Introduction

A provident fund is created with a purpose of providing financial security and stability to elderly people. Generally one contributes in these funds when one starts as employee, the contributions are made on a regular basis. Its purpose is to help employees save a fraction of their salary every month, to be used in an event that the employee is temporarily or no longer fit to work or at retirement.

|

SCHEME NAME |

EMPLOYEE CONTRIBUTION (%) |

EMPLOYER CONTRIBUTION (%) |

|

EPF |

12 |

3.67 |

|

EPS |

0 |

8.33 |

|

EDLI |

0 |

0.5 |

|

EPF ADMIN CHARGES |

0 |

0.85 |

|

PF ADMIN CHARGES |

0 |

1.1 |

|

EDLIS ADMIN CHARGES |

0 |

0.01 |

Whether Contribution by Employee Is Mandatory

Employees Drawing basic salary up to Rs 15000 has to compulsory contribute to the Provident fund.Employee who while joining the organisation has a basic salary above Rs 15001/- have an option to either become or avoid becoming member of Provident fund but employees whose basic salary while joining the organisation is less then Rs 15001/- but after some period of time their basic increases above Rs 15001/- have to compulsorily continue to be member of provident Fund.

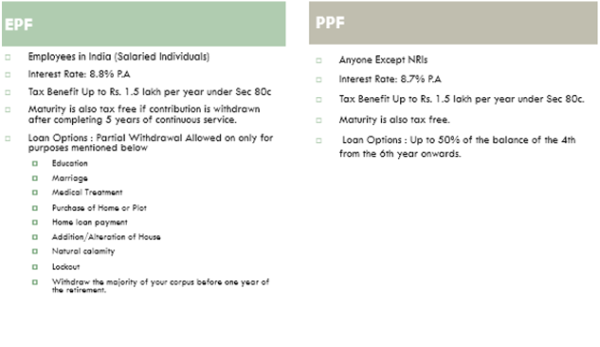

EPF V/S PFF

FAQ’S

Can contribute more than 12% towards EPF?

As per EPF Act, 1952, the minimum contribution of employee towards EPF account should be at least 12% but one can contribute up to 100% of your salary plus DA on voluntary basis but remember this does not bound employer to contribute more

What If Change Job?

a. At such times, the PF balance could be transferred from one employer to another. The existing balance would continue to stay, with fresh contributions made by the new employer.

b. When you quit your job, PF could be withdrawn. You need to provide a declaration that you do not intend to work for the next six months.

Withdrawal from Provident Fund (PF) Account before Completion of Five years taxable?

a. Maturity is also tax free if contribution is withdrawn after completing 5 years of continuous service.

b. The employer’s contribution and interest, thereon, would be fully taxable Under the head Salary

c. The employee’s contribution would be taxable to the extent of deduction claimed under Section 80C, if any, under the Income-tax Act,1961 andThe interest earned on employee’s total contributions would be taxable as ‘income from other sources’ in the hands of the employee.

d. TDS Will be deducted if at the time of payment of the accumulated PF balance is more than or equal to Rs 50,000 with service less than 5 years. Besides, it will not attract TDS if the employee is terminated from service due to ill health of member and discontinuation or contraction of business by employer.

CAclubindia

CAclubindia