Introduction:-

The Hon’ble Finance Minister P Chidambaram presented the Union Budget for the financial year 2013 – 2014 in the Assembly of Parliament on 28th February 2013. The main highlights of the Union Budget 2013 are presented here for ready reference of readers.

Direct Tax Changes:

|

In any area within the distance not more than |

Population is more than |

| 2 KMS | 10K but not exceeding 1 Lakh |

| 6 KMS | 1 Lakh but not exceeding 10 Lakh |

| 8 KMS | 10 Lakh |

|

Relaxed (Good initiative for physically Challenged) |

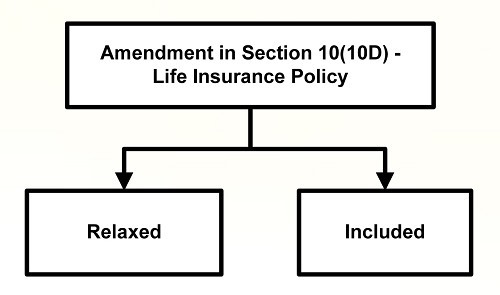

Included (long awaited provision) |

|

10% of sum assured to 15% of sum assured (for person with disability / suffering from disease) |

Insurance policy which has been assigned to a person, at any time during the term of the policy |

New:

|

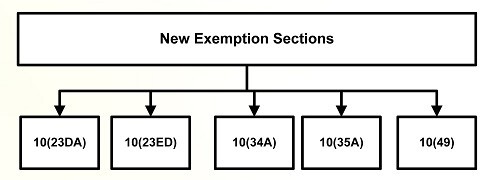

Section |

What type of Income? |

|

10(23DA) |

Income of a Securitization Trust |

| 10(23ED) | Contributions received from a depository of such Investor Protection Fund |

| 10(34A) | Income arising on account of Buy-back of shares as referred in 115QA |

| 10(35A) | Distributed income received from a Securitization Trust |

| 10(49) | Income of NFHCL – National Financial Holdings Company Limited |

Section 32AC - Investment in New Plant & Machinery

Investment Allowance: “I am Back – this time only for 2 years”

Conditions:

• Applicable only to a company

• Cost of New Assets > Rs: 100 crore

• New Assets does not include used machinery, office equipments/appliances, vehicle and 100% depreciated assets in previous years

• Deduction for Two years

• Deduction = 15% of Actual Cost of assets installed between (1.4.2013 to 31.3.2015)

• Available even if the company is amalgamated or demerged within 5 years

• If sold/transferred (other than amalgamation or demerger) within 5 years allowance will be withdrawn and taxed.

Change in Section 56(2)(vii): Gift of Immoveable Property

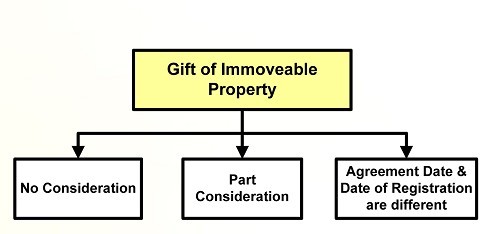

• Without consideration: the stamp duty value of which exceeds Rs: 50,000, the stamp duty value of such property;

• For consideration > Rs: 50,000 but < stamp duty value: the stamp duty value of such property as exceeds such consideration:

• The date of the agreement and the date of registration are not the same,: the stamp duty value on the date of the agreement may be taken

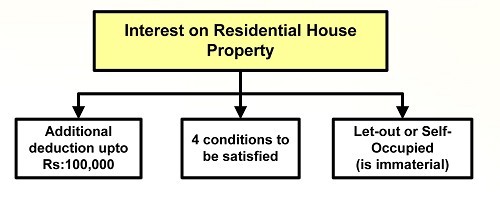

Section 80EE: Deduction is respect of Interest on loan taken for residential House Property:

Conditions to be Satisfied: “This

1. Loan amount <= 25 Lakhs

2. Residential House Value <= 40 Lakhs

3. Loan is disbursed between 1/4/2013 to 31/3/2014

4. Assessee does not own any other residential house property on the date of Loan Sanction

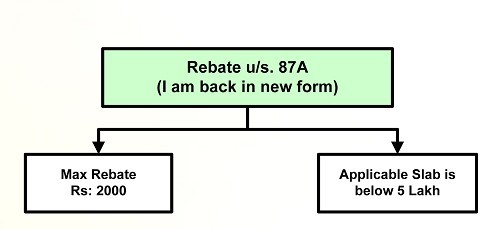

Conditions:

