1. Definition and Scope of Rent-A-Cab Service

1.1 What is Rent- A-Cab Service?

Rent-A-Cab Service means renting of any motor vehicle designed to carry passengers!!!

1.2 What? I haven’t heard or read such a definition anywhere?

Correct, but let me explain - As per Finance Act, 1994 the relevant definitions contained in Section 65 are as follows:

Section 65(105)(o) – ‘taxable service’ means any service provided or to be provided “to any person, by a ‘rent-a-cab scheme operator’ in relation to the renting of a cab.”

Section 65(91) - “rent-a-cab scheme operator means any person engaged in the business of renting of cabs.”

Section 65(20) - “Cab means –

(i) a motorcab, or

(ii) a maxicab, or

(iii) any motor vehicle constructed or adapted to carry more than twelve passengers, excluding the driver, for hire or reward:

Provided that the maxicab referred to in sub-clause (ii) or motor vehicle referred to in sub-clause (iii) which is rented for use by an educational body imparting skill or knowledge or lessons on any subject or field, other than a commercial training or coaching centre, shall not be included within the meaning of cab.”

Section 65(71) read with Section 2(25) of Motor Vehicle Act, 1988, “motor cab means any motor vehicle constructed or adapted to carry not more than six passengers excluding the driver for hire or reward.”

Section 65(70) read with Section 2(22) of Motor Vehicle Act, 1988, “maxi cab means any motor vehicle constructed or adapted to carry more than six passengers but not more than twelve passengers excluding the driver for hire or reward.”

Section 65(73) read with Section 2(28) of Motor Vehicle Act, 1988, “motor vehicle or vehicle means any mechanically propelled vehicle adapted for use upon roads whether the power of propulsion is transmitted thereto from an external or internal source and includes a chassis to which a body has not been attached and a trailer; but does not include a vehicle running upon fixed rails or a vehicle of a special type adapted for use only in a factory or in any other enclosed premises or a vehicle having less than four wheels fitted with engine capacity of not exceeding thirty-five cubic centimetres.”

However, as per Notification No. 20/2012-ST dated 05-06-2012, the provisions of Section 65 shall not apply with effect from 01-07-2012. It means, in the Negative List regime, the definitions contained in Section 65 are no longer applicable for service provided or agreed to be provided on or after 01-07-2012. The new definitions are contained in section 65B of the Finance Act, 1994 which do not define ‘Rent-A-Cab’ or any similar service.

1.3 How rent-a-cab service has been defined at Answer to Q. 1.1 above?

For the purposes of abatement and reverse charge mechanism, the service of ‘renting of motor vehicle designed to carry passengers’ has been specifically provided. And as per rules of interpretations under section 66F(2), where a service is capable of differential treatment for any purpose based on its description, the most specific description shall be preferred over a more general description. So, the definition given at answer to Q.1 is not the statutory definition, but adopted for the sake of convenience to name such specific description. Also for payment of tax, the accounting code ‘00440048’ of rent a cab operator service is the most appropriate code for such service.

1.4 Who are covered under rent-a-cab service?

Any person providing service of ‘renting’ of motor vehicle designed to carry ‘passengers’, which is not covered under the negative list u/s 66D and also not exempted vide Notification No. 25/2012-ST dated 20-06-2012 is covered in the description of rent-a-cab service. It can be clearly seen that renting of any motor vehicle (and not just a cab/taxi) is included. It means it includes renting of motor cars, motor cabs, maxi cabs, mini buses, buses and all other motor vehicles which are designed to carry passengers, irrespective of its passenger carrying capacity. The more meaningful description of this service could be ‘Rent-A-Passenger Vehicle Service’ which is not provided in the listed services. Also note that the vehicles like truck, trailer, dumper, etc designed to carry goods are not covered by this description.

