The sector that is making most to the headlines today is the Banking Sector .The best part of the unfolding of events has been the quantification of NPA’s in the banking system .With numbers as high Rs.3,61,731 crores as reported NPA’s in March 2015 to write off of Rs.1.14 lakh crores of NPA’s by 29 PSB’s between FY 2013 and FY 2015. I believe that this is also a part of “स्वच्छ भारत अभियान” wherein our banking system is getting cleaned up. Such a historic event always makes a smart investor to search for some good bets which can be multibagger’s. In this article, I have tried to do some data analysis for the same .Hope it might be useful to you all. However, I have limited the scope of the paper to Valuation Only , whereas we all know that there are many other aspects one has to look in before investing; like fundamentals of the company timing of investing ,risk appetite of the client, investment horizon etc

I. Introduction -

We all are aware that basically there are following four methods of corporate valuation –

1. Asset Based Valuation Approach – The key factor in this approach is Net Asset Value or Book Value wherein Book Value is the residual value of Assets of the business after paying all the liabilities. Various corollaries of this method are Net Asset Value (Adjusted), Net Asset Value ( Replacement Value ), Liquidation Value

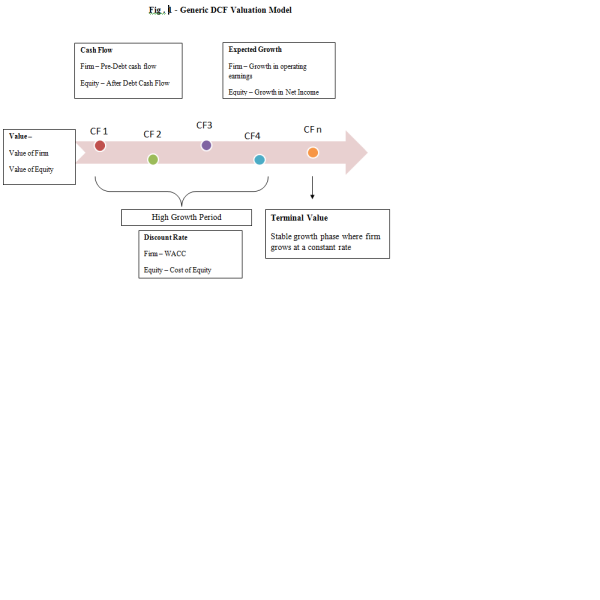

2. Discounted Cash Flow Method (DCF) - In DCF approach , we sum the present value of the unlevered or levered free cash flows (either FCFE i.e. Free Cash Flows to equity or FCFF i.e. Free cash flows to firm) and add that to the present value of the terminal value; in a dividend discount model, we sum the present value of the dividends and add that to the present value of the terminal value .So basically we have three variables i.e. Cash Flow, Discounting factor and growth rate .

3. Relative Valuation Approach - In this approach the value of the asset is compared with the value of similar other assets in the market .To do relative valuation –

- We need to Identify comparable assets and obtain market value of those assets

- As absolute prices cannot be compared we need to convert market values into standardised value so as to derive price multiples

- We need to compare the multiple with the standardised value of similar assets to determine whether the asset is undervalued , overvalued or properly valued

4. Contingent Claim Valuation Approach – One of the most significant development in valuation is the acceptance, at least in some cases, that the value of an asset may not be greater than the present value of expected cash flows if the cash flows are contingent on the occurrence or non-occurrence of an event. This acceptance has largely come about because of the development of option pricing models like the Binomial Model and BSOPM . While these models were initially used to value traded options, there has been an attempt, in recent years, to extend the reach of these models into more traditional valuation. There are many who argue that assets such as patents or undeveloped reserves are really options and should be valued as such, rather than with traditional discounted cash flow models.

II. Valuation of a Bank –

The most acceptable approach for bank valuation is the P/BV (Relative Valuation) approach .In case of a bank we use metrics like Total Assets rather than EBTIDA to determine the size of the bank . Book Value multiples are thought to be more reliable than P/E multiples because non-recurring and non-cash charges can affect earnings; also, Book Value multiples are linked closely to ROE, which is the key operating metric for a bank.

