Introduction

The Goods and Services Tax (GST) law provides for various types of assessments to ensure proper determination of tax liability and compliance. This article aims to provide a simple and practical understanding of the different types of assessments under GST. This article will cover the types of assessments, their legal provisions and the situations in which they apply.

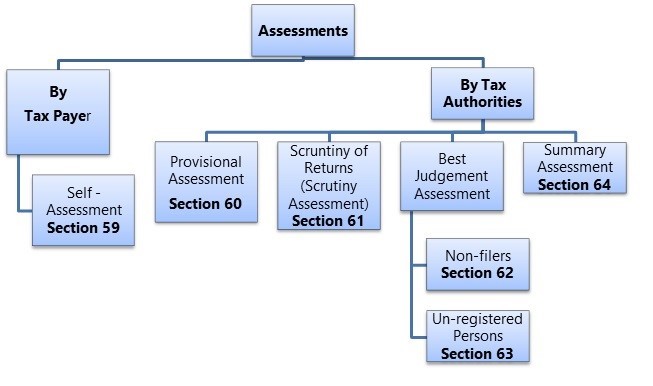

Assessments under GST

Section -59 - Self Assessment

Every registered person shall self-assess the taxes payable under this Act and furnish a return for each tax period as specified under section 39 (regular returns).

Section -60 - Provisional Assessment

60(1)

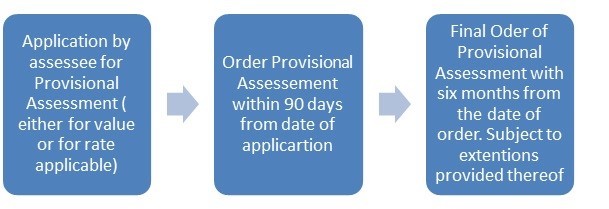

Subject to sub-section (2), If a taxable person is unable to determine the value of goods or services or the applicable tax rate, they can make a written request to the proper officer explaining the reasons for wanting to pay taxes on a provisional basis.

The proper officer must then issue an order within a maximum of ninety days from the receipt of the request. This order will allow the taxable person to pay taxes on a provisional basis, specifying the rate or value determined by the officer.

60(2)

To be eligible for payment of tax on a provisional basis, the taxable person must fulfill an additional requirement. They need to execute a bond, as prescribed, which includes providing surety or security as determined appropriate by the proper officer. This bond binds the taxable person to pay the difference between the amount of tax provisionally assessed and the amount of tax finally assessed. In other words, it ensures that the taxable person will settle any additional tax liability once the final assessment is determined.

60(3)

The proper officer is required to issue the final assessment order within a maximum of six months from the date of communication of the order issued in sub-section (1). During this process, the officer will consider any necessary information needed to finalize the assessment.

However, in certain circumstances, the specified period can be extended. The Joint Commissioner or Additional Commissioner can grant an extension of up to six months if sufficient cause is shown and the reasons are recorded in writing. Furthermore, the Commissioner has the authority to extend the period for a further period not exceeding four years if deemed necessary.

60(4) - Interest payable on Provisional Assessment

If a registered person is liable to pay taxes on the supply of goods or services under provisional assessment but fails to pay them by the specified due date mentioned in sub-section (7) of section 39 or the related rules, they will be subject to paying interest. The interest rate applicable will be the rate specified in sub-section (1) of section 50.

Interest will be calculated from the day immediately following the due date for tax payment in relation to the specific supply of goods or services until the actual date of payment. This applies regardless of whether the payment is made before or after the issuance of the final assessment order.

60(5) - Refund payable on Provisional Assessment

If a registered person is eligible for a refund consequent to final assessment order under sub-section (3), they are entitled to receive interest on the refund amount. The payment of interest on the refund is governed by the provisions specified in section 56, subject to the conditions mentioned in sub-section (8) of section 54.