It is pertinent to mention that as per declared service u/s 66E(f), the levy of service tax is attracted on transfer of goods by way of hiring, leasing, licensing or in any such manner without transfer of right to use such goods. This is because any transfer of right to use goods is considered as ‘deemed sale’ as per Article 366(29A) of the Constitution of India and the Central Government is not empowered to levy service tax on such transactions. However, almost all the state governments have levied VAT on such deemed sale. It means that any such activity of renting, hire, lease, licence, etc would attract service tax or VAT, which are mutually exclusive, depending on transfer of right to use as per facts and circumstances of each transaction and based on judicial precedents.

The Hon’ble Supreme Court in the case of Rashtriya Ispat Nigam Ltd. held that ‘transfer of right to use goods’ involves transfer of possession and effective control over such goods, but mere transfer of custody along with permission to use or enjoy such goods, per se, does not lead to transfer of possession and effective control. This being a completely different and vast subject in itself, the author does not wish to elaborate more of it here.

1.5 What is the meaning of ‘renting’?

As per Section 65B(41), “renting means allowing, permitting or granting access, entry, occupation, use or any such facility, wholly or partly, in an immovable property, with or without the transfer of possession or control of the said immovable property and includes letting, leasing, licensing or other similar arrangements in respect of immovable property.”

The term renting has been defined above in the context of renting of immovable property and the same definition can’t be imported to interpret ‘renting of motor vehicle’. Hence, renting has to be given its general and common usage meaning in the context of motor vehicles. The meaning of ‘rent’ as per Oxford Dictionary is: (i) “Pay someone for the use of (something, typically property, land, or a car).” (ii) “A sum paid for the hire of equipment.”

1.6 Whether ownership of the vehicle is a pre-requisite?

No. Even the erstwhile statutory definition of ‘rent-a-cab scheme operator’ uses the words ‘renting of cabs’ and does not stipulate that the cab must be owned by the operator.

a) In case of Transport Solutions Group Vs. CCE (2006), the Tribunal, Mumbai held that there is no requirement for a rent-a-cab scheme operator to own the vehicles which are rented out.

b) In case of Ghanshyam Transport Vs. CCE (2009), it was held that if a person is engaged in business of engaging taxis for customers and giving them services without even owning or plying vehicle, service tax is payable under ‘Rent-a-cab scheme operators’ service.

In the negative list regime, any service other than in negative list or exempted is a taxable service. An operator can take a vehicle on rent and then rent it out to a third party; he will be treated as a rent-a-cab operator. Similarly, the owner of the vehicle in such situation will also be treated as rent-a-cab operator when he renders service of renting of motor vehicles.

1.7 Whether service tax is attracted when the customer hires the vehicle on per KM rate basis, agreeing to some minimum fare and where the driver as well as the fuel is provided by the service provider?

Prior to 01-07-2012, i.e. in the positive list approach of taxation, various courts held that such services are in the nature of ‘transportation service’ provided to the customer wherein neither the possession, not the control has been given to the customer and service tax not attracted.

a) In the case of Kuldip Singh Gill Vs. CCE [2006(3) STR 689], [STO-2005-CESTAT-324] has observed that the vehicle running on Kilometre basis are not liable to service tax.

b) In the case of RS Travels Vs. CCE [2008 (12) STR 27] [(2008) 15 STT 437 (New Delhi – CESTAT)], where the Tribunal observed that the cab operator providing cab with driver for going from one place to another either on Kilometre basis or lump sum basis based on the distance is that of a transportation service and observed that no service tax is payable as the control over the vehicle is with the rent-a-cab operator. Similar view was taken in the case of Surya Tours & Travels Vs. CCE [2008 (10) TMI 123 – CESTAT, NEW DELHI].

c) Further, in the case of Cochin International Airport Prepaid Taxi Operators Co-op society [2008 (16) STT 190], the Tribunal held that a co-operative society formed by taxi drivers playing to and for airport cannot be considered as operating tours in a tourist vehicle for purpose of levy of service tax.