This makes sense as : if a company expects to earn a higher return on its capital (shareholders’ equity), it should be valued at a premium to that capital. But if it earns a lower or less-than-expected return on its capital, it should be valued at a discount to that capital.

III. Primary Research –

Data-

- The research universe has in all 35 banks including 21 public sector banks (PSB) and 14 private sector banks

- The model uses weekly price changes for 157 weeks i.e. three years from 13/6/2013 to 13/6/2016 .

- The ROE and P/BV are as on March 2016 .

Data source –

- Historical Prices of shares are taken from yahoo finance

- ROE and P/BV have been taken from way2wealth.com

Objective of research –

- To find out which shares are undervalued , overvalued and properly valued

- To find out a working relationship between ROE , Standard Deviation (taken as a proxy for risk ) and P/BV so as to find a fair relative value of the stock

IV. Analysis of Bank

The rules for undervaluation and overvaluation are –

- Undervalued shares – Shares traded at a P/BV which is below median P/BV , has higher ROE than the median ROE and has lower SD than median SD

- Overvalued shares - Shares traded at a P/BV which is above median P/BV , has lower ROE than the median ROE

Part A – Public Sector banks

Table 1 –Public Sector Banks

|

Sr.No |

Bank Name |

PBV |

ROE |

SD |

|

1 |

Allahabad Bank |

0.35 |

5.02% |

0.06176 |

|

2 |

Andhra Bank |

0.36 |

5.02% |

0.06002 |

|

3 |

Bank of Baroda |

0.84 |

0.00% |

0.3444 |

|

4 |

Bank of India |

0.31 |

6.18% |

0.06654 |

|

5 |

Bank of Maharashtra |

0.53 |

6.53% |

0.04757 |

|

6 |

Canara Bank |

0.48 |

10.57% |

0.06467 |

|

7 |

Central Bank of India |

1.19 |

4.18% |

0.05917 |

|

8 |

Corporation Bank |

0.38 |

5.44% |

0.34322 |

|

9 |

Dena Bank |

0.34 |

0.00% |

0.05683 |

|

10 |

IDBI Bank Limited |

0.75 |

4.14% |

0.06478 |

|

11 |

Indian Bank |

0.52 |

8.22% |

0.06973 |

|

12 |

Indian Overseas Bank |

0.36 |

0.00% |

0.05428 |

|

13 |

Oriental Bank of Commerce |

0.27 |

1.16% |

0.07478 |

|

14 |

Punjab & Sind Bank |

0.33 |

5.62% |

0.05626 |

|

15 |

Punjab National Bank |

0.5 |

7.98% |

0.34099 |

|

16 |

State Bank of India |

0.94 |

10.53% |

0.80088 |

|

17 |

Syndicate Bank |

0.43 |

0.00% |

0.06786 |

|

18 |

UCO Bank |

0.42 |

0.00% |

0.0604 |

|

19 |

Union Bank of India |

0.43 |

9.52% |

0.07715 |

|

20 |

United Bank of India |

0.45 |

4.89% |

0.066 |

|

21 |

Vijaya Bank |

0.6 |

5.84% |

0.04527 |

|

Average |

0.513 |

4.8% |

13.7% |

|

|

Median |

0.43 |

5.02% |

6.48% |

Conclusion from the above table -

Any smart investor will like to buy a undervalued stock which has higher return potential and lower risk .This means in the above case a investor will like to invest in a stock whose P/BV is less than 0.43 ( median value ) , while having a ROE of more than 5.02% ( median value ) and having a standard deviation of less than 6.48% ( median value ) .Say a bank like Punjab and Sind Bank with a P/BV of 0.33 , ROE of 5.62% and SD of 5.6% .A typical investor may also chose Union Bank of India Bank with a P/BV of 0.43 , ROE of 9.52% and SD of 7.7 %.However , Central Bank of India is not a good stock to invest as it has a PBV of 1.19 ( more than median of 0.43 ) and ROE is 4.8% ( lower than median of 5.02%)