1. The assessees income does not exceed `5 Lakh

2. Maximum Tax Rebate is `2000 [i.e. Persons whose income is above `220,000 to `500,000 will get a flat rebate of `2000 only]

Necessary but not sufficient condition:

• Section 90 & 90A: Bi-lateral and Unilateral Double Taxation Relief: Condition prescribed henceforth

• The certificate of being a resident in a country outside India or specified territory outside India, as the case may be, shall be necessary but not a sufficient condition for claiming any relief under the double taxation avoidance agreement.

TDS on Transfer of Immovable Properties

New Section 194-IA: Payment on transfer of certain immovable property other than agricultural land

• Transferee is responsible to deduct tax at source @ 1% on Sale Consideration

• Not applicable if the consideration is < Rs: 50 Lakh

• Not applicable for Agricultural Land

• Tax Administration Reforms Commission to be set up.

• However, relief for Tax Payers in the first bracket of `2 lakhs to `5 lakhs. A tax credit of `2000 to every person with total income upto `5 lakhs.

• Surcharge of 10percent on persons (other than companies) whose taxable income exceed `1 crore to augment revenues.

• Increase surcharge from 5 to 10 percent on domestic companies whose taxable income exceed `10 crore.

• In case of foreign companies who pay a higher rate of corporate tax, surcharge to increase from 2 to 5 percent, if the taxabale income exceeds `10 crore.

• In all other cases such as dividend distribution tax or tax on distributed income, current surcharge increased from 5 to 10 percent.

• Additional surcharges to be in force for only one year.

• Donations made to National Children Fund eligible for 100 percent deduction.

• Permissible premium rate increased from 10 percent to 15 percent of the sum assured by relaxing eligibility conditions of life insurance policies for persons suffering from disability and certain ailments.

• Contributions made to schemes of Central and State Governments similar to Central Government Health Scheme, eligible for section 80D of the Income tax Act.

• Investment allowance at the rate of 15 percent to manufacturing companies that invest more than `100 crore in plant and machinery during the period 1.4.2013 to 31.3.2015.

• Fifth large tax payer unit (LTU) to open at Kolkata shortly.

Continue:

• No case to revise either the slabs or the rates of Personal Income Tax. Even a moderate increase in the threshold exemption will put hundreds of thousands of Tax Payers outside Tax Net.

• Education cess to continue at 3 percent.

Extended / Liberalized:

• ‘Eligible date’ for projects in the power sector to avail benefit under Section 80-IA extended from 31.3.2013 to 31.3.2014.

• Concessional rate of tax of 15 percent on dividend received by an Indian company from its foreign subsidiary proposed to continue for one more year.

Exemption:

• Securitisation Trust to be exempted from Income Tax. Tax to be levied at specified rates only at the time of distribution of income for companies, individual or HUF etc. No further tax on incom received by investors from the Trust.

• Investor Protection Fund of depositories exempt from Income-tax in some cases.

• Parity in taxation between IDF-Mutual Fund and IDF-NBFC.

• A Category I AIF set up as Venture capital fund allowed pass through status under Income-tax Act.

• TDS at the rate of 1 percent on the value of the transfer of immovable properties where consideration exceeds `50 lakhs. Agricultural land to be exempted.

• A final withholding tax at the rate of 20 percent on profits distributed by unlisted companies to shareholders through buyback of shares.

• Proposal to increase the rate of tax on payments by way of royalty and fees for technical services to non-residents from 10 percent to 25 percent.

• Tax holiday for power plant extended to march 2014

• Reductions made in rates of Securities Transaction Tax in respect of certain transaction.

• Proposal to introduce Commodity Transaction Tax (CTT) in a limited way. Agricultural commodities will be exempted.

Deferred:

• Modified provisions of GAAR will come into effect from 1.4.2016.

• Rules on Safe Harbour will be issued after examing the reports of the Rangachary Committee appointed to look into tax matters relating to Development Centres & IT Sector and Safe Harbour rules for a number of sectors.

• A number of administrative measures such as extension of refund banker system to refund more than `50,000, technology based processing, extension of e-payment through more banks and expansion in the scope of annual information returns by Income-tax Department.

