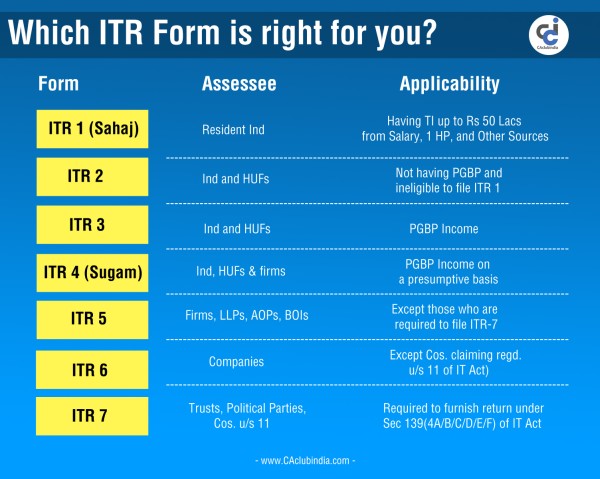

Which ITR form is right for you? The ultimate guide on ITR forms for AY 18-19

It is that time of the year when we all have to take out time to file the Income tax returns for the previous year. The due date to file return is 31st July 2018 for the individuals. So do not delay it any further and grab your Form 16, Investment and saving certificates, Form 26AS etc. CBDT has already notified and released around seven ITR forms for the A.Y. 18-19. Out of the these ITR forms, four ranging from ITR -1 to ITR - 4 are for the individual assessees. The form applicable to you depends upon many factors like the income level, the sources of income, residential status of the assessee, location of assets etc.

It is very important to furnish the correct ITR form as filing the wrong form may lead to your return being declared invalid or defective by the department. So this article will guide you on the correct ITR form which will be applicable on.

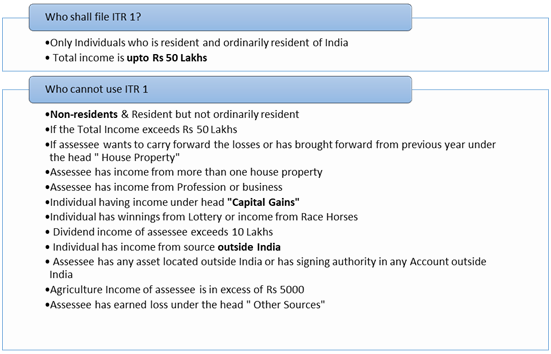

ITR-1 SAHAJ

ITR 1 - Sahaj, as the name suggests is the simplest of the seven forms which is created for the highest proportion of taxpayers who are salaried or draw pension and have income from maximum one house property and their other incomes comprise of mostly interest from deposits.

CHANGES INTRODUCED IN THE FORM FOR AY 2018-19

- The new forms introduced for AY 2018-19 require disclosure of break up of salary into different components.

- Last year's ITR-1 was applicable on all individuals, whether resident or non-resident. However, this year' ITR-1 can be filed only by a resident individual. So non-residents and RNOR individuals shall have to opt for the ITR-2.

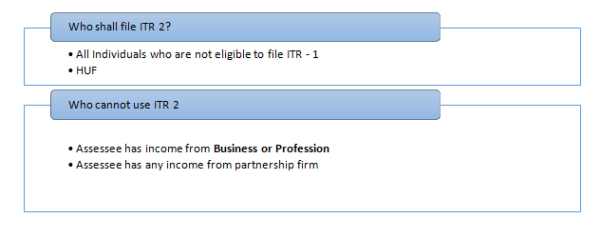

ITR-2

- ITR 2 is the form for those individuals who are not eligible to file ITR-1.

- ITR-2 can be furnished by HUFs also.

- Those individuals or HUFs who are either having business income or are partners in any partnership firm or AOP are not eligible to file ITR 2 and shall have to file either ITR-3 or ITR-4.

ITR-3

- ITR - 3 is the form for those individuals and HUFs who have income from business and profession apart from income from other heads.

- In ITR - 3, all individuals who are engaged in business or profession are required to disclose details relating to GST such as GSTIN, turnover declared in GST return etc

- All individuals who are partners in any firm or AOP shall also have to furnish ITR - 3 from AY 2018-19 onwards.

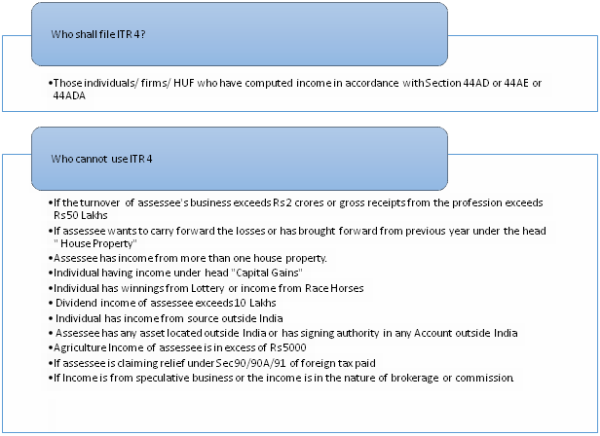

ITR-4 - SUGAM

- ITR - 4 is applicable on all those individuals, HUF and firms which have opted for taxation on presumptive basis as per Sec 44AD or 44ADA or 44AE etc. of the Income Tax Act.

- Assessees can also have income from the heads - salary, house property and other sources

- ITR 4S form which existed earlier has been withdrawn by the department and thus not applicable this year.

ITR 5

This form is applicable for:

- Firms

- LLPs

- AOPs

- BOIs

- Artificial Juridical Person

- Cooperative Societies

- Registered Societies

- Local authority

However, a person who is required to file the return of income under section 139(4A) or 139(4B) or 139(4C) or 139(4D) or 139(4F) shall not use this form as they are required to file ITR-7

ITR 6

- All companies (other than those companies functioning for charitable or religious purpose which have claimed exemption u/s 11 of Income Tax Act 1961) shall file ITR - 6

ITR 7

- All persons (including companies) which are required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) or section 139(4E) or section 139(4F) of the Income Tax Act 1961 shall file ITR 7

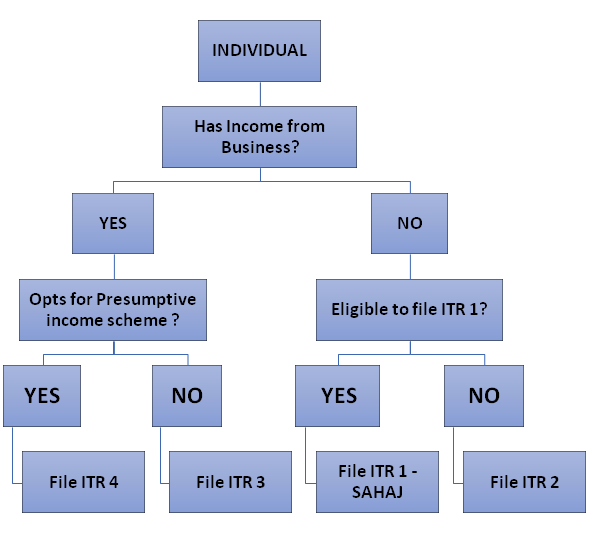

TO SUM UP:

CAclubindia

CAclubindia