Related Rules - 98

Rule 98 outlines the procedure to be followed for applying for Provisional Assessment

1. Registered person submits an application (FORM GST ASMT-01) along with supporting documents for provisional tax payment. [98 Sub-rule 1]

2. Proper officer may issue a notice (FORM GST ASMT-02) requesting additional information or documents. [98 Sub-rule 2]

3. Registered person responds to the notice by filing a reply (FORM GST ASMT-03) and may appear in person if desired. [98 Sub-rule 2]

4. Proper officer may issues an order (FORM GST ASMT-04) allowing provisional tax payment, specifying the value or rate, and the amount for which a bond and security are required. [98 Sub-rule 3]

5. Registered person executes a bond (FORM GST ASMT-05) and provides a security (bank guarantee) as determined by the officer. [98 Sub-rule 4]

6. Proper officer issues a notice (FORM GST ASMT-06) to gather information and records for the final assessment. [98 Sub-rule 5]

7. Proper officer issues a final assessment order (FORM GST ASMT-07) specifying the amount payable or refundable. [98 Sub-rule 5]

8. Applicant can file an application (FORM GST ASMT-08) for the release of the security after receiving the final assessment order. [98 Sub-rule 6]

9. Proper officer releases the security after confirming payment and issues an order (FORM GST ASMT-09) within seven working days of receiving the application. [98 Sub-rule 7]

Note: FORM ASMT 01 to ASMT-09 for Provisional Assessment.

Section 61 - Scrutiny of Returns filed

60(1) - The proper officer has the authority to review the return and related details provided by a registered person to ensure its accuracy. If any discrepancies are identified, the officer will inform the registered person of these discrepancies in the prescribed manner and request an explanation.

According to section 61(2), if the explanation provided by the registered person is deemed acceptable by the proper officer, the person will be notified accordingly, and no further action will be taken in relation to the discrepancies.

However, as per section 61(3), if the registered person fails to provide a satisfactory explanation within thirty days of being informed by the officer (or any permitted extension), or if the registered person accepts the discrepancies but fails to correct them in their subsequent return, the proper officer may initiate appropriate actions. These actions can include actions under section 65, section 66, or section 67, or proceeding to determine the tax and other dues under section 73 or section 74.

Connected Rule 99

Rule 99 Sub-Rule 1

If a return filed by a registered person is selected for scrutiny, the concerned officer will examine it based on the information available. If any discrepancies are found, the officer will issue a notice (FORM GST ASMT-10) to the person, informing them about the discrepancies and requesting an explanation within thirty days or a longer period if permitted. The notice may also specify the amount of tax, interest, and any other payments related to the discrepancies if possible.

Rule 99 Sub-Rule 2

The registered person has the option to either accept the discrepancies mentioned in the notice and make the required payments (tax, interest, etc.), or provide an explanation for the discrepancies by submitting FORM GST ASMT-11 to the officer.

Rule 99 Sub-Rule 3

If the explanation provided by the registered person or the information submitted in FORM GST ASMT-11 is considered acceptable, the officer will inform the person accordingly through FORM GST ASMT-12.

Note: Form ASMT 10 to ASMT 12 - Scrutiny Assessment.

Section 62-63 - Best Judgement Assessment

Section 62 - For Non-Filers of GST Returns

62(1) - In cases where a registered person fails to submit the required return under section 39 (Regular Returns) or section 45 (final Returns), even after receiving a notice under section 46, the proper officer has the authority to assess the tax liability of that person based on their best judgement. The officer will consider all relevant available material or information gathered and issue an assessment order.

It is important to note that this section, overrides the provisions stated in section 73 or section 74. The assessment order must be issued within a period of five years from the date specified under section 44 (Annual Return) for the submission of the annual return related to the financial year for which the tax was not paid.

62(2) - If a registered person submits a valid return within thirty days of receiving the assessment order mentioned in sub-section (1), the assessment order will be considered withdrawn. However, it's important to note that the liability for payment of interest as per sub-section (1) of section 50 (related to late payment of taxes) and the late fee as per section 47 will still apply. In other words, even if the assessment order is withdrawn, the person is still responsible for paying any applicable interest and late fees.

Rule 100 sub rule 1 - The order of assessment made under sub-section (1) of section 62 shall be issued in FORM GST ASMT-13 and a summary thereof shall be uploaded electronically in FORM GST DRC-07.

Section 63 - For Unregistered Person

In cases where a taxable person fails to obtain registration despite being liable to do so, or their registration has been cancelled under sub-section (2) of section 29 but they were still liable to pay tax, the proper officer has the authority to assess their tax liability to the best of their judgement. This assessment will be carried out for the relevant tax periods. The officer will issue an assessment order within a period of five years from the date specified under section 44 (Annual Return) for the submission of the annual return corresponding to the financial year for which the tax was not paid.