DIRECT TAX – IN NUTSHELL

• No change in basic tax rates

• No changes in personal Income Tax slabs

• Tax credit of Rs 2000 on incomes between `2 - 5 lakh

• Surcharge on super rich, Surcharge of 10% for income of `1 crore or more per annum for one year. This will apply to individuals, HUFs, firms and entities with similar tax status.

• Surcharge charge increased from 5% to 10 percent on domestic companies whose taxable income exceeds `10 crore per year. In the case of foreign companies, who pay the higher rate of corporate tax, the surcharge will increase from 2 percent to 5 percent.

• Additional Surcharge on tax only for 1 year

• Educational Cess to continue at 3 %

• Deduction under Section 80IA extend for 1 year

• Donations to National Children's Fund will be eligible for 100% tax deduction

• Long-term infra bonds also eligible for tax deduction, additional Rs

• 1 lakh deduction for home loans

• 1% TDS for property sale worth more than Rs 50 lakh, exempt on agri land

• TDS on value of immovable property as transaction on immovable properties are usually undervalued

• Extends tax cuts benefits to Rupee Infrastructure Funds

• Securitization Trust income to be exempt

• Tax on Royalty for services provided abroad increased

• 15% Tax on dividend from overseas subsidiaries extended for one

INDIRECT TAX

CUSTOM DUTY

• Leather and leather goods duty reduced from 7.5% to 5%

• Duty on pre-forms of precious and semi-precious stones reduced from 10 percent to 2 percent

• Duty on de-oiled rice bran oil cake has been withdrawn

•Customs duty of 10 percent imposed on export of unprocessed ilmenite and 5 percent on export of upgraded ilmenite

• Customs duty on set top box increased from 5% to 10%

• Customs duty on raw silk increased from 5% to 15%

• Steam coal is exempt from customs duty but attracts a concessional CVD of one percent. Bituminous coal attracts a duty of 5 percent and CVD of 6 percent. To equalize the duty on both kinds of coal , imposed 2 % customs duty and 2 % CVD.

• Luxury cars import duty increased from 75% to 100%

• Yachts duty increased from 10% to 25%

• Luxury motorcycle duty increased from 60% to 75%

• Baggage rules to permit bringing jewellery duty free limit raised to

• `50000 for males and `1 lakh for females

EXCISE DUTY

• Imposed Zero percent Excise duty on Cotton at the fibre stage

• Imposed 12% Excise duty on Spun yarn at the fibre stage

• Handmade carpets and textile floor coverings of coir or jute exempt from excise duty

• In ship building industry, excise duty exempt on ships and vessels

• Increase in excise duty on cigarettes by 18%

• Tax on SUVs increased from 27% to 30%; taxis exempt

• Excise duty on marbles increased from `30 per sq. mtr to `60 per sq mtr

• Excise duty of 4 % imposed on silver manufactured from smelting zinc or lead

• Excise duty of 70 % imposed on imported mobile phones

• Excise duty of 60 % imposed on domestically manufactured mobile phones priced at `2000 or below

• Excise duty increased to 6% on mobile phones priced at more than `2000

• MRP based assessment to be provided in respect of branded medicaments of Ayurveda, Unani, Siddha, Homeopathy and bio-chemic systems of medicine. There will be an abatement of 35 percent.

SERVICE TAX

• Vocational courses and testing activities in relation to agriculture and agricultural produce have been included in the negative list of service tax,.

• Till now, full exemption of service tax was granted on copyright on cinematography. Now the exemption of service tax is limited to films exhibited in cinema halls

• Till now, service tax does not apply to air conditioned restaurants that do not serve liquor. From now, service tax on all air conditioned restaurants irrespective of any distinction.

• The rate of abatement reduced to 70% from 75% for the Homes and flats with a carpet area of 2,000 sq.ft or more or of a value of `1 crore or more

• Existing exemptions from service tax for low cost housing and single residential units will continue.

DISCLAIMER

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation

Post your reflections to:

S.Dhanapal, B.Com, B.A,B.L, F.C.S

Managing partner

S DHANAPAL & ASSOCIATES

Practising Company Secretaries

3rd Floor, Victory Towers,

Old No.724/725, New No.486,

Poonamallee High Road,

(Opp to Pachaippa's College),

Aminjikarai, Chennai- 600 029.

Email Id. csdhanapal@gmail.com

CAclubindia

CAclubindia