The word tax has not been specifically defined under any Law, however it simply means compulsory extortion of money by any Government within Constitutional power of the Country. Imposition of tax is necessary for States to collect money for its development activities, sovereign functions and meeting other sovereign objectives. The types of tax systems prevalent across the world are “Direct Taxes” and “Indirect Tax”. Direct Tax, also called as “Corporation Tax”, means the tax which shall be paid by the person on whom it is levied. Indirect Tax is tax levied on the goods or services rather on income of a person. Indirect tax means the tax which is paid by the person other than the person on whom it is levied.

Meaning of VAT

VAT simply means Indirect tax on the domestic consumption of goods and services, except those that are zero-rated (such as food and essential drugs) or are otherwise exempt (such as exports). It is levied at each stage in the chain of production and distribution from raw materials to the final sale based on the value (price) added at each stage. It is not a cost to the producer or the distribution chain members, and whereas its full brunt is borne by the end consumer, it avoids the double taxation (tax on tax) of a direct sales tax. Introduced by the European Economic Community (now the European Union) in the 1970s.

Legal enactment of VAT in UAE:

In line with the said Economic Agreement 2001, based on the decision of Supreme Council of GCC, held in December 2015, and keeping in mind the uniformity in imposition of VAT by the GCC States, the decision to establish a unified legal framework for the introduction of a general tax on consumption in the GCC known as VAT was made. Such agreement is termed as “Common VAT Agreement of the States of the Gulf Cooperation Council (GCC)”, and commonly called as ‘Unified VAT Agreement’ or ‘GCC VAT Framework’.

The GCC Framework contains 15 Chapters consisting of 78 Articles covering different aspect starting from definitions, scope of tax and supplies, place of supply, tax due date, calculation of tax, and value of supply so on. The Framework Agreement provides for various tax treatment of different types of transactions in different circumstances. Though the Framework Agreement covers most of the aspects of VAT law to be implemented in GCC countries, th final law to be implemented by the respective countries will be formulated by them an adopted. In lien with understanding of framework, ‘United Arab Emirates’ & ‘Kingdom of Saud Arabia’ has already finalized their VAT law, whereas other member states are yet to come u with their respective laws. It is expected that other member states will impose the VAT law i the year 2019-2020.

Merits of VAT

Introduction of VAT in UAE:

The United Arab Emirates is a federation of seven emirates which included emirate and local government. The United Arab Emirates does not have any federal Income Tax. The UAE Government implement the VAT (Value Added Tax) in the country from 1st January 2018 with a standard rate of 5%, that too on destination taxation based principal, i.e tax will be levied based destiny of goods or services. That is what the reason the Exports are tax free while Imports are treated at par with domestic products and services.

Factors Leading to introduction of VAT on the basis of GCC:

- GCC Countries have dependent on only oil, the largest revenue contributor to most of these countries economic growth.

- Recent budget included subsidy reforms and plans to diversify the economy to the non-oil sector and reduce wasteful expenditure.

- Due to the anticipation of higher oil prices GCC expect the oil average at USD 45-50/bbl in 2017 but at the November end it would be USD 60/bbl.

- To increase the non-oil sector government introduce the VAT (Value Added Tax) that would be counted as 5% in January 2018. Basically according to IMF revenue for VAT which contributes its 2.1% to the UAE’S GDP. Qatar & Kuwait are expected to generate around 1.1% & 2.1% of GDP.

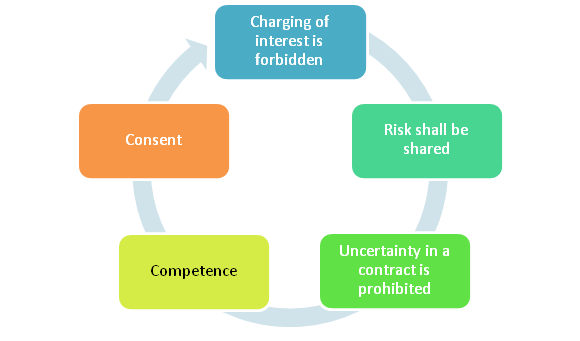

The core principles of VAT Law in UAE are drawn from Sharia Law, most of the legislations are comprised of a mix of Sharia and European concepts of civil law. The principles of Sharia Law are applicable to business transactions and have influenced the development of the commercial code. These principles have influenced the drafting and interpretation of laws in the UAE.

Five Core Principles of Sharia Law:

Features of UAE VAT:

Registration Criteria:

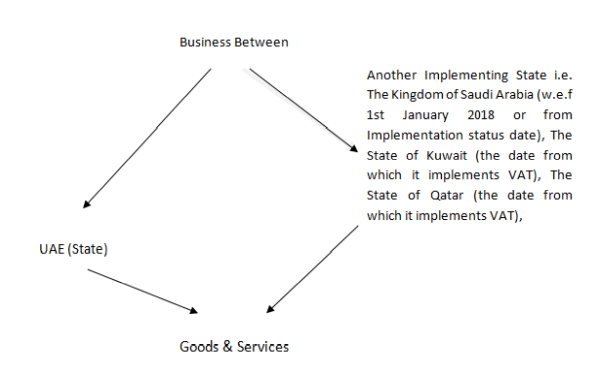

- Each person making supply who has place of residence in the State or in any other implementing states is required to obtain registration if value of aggregate supplies made by him in the state (as per place of supply) exceed compulsory registration threshold of AED 375,000 in preceding 12 months.

