The new legislation is focused on transparency and disclosure and gives audit its due recognition. In the new Act, attempt has been made to cover each aspect of corporate functioning under audit by prescribing various types of audits like internal audit and secretarial audit. This not only augurs well for the stakeholders but also throws open opportunities for professionals to utilize their skills in pursuit of their profession.

The current write up throws light on the various types of audits prescribed under the Companies Act, 2013.

Statutory Audit

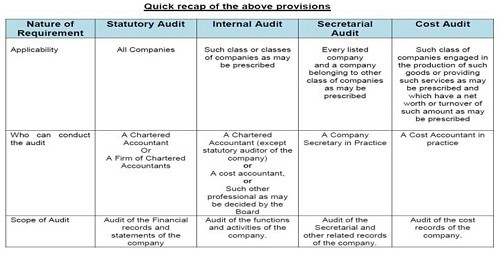

Sections 139 to 147 under chapter X of the Act contain provisions regarding audit and auditors. Section 139 contains that at the first annual general meeting every company shall appoint an inpidual or firm as it auditor who will hold office from the conclusion of that meeting till the conclusion of the sixth annual general meeting. Section 141 contains that a person shall be eligible for appointment as an auditor of a company only if he is a chartered accountant and in case of a firm whereof majority of partners practising in India are qualified for appointment as aforesaid may be appointed by its firm name to be auditor of a company. Section 143 which contains provisions regarding powers and duties of auditors contains that the statutory auditor shall make a report to the members of the company on the accounts and financial statements examined by him. The main provisions regarding statutory audit are:

· Auditor will have access to books of accounts and vouchers etc. at all times and he can seek information from officers of the company as he may deem necessary.

· In his report he must state, besides other things, whether the financial statements represent a true and fair view of the state of company's affairs as at the end of the financial year.

· In case of any qualifications in the audit report, the reason for same must be stated in the report.

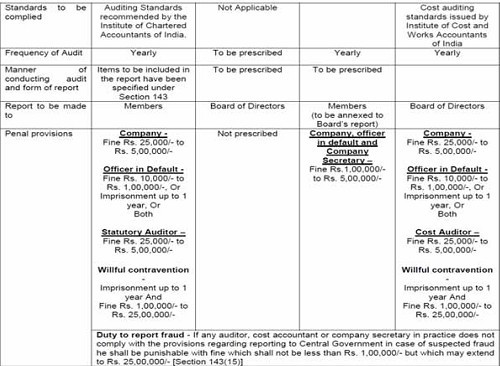

· Auditor is required to comply with Auditing Standards.

· In case auditor suspects any fraud, he must immediately report the same to the Central Government.

Internal Audit

Section 138 of the Bill contains provisions regarding internal audit. The provisions prescribed in the bill are very brief in nature which will be substantiated by the rules to be prescribed. The provisions contained in the bill are as follows:

· Certain class or classes of company as may be prescribed shall appoint an internal auditor who will conduct an audit of the functions and activities of the company and make a report thereon to the Board of Directors.

· Any chartered Accountant (except statutory auditor of the company) or Cost Account or other professional as may be decided by the Board, can be appointed to conduct the internal audit.

· Manner and frequency of conducting the audit will be prescribed.

Secretarial Audit

Secretarial Audit is a new requirement which has been prescribed under Section 204 of the Bill. The provisions regarding secretarial audit are as follows:

· Every listed company and other class of companies as may be prescribed is required to annex to the Board's Report, a Secretarial Audit Report.

· Secretarial Audit has to be conducted by a Practising Company Secretary in respect of the secretarial and other records of the company

· Company is required to give all necessary information and assistance to the Practising Company Secretary to conduct the audit.

· The Board is required to provide explanation in the Board's Report to every qualification, observation or other adverse remark made by the company secretary in his report.

· Form of report will be prescribed.

· As per Section 143(14), all provisions regarding rights, duties and obligations of statutory auditors shall also apply to Company Secretary in Practice conducting secretarial audit.

Cost Audit

Section 148 of the Bill contains provisions regarding cost audit and contains that a cost audit wherever conducted is in addition to statutory audit conducted under section 143.

The main provisions regarding cost audit as contained in the Bill are:

· Certain class of companies engaged in the production of such goods or providing such services as may be prescribed and which have a net worth or turnover of such amount as may be prescribed may be directed to get their cost audit records audited.

· Cost audit has to be conducted by a Cost Accountant in Practice who is required to comply with cost auditing standards

· It shall be the duty of the company to give all assistance and facilities to the cost auditor.

· As per Section 143(14), the qualifications, disqualifications, rights, duties and obligations applicable to statutory auditors will also apply to a cost auditor.

· Cost auditor has to submit his report to the Board of Directors who in turn shall file it with the Central Government within 30 days of the receipt of the report.

CAclubindia

CAclubindia