Part B – Private Sector Banks

Table 2 –Private Sector Banks

|

Sr.No |

Bank Name |

PBV |

ROE |

SD |

|

1 |

City Union Bank Ltd. |

2.43 |

14.65% |

0.03626 |

|

2 |

Dhanlaxmi Bank Ltd |

0.81 |

0.00% |

0.06683 |

|

3 |

The Federal Bank Ltd. |

1.27 |

17.73% |

0.10391 |

|

4 |

The Karnataka Bank Ltd. |

0.77 |

13.32% |

0.0557 |

|

5 |

The Karur Vysya Bank Ltd. |

1.24 |

10.93% |

0.03716 |

|

6 |

The Lakshmi Vilas Bank Ltd. |

1.04 |

11.32% |

0.04255 |

|

7 |

RBL Bank |

2.01 |

13.23% |

0.07235 |

|

8 |

The South Indian Bank Ltd. |

0.72 |

8.97% |

0.03881 |

|

9 |

Axis Bank Ltd. |

2.76 |

16.56% |

0.32054 |

|

10 |

HDFC Bank Ltd. |

4 |

16.92% |

0.02644 |

|

11 |

ICICI Bank Ltd. |

1.65 |

14.45% |

0.34009 |

|

12 |

Indusind Bank Ltd. |

6.31 |

13.20% |

0.04174 |

|

13 |

Kotak Mahindra Bank Ltd. |

6.19 |

10.36% |

0.09547 |

|

14 |

YES Bank |

3.88 |

18.38% |

0.06348 |

|

Average |

2.51 |

12.86% |

9.58% |

|

|

Median |

1.83 |

13.28% |

5.96% |

Conclusion from the above table -

Any smart investor will like to buy a undervalued stock which has higher return potential and lower risk .This means in the above case a investor will like to invest in a stock whose P/BV is less than 1.83 ( median value ) , while having a ROE of more than 13.28% ( median value ) and having a standard deviation of less than 5.96% ( median value ) .Say a bank like Karnataka Bank with a P/BV of 0.77 , ROE of 13.32% and SD of 5.6% is a good investment bet.