However, all these judgement are with respect to ‘rent a cab scheme operator’ service which had a statutory definition u/s 65(91) and is no more applicable in the negative list regime. In author’s view, all such services which were earlier termed as ‘transportation service’ are now liable to service tax as rent-a-cab service.

2. NEGATIVE LIST

2.1 What types of Rent-A-Cab services are not taxable?

The service of transportation of passengers with or without accompanied belongings by a stage carriage; and metered cabs, radio taxis or auto rickshaws are covered in the negative list, hence not taxable.

As per Section 65B(40) “stage carriage means a motor vehicle constructed or adapted to carry more than six passengers excluding the driver for hire or reward at separate fares paid by or for individual passengers, either for the whole journey or for stages of the journey”

As per Section 65B(32) “metered cab means any contract carriage on which an automatic device, of the type and make approved under the relevant rules by the State Transport Authority, is fitted which indicates reading of the fare chargeable at any moment and that is charged accordingly under the conditions of its permit issued under the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under”

The term ‘radio taxi’ has neither been defined in the Finance Act, 1994 nor in the Central Excise Act, 1944 or in any rules framed there under. However, the intention could be to exempt radio taxis operated by operators who obtained licence under any scheme, in this behalf, framed by the state government u/s 74 and other provisions of the Motor Vehicle Act, 1988. In general, but not necessarily, the main features of radio taxis are:

a. The vehicle should be fitted with electronic fare meters on the front panel.

b. The vehicle should be fitted with GPS/GPRS based tracking devices which must be in constant communication with the Central Control unit while the vehicle is on duty.

c. The vehicle should be equipped with a mobile radio fitted in the front panel for communication between driver and the main control room of the licensee.

d. On the roof of the vehicle there should be an LCD board to display that the vehicle is a radio taxi.

e. The scheme may provide for minimum fleet size, say 100 cabs for making application for licence under the scheme.

f. The scheme may also prescribe the manner in which the fare is to be charged.

3. EXEMPTION

3.1 Whether ambulance service provided by hospitals is exempted?

Yes, as per entry no. 2 of mega exemption Notification No. 25/2012-ST dated 20-06-2012, health care services, which include services by way of transportation of patient to and from a clinical establishment is exempted. Also, as per clarification given by CBEC vide Letter F. No. 334/1/2007- TRU dated 28-02-2007, ambulances are not meant for carrying passengers for hire or reward. Hence, service tax liability does not arise on renting of ambulances.

3.2 Whether services provided to an educational institution including schools, colleges and universities by way of transportation of students, faculty or staff is exempted?

Yes, as per entry no. 9 of mega exemption Notification No. 25/2012-ST dated 20-06-2012, auxiliary educational services, which include services relating to transportation of students, faculty or staff of such institution is exempted.

3.3 Whether services provided by an educational institution including schools, colleges and universities by way of transportation of students, faculty or staff is exempted?

The exemption was given under the above entry no. 9 which has been withdrawn w.e.f. 01-04-2013. However, as per entry no. 23 of mega exemption Notification No. 25/2012-ST dated 20-06-2012, service of transport of passengers, with or without belongings, by a contract carriage for the transportation of passengers, excluding tourism, conducted tour, charter or hire is also exempted.

As per section 2(7) of the Motor Vehicles Act, a “contract carriage means a motor vehicle which carries a passenger or passengers for hire or reward and is engaged under a contract, whether express or implied, for the use of such vehicle as a whole for the carriage of passengers mentioned therein and entered into by a person with a holder of a permit in relation to such vehicle or any person authorized by him in this behalf on a fixed or an agreed rate or sum–

a) On a time basis, whether or not with reference to any route or distance; or

b) From one point to another;

And, in either case, without stopping to pick up or set down passengers not included in the contract anywhere during the journey, and includes

a) A maxi cab; and

b) A motor vehicle notwithstanding that separate fares are charged for its passengers.”