However, it is important to note that before passing such an assessment order, the person in question must be given an opportunity to be heard. This ensures that they have a chance to present their case or provide any relevant information before the assessment order is finalized. It is important to note that this section, overrides the provisions stated in section 73 or section 74.

Rule 100 sub-rule 2 - The proper officer shall issue a notice to a taxable person in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and shall also serve a summary thereof electronically in FORM GST DRC-01, and after allowing a time of fifteen days to such person to furnish his reply, if any, pass an order in FORM GST ASMT-15 and summary thereof shall be uploaded electronically in FORM GST DRC-07.

Section 64 - Summary Assessment

Summary assessment is in the nature of protective assessment. It is procedure where quick and fast assessment of tax liability is made. Section 64 deals with summary assessment in certain special cases to protect the interest of the revenue. It gives special powers, in exceptional circumstances, to the proper officer to assess tax without giving any notice or opportunity of hearing.

According to section 64(1), the proper officer, with the prior permission of the Additional Commissioner or Joint Commissioner, can initiate an assessment of tax liability for a person based on any evidence indicating their tax liability. This assessment is done to protect the interests of revenue. If the officer has reasonable grounds to believe that any delay in assessing the tax liability may harm revenue, they can issue an assessment order.

However, in cases where the taxable person responsible for the liability cannot be identified and the liability pertains to the supply of goods, the person in charge of those goods will be treated as the taxable person liable to be assessed and pay the tax and any other amount due under this section.

Rule 100 Sub-rule 3 - The order of assessment of section 64(1) shall be issued in FORM GST ASMT-16 and a summary of the order shall be uploaded electronically in FORM GST DRC-07.

Furthermore, as per section 64(2), if the taxable person receives an order under sub-section (1), they have the option to apply within thirty days to the Additional Commissioner or Joint Commissioner for withdrawal of the order. The Additional Commissioner or Joint Commissioner, if they find the order to be erroneous, can withdraw it and proceed with the assessment procedure outlined in section 73 or section 74.

Rule 100 Sub-rule 4 - The person referred to in section 64(2) may file an application for withdrawal of the assessment order in FORM GST ASMT-17.

Rule 100 Sub-rule 5 - The order of withdrawal or, as the case may be, rejection of the application under sub-section (2) of section 64 shall be issued in FORM GST ASMT-18.

SUMMARY OF ASSESSMENT

|

S. No. |

Type of Assessment |

Section |

By Whom |

When Initiated |

Key Features |

Relevant Forms |

|

1 |

Self-Assessment |

59 |

Registered Taxpayer |

Every registered person for each tax period |

- Self-assessment of tax liability- Filing of return under Section 39 |

- |

|

2 |

Provisional Assessment |

60 |

Proper Officer |

When the taxpayer is unable to determine value/rate |

- Written request required (ASMT-01)- Provisional order in 90 days- Bond + security needed- Final order in 6 months (extendable up to 4 yrs) |

ASMT-01 to ASMT-09 |

|

3 |

Scrutiny of Returns |

61 |

Proper Officer |

On noticing discrepancies in returns filed |

- ASMT-10 issued for explanation- Accept or clarify via ASMT-11- Closure via ASMT-12 or move to audit/demand |

ASMT-10 to ASMT-12 |

|

4 |

Best Judgment - Non-filers |

62 |

Proper Officer |

If a return is not filed even after Sec 46 notice |

- Officer estimates tax liability- ASMT-13 issued- If return filed within 30 days → order withdrawn |

ASMT-13, DRC-07 |

|

5 |

Best Judgment - Unregistered |

63 |

Proper Officer |

Person liable to register but didn't or continued taxable activity after cancellation |

- Opportunity of hearing required- ASMT-14 notice → ASMT-15 order |

ASMT-14, ASMT-15, DRC-01, DRC-07 |

|

6 |

Summary Assessment |

64 |

Proper Officer (with JC/ADC approval) |

In special cases to protect the interest of revenue |

- No prior notice required- Officer can act immediately if delay may harm revenue- Order can be withdrawn by JC/ADC |

ASMT-16 to ASMT-18, DRC-07 |

CAclubindia

CAclubindia