- A business may choose voluntarily to register under VAT if their taxable supplies and imports are less than the registration threshold, but exceed the voluntary registration threshold of AED 187,500.

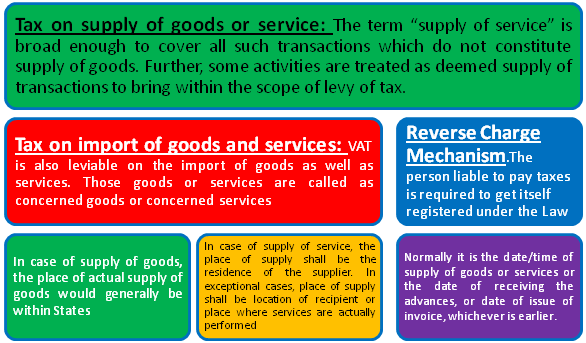

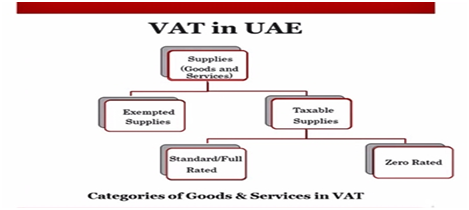

Zero- Rated Items in UAE VAT law:

VAT will be charged at 0% on the following categories of supplies, but corresponding input tax may be recovered and claim as refund:

- International transportation and related supplies.

- Supplies of certain sea, air and land means of transportation such as aircraft, spaceship etc.

- Supply of certain Healthcare Services and supply of relevant goods and services.

- Supply of certain Education Services and supply of relevant goods and services.

- Certain investment in gold and silver or precious metals.

- Newly constructed residential properties that are supplied for the first time within 3 years of their Construction.

- Exports of goods and services to outside the GCC.

Exemptions under VAT Law:

- Basic healthcare services.

- The supply of some financial services.

- Transactions of Bare land and Local passenger transport.

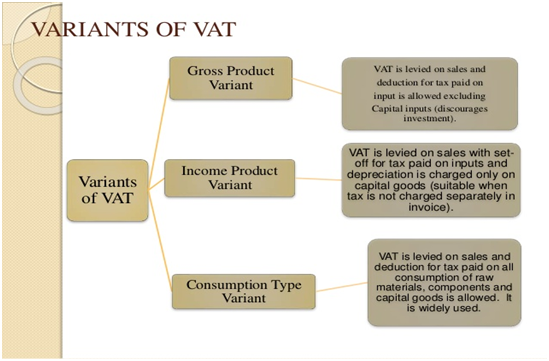

Variants of VAT:

VAT is divided into three variants such as gross product variants, income variants and consumption variants. They are distinguished on the basis of their methods of calculation, addition method, invoice method and subtraction method.

1. Gross Product Variants :

- Allows deduction on all purchases of raw material and components but not for capital inputs, i.e taxes on capital goods such as plant and machinery are not deductible from the tax base in the year of purchase.

- No deduction for the depreciated part of the plant and machinery in the base year.

- The economic base of Gross Product Variant is same as to Gross National Product.

- Tax on capital goods is not refunded then it is called Gross Product Variants.

- In this variant of VAT, capital goods carry a heavier tax burden as they are taxed twice at the time they are purchased and also when the products they produce are sold to consumers. Thus Capital goods carry a heavier tax burden because they are taxed twice and Modernization and upgrading of plant and machinery is delayed due to this double tax treatment.

2. Income Variant :

- Allows deduction on purchase on raw material, components, and depreciation on capital goods. In other words, the input tax credit for capital goods is not refunded straightway but is refunded in accordance with the depreciation schedule similar to the one used for income tax purposes.

- Income Variant is same as the Net National Product.

- Methods of measuring depreciation depend on the life of an asset and on the rate of inflation.

3. Consumption Variant :

- This is the most popular variant which is worldwide accepted, since it does not affect decisions regarding investment because the tax on capital goods is also available for set-off against the VAT liability. Hence, the system is tax neutral in respect of techniques of production (labour or capital-intensive).

- In the foreign-trade sector, this variant relieves all exports from taxation while imports are taxed.

- The consumption variant is convenient from the point of administrative expediency since the business gets set-off for the tax on services, it does not cause any cascading effect.

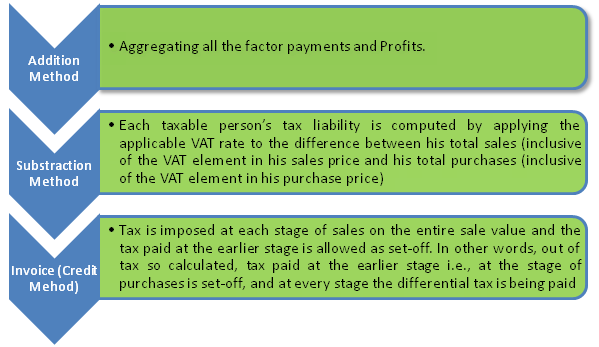

Methods for Computation of VAT:

Disclaimer

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, Or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, Or otherwise without prior permission, in writing, from the publisher.

The author can also be reached at cadeepakbharti@yahoo.com.

CAclubindia

CAclubindia