The essential ingredient of a contract carriage is that it plies under a contract for a fixed set of passengers, and does not allow any other passenger to board or alight from the carriage at will. The transportation service provided by educational institutions is in the nature of contract carriage and hence exempted. Moreover, this exemption is not restricted to educational institutions but can be availed by any ‘contract carriage’.

3.4 Whether any other exemption is also available?

As per entry no. 22 of mega exemption Notification No. 25/2012-ST dated 20-06-2012, services by way of giving on hire - (a) to a state transport undertaking (as defined in section 2(42) of Motor Vehicle Act, 1988), a motor vehicle meant to carry more than twelve passengers; (b) to a goods transport agency, a means of transportation of goods; is exempted.

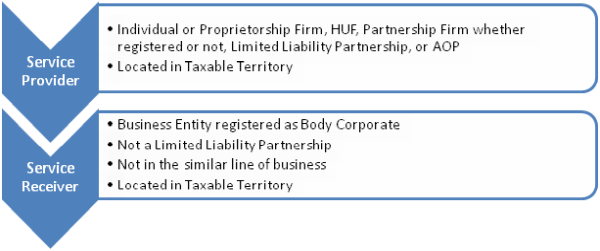

4. REVERSE CHARGE MECHANISM

4.1 When is Reverse Charge Mechanism – RCM applicable for Rent-A-Cab Service?

As per Section 68(2) of the Finance Act, 1994, the Central Government is empowered to notify such services on which the liability of pay service tax shall be on the service receiver to the extent specified, instead of service provider. The Central Government has issued Notification No. 30/2012-ST dated 20-06-2012 and RCM is also applicable on Rent-A-Cab service if all the following conditions are fulfilled:

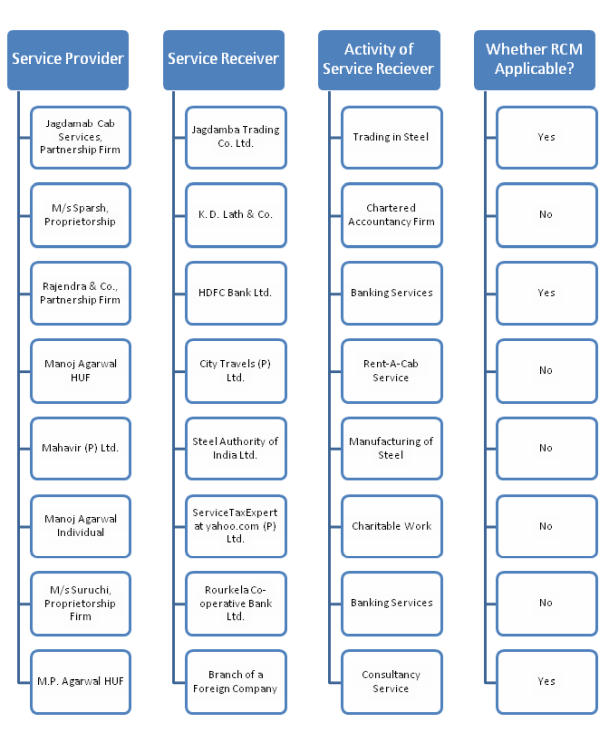

5. Illustrations under various situations to show whether reverse charge mechanism is applicable or not, assuming that both the service provider and service receiver are located in the taxable territory.

6. ABATEMENT

6.1 When is abatement available for Rent-A-Cab Service?

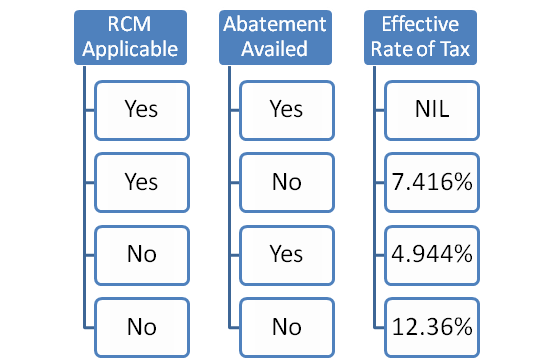

As per Sr. No. 9 of Notification No. 26/2012-ST dated 20-06-2012, abatement of 60% is available on Rent-A-Cab Service i.e. service of renting of any motor vehicle designed to carry passengers. It means service tax is payable on only 40% of the value of Rent-A-Cab service. The abatement is subject to the condition that the Cenvat Credit of inputs, capital goods and input services, used for providing the taxable service, has not been taken under the provisions of Cenvat Credit Rules, 2004. If the service provider avail cenvat credit on any input, capital good or input service, used for providing rent a cab service, then abatement is not available.