Table 3 – All the Banks together

|

Sr.No |

Bank Name |

PBV |

ROE |

SD |

|

1 |

Allahabad Bank |

0.35 |

5.02% |

0.06176 |

|

2 |

Andhra Bank |

0.36 |

5.02% |

0.06002 |

|

3 |

Bank of Baroda |

0.84 |

0.00% |

0.3444 |

|

4 |

Bank of India |

0.31 |

6.18% |

0.06654 |

|

5 |

Bank of Maharashtra |

0.53 |

6.53% |

0.04757 |

|

6 |

Canara Bank |

0.48 |

10.57% |

0.06467 |

|

7 |

Central Bank of India |

1.19 |

4.18% |

0.05917 |

|

8 |

Corporation Bank |

0.38 |

5.44% |

0.34322 |

|

9 |

Dena Bank |

0.34 |

0.00% |

0.05683 |

|

10 |

IDBI Bank Limited |

0.75 |

4.14% |

0.06478 |

|

11 |

Indian Bank |

0.52 |

8.22% |

0.06973 |

|

12 |

Indian Overseas Bank |

0.36 |

0.00% |

0.05428 |

|

13 |

Oriental Bank of Commerce |

0.27 |

1.16% |

0.07478 |

|

14 |

Punjab & Sind Bank |

0.33 |

5.62% |

0.05626 |

|

15 |

Punjab National Bank |

0.5 |

7.98% |

0.34099 |

|

16 |

State Bank of India |

0.94 |

10.53% |

0.80088 |

|

17 |

Syndicate Bank |

0.43 |

0.00% |

0.06786 |

|

18 |

UCO Bank |

0.42 |

0.00% |

0.0604 |

|

19 |

Union Bank of India |

0.43 |

9.52% |

0.07715 |

|

20 |

United Bank of India |

0.45 |

4.89% |

0.066 |

|

21 |

Vijaya Bank |

0.6 |

5.84% |

0.04527 |

|

22 |

City Union Bank Ltd. |

2.43 |

14.65% |

0.03626 |

|

23 |

Dhanlaxmi Bank Ltd |

0.81 |

0.00% |

0.06683 |

|

24 |

The Federal Bank Ltd. |

1.27 |

17.73% |

0.10391 |

|

25 |

The Karnataka Bank Ltd. |

0.77 |

13.32% |

0.0557 |

|

26 |

The Karur Vysya Bank Ltd. |

1.24 |

10.93% |

0.03716 |

|

27 |

The Lakshmi Vilas Bank Ltd. |

1.04 |

11.32% |

0.04255 |

|

28 |

RBL Bank |

2.01 |

13.23% |

0.07235 |

|

29 |

The South Indian Bank Ltd. |

0.72 |

8.97% |

0.03881 |

|

30 |

Axis Bank Ltd. |

2.76 |

16.56% |

0.32054 |

|

31 |

HDFC Bank Ltd. |

4 |

16.92% |

0.02644 |

|

32 |

ICICI Bank Ltd. |

1.65 |

14.45% |

0.34009 |

|

33 |

Indusind Bank Ltd. |

6.31 |

13.20% |

0.04174 |

|

34 |

Kotak Mahindra Bank Ltd. |

6.19 |

10.36% |

0.09547 |

|

35 |

YES Bank |

3.88 |

18.38% |

0.06348 |

|

Average |

1.31 |

8.02% |

12.07% |

|

|

Median |

0.72 |

7.98% |

6.47% |

Conclusion from the above table –

As W.Sharpe rightly said “If you torture the data too much it will confess any crime “.Even though it is statistically possible to get median P/BV , ROE and SD for all the banks combined together , it will be logically incorrect to club them into one , as we follow the relative approach of valuation where we need comparable assets and I strongly believe that the quality of assets and liabilities of PSB banks are not comparable with Private Sector Banks .Hence we need not go in depth of table no – 3

The Regression Model –

We are looking for stocks that are traded at low P/BV ratios while giving higher ROE. The big question here is what do we mean by low P/BV and high ROE .Here two separate regression’s are run on the two samples of PSB and Private Sector Banks .I have regressed P/BV against ROE and SD ( the proxy for risk ) .The results are as under –

For PSB’s –

P/BV = 0.43 +0.16*ROE+0.53*SD

For Private sector banks –

P/BV = 1.14 +12.31*ROE+2.26*SD

With the use of above regression equations we can have the following predictions –

