had bought a share worth Rs. 500 on 1st May 2006, and now he wants to sell the same share at Rs. 700 on 1st June 2018. The Fair Market Value of the share as on 31st January was 400

In this case, if we go by the normal provisions, the exempt part would be, Exempt= FMV as on 31st January 2018- Purchase Price

= 400 - 500 = (100)

Taxable= Sale Price - FMV as on 31st January 2018

= 700 - 400 = 300 gain Now here if you see,

The actual gain occurred to Mr. X was Rs. 200 (700 - 500)

But due to the provisions, he has to pay tax on additional Rs. 100

To avoid such a situation, for the purpose of calculating the long term capital gain tax, the FMV as on 31st January will be assumed to be the actual purchase price which is Rs. 500 in this case.

Therefore, when the Sale Price> Purchase Price > Fair Market Value i.e. the purchase price is less than the sale price and more than the fair market value, for the purpose of calculating the taxable part, we will assume actual purchase price to be the FMV as on 31st January 2018.

Now after the revised provisions,

Taxable part = Sale Price - FMV as on 31st January

2018

= 700 - 500 = 200

The actual gain that should be taxable is now being taxed.

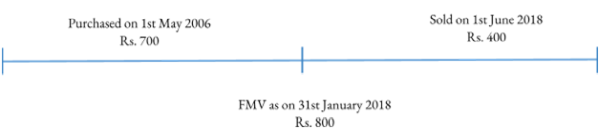

Case 4:

Say, Mr. X had bought a share worth Rs. 700 on 1st May 2006, and now he has to sell the same share at Rs. 400 on 1st June 2018. The Fair Market Value of the share as on 31st January was 800.

Let's look at the calculations under the normal provisions,

Exempt = FMV as on 31st January 2018 - Purchase

Price

= 800 - 700 = 100 gain

Taxable= Sale Price - FMV as on 31st January 2018

= 400 - 800 = 400 loss

Now here, the actual loss that is occurring to Mr. X is, 400 - 700 = 300, but the loss that is booking due to the provisions is Rs. 400. Hence, he is getting the advantage of booking Rs. 100 extra loss.

To avoid this situation, the revised provisions say that, when the sale price of the share is less than the actual purchase price, the fair market value as on 31st January 2018 should be assumed as the actual purchase price which is Rs. 700 instead of the Rs 800.

Therefore, after the revised provisions,

The actual taxable amount shall be, 400 - 700 = 300.

To sum up, the entire provision on long term capital tax on sale of shares is summarized in the chart given below,

CAclubindia

CAclubindia