7. CENVAT CREDIT

7.1 Whether Cenvat Credit is available on Rent-A-Cab Service?

The Hon’ble Karnataka High Court in the case of CCE Vs. Stanzen Toyotetsu India (P) Ltd. [(2011) 32 STT 244 (Kar.)] held that the transportation/Rent-a-Cab service is provided by the assessee to their employees in order to reach their factory premises in time which has a direct bearing on manufacturing activity. In fact, the employee is also entitled to conveyance allowance which would form part of his condition of service. Therefore, by no stretch of imagination it can be construed as a welfare measure by denying the availment of Cenvat credit to the assessee for providing transportation facilities as a basic necessity which has a direct bearing on the manufacturing activity. This decision was again followed by the same court in the case of CCE Vs. Tata Auto Comp Systems Ltd. CEA No. 132 of 2009.

But, w.e.f. 01-04-2011, the Central Government has amended the definition of ‘input service’ under Rule 2(l) of Cenvat Credit Rules, 2004 vide Notification No. 3/2011 – CE(NT) dated 01-03-2011 and again vide Notification No. 18/2012 – CE(NT) dated 17-03-2012 (w.e.f. 01-04-2012). The effect of the amendment is that rent-a-cab service has been specifically excluded from the definition of ‘input service’ and hence cenvat credit is generally not available. Cenvat Credit is available only when rent a cab service could be related to a motor vehicle which is capital good for them. In other words, when a motor vehicle designed to carry passengers including their chassis, registered in the name of provider of service, when used for provided output service of- (i) transportation of passengers; or (ii) renting of such motor vehicle; or (iii) imparting motor driving skills, then cenvat credit can be availed.

8. EFFECTIVE RATE OF SERVICE TAX

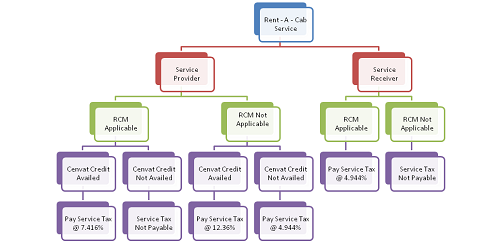

8.1 What is the effective rate at which service tax is payable by Service Provider?

8.2 What is the effective rate at which service tax is payable by Service Receiver?

The service receiver shall pay service tax @ 4.944% (i.e. 12.36% of 40% Value) only when reverse charge is applicable. His liability to pay service tax is not affected by cenvat credit availed or not availed by the service provider. When RCM is not applicable, service receiver is not required to pay any tax.

9. Below is the Flow Chart of effective rate of service tax payable by service provider and service recipient under various situations:

POINTS TO NOTE:

1. When the service provider has not availed any cenvat credit, i.e. when abatement is available, then the service tax is payable @ 4.944% either by provider or receiver depending of applicability of RCM.

2. When the service provider has availed any cenvat credit, i.e. when abatement is not available, then the total service tax is payable @ 12.36% by provider or jointly with receiver depending of applicability of RCM.

3. As far as service receiver is concerned, he shall pay @ 4.944% only, irrespective of abatement, only when RCM is applicable.

Author: Manoj Agarwal,

Address: Ganpati Campus, Lal Building Road, Rourkela – 769012

E:mail: ServiceTaxExpert@yahoo.com Kindly send mail for further clarifications.

CAclubindia

CAclubindia