Table No – 4 Predicted P/BV of Public Sector Banks

|

Sr.No |

Bank Name |

PBV |

ROE |

SD |

Predicted P/BV |

- Undervaluation /Overvaluation % |

|

1 |

Allahabad Bank |

0.35 |

5.02% |

6.2% |

0.47 |

-35% |

|

2 |

Andhra Bank |

0.36 |

5.02% |

6.0% |

0.47 |

-31% |

|

3 |

Bank of Baroda |

0.84 |

0.00% |

34.4% |

0.61 |

27% |

|

4 |

Bank of India |

0.31 |

6.18% |

6.7% |

0.48 |

-53% |

|

5 |

Bank of Maharashtra |

0.53 |

6.53% |

4.8% |

0.47 |

12% |

|

6 |

Canara Bank |

0.48 |

10.57% |

6.5% |

0.48 |

0% |

|

7 |

Central Bank of India |

1.19 |

4.18% |

5.9% |

0.47 |

61% |

|

8 |

Corporation Bank |

0.38 |

5.44% |

34.3% |

0.62 |

-63% |

|

9 |

Dena Bank |

0.34 |

0.00% |

5.7% |

0.46 |

-35% |

|

10 |

IDBI Bank Limited |

0.75 |

4.14% |

6.5% |

0.47 |

37% |

|

11 |

Indian Bank |

0.52 |

8.22% |

7.0% |

0.48 |

8% |

|

12 |

Indian Overseas Bank |

0.36 |

0.00% |

5.4% |

0.46 |

-27% |

|

13 |

Oriental Bank of Commerce |

0.27 |

1.16% |

7.5% |

0.47 |

-75% |

|

14 |

Punjab & Sind Bank |

0.33 |

5.62% |

5.6% |

0.47 |

-42% |

|

15 |

Punjab National Bank |

0.5 |

7.98% |

34.1% |

0.62 |

-25% |

|

16 |

State Bank of India |

0.94 |

10.53% |

80.1% |

0.87 |

7% |

|

17 |

Syndicate Bank |

0.43 |

0.00% |

6.8% |

0.47 |

-8% |

|

18 |

UCO Bank |

0.42 |

0.00% |

6.0% |

0.46 |

-10% |

|

19 |

Union Bank of India |

0.43 |

9.52% |

7.7% |

0.49 |

-13% |

|

20 |

United Bank of India |

0.45 |

4.89% |

6.6% |

0.47 |

-5% |

|

21 |

Vijaya Bank |

0.6 |

5.84% |

4.5% |

0.46 |

23% |

Conclusion from the above table -

So as per Table No-4 the most undervalued PSB bank seems to be Oriental Bank of Commerce as it is undervalued by 75% and hence one can take a long position on it while Central Bank of India is most overvalued bank as it is overvalued by 61% which makes it suitable “short” candidate.

Table No – 5 Predicted P/BV of Private Sector Banks

|

Sr.No |

Bank Name |

PBV |

ROE |

SD |

Predicted P/BV |

- Undervaluation /Overvaluation % |

|

1 |

City Union Bank Ltd. |

2.43 |

14.65% |

3.6% |

2.86 |

-18% |

|

2 |

Dhanlaxmi Bank Ltd |

0.81 |

0.00% |

6.7% |

0.99 |

-22% |

|

3 |

The Federal Bank Ltd. |

1.27 |

17.73% |

10.4% |

3.09 |

-143% |

|

4 |

The Karnataka Bank Ltd. |

0.77 |

13.32% |

5.6% |

2.65 |

-245% |

|

5 |

The Karur Vysya Bank Ltd. |

1.24 |

10.93% |

3.7% |

2.40 |

-94% |

|

6 |

The Lakshmi Vilas Bank Ltd. |

1.04 |

11.32% |

4.3% |

2.44 |

-134% |

|

7 |

RBL Bank |

2.01 |

13.23% |

7.2% |

2.61 |

-30% |

|

8 |

The South Indian Bank Ltd. |

0.72 |

8.97% |

3.9% |

2.16 |

-200% |

|

9 |

Axis Bank Ltd. |

2.76 |

16.56% |

32.1% |

2.45 |

11% |

|

10 |

HDFC Bank Ltd. |

4 |

16.92% |

2.6% |

3.16 |

21% |

|

11 |

ICICI Bank Ltd. |

1.65 |

14.45% |

34.0% |

2.15 |

-30% |

|

12 |

Indusind Bank Ltd. |

6.31 |

13.20% |

4.2% |

2.67 |

58% |

|

13 |

Kotak Mahindra Bank Ltd. |

6.19 |

10.36% |

9.5% |

2.20 |

64% |

|

14 |

YES Bank |

3.88 |

18.38% |

6.3% |

3.26 |

16% |

Conclusion from the above table -

So as per Table No-5 the most undervalued Private Sector bank seems to The Karnataka Bank Ltd. as it is undervalued by 245% and hence one can take a long position on it while Kotak Mahindra Bank Ltd. is most overvalued Private Sector bank as it is overvalued by 64% which makes it suitable “short” candidate.

Other Notable points of the study –

- Compared to PSB’s , Private sector banks are priced at higher P/BV ratios

- Compared to PSB’s , Private sector banks have a higher ROE

- Compared to PSB’s , Private sector banks have lower SD

This makes private sector banks a better investing option as compared to PSB’s as it fits what W.Buffet says “It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

A word of caution here is that an investor has to continuously test and change his mathematical model in order to be relevant and make money .In times of extra ordinary market situation one needs to use more of wisdom and less of mathematics.

CAclubindia

CAclubindia