Dear Professional Colleague,

The Union Budget, 2014 presented by the Finance Minister today is promising on building consumer’s confidence, investor’s confidence & overall confidence and taken several steps to improve fiscal situation and boost growth of Indian economy to 7-8% in coming years. The Roadmap made for fiscal consolidation in the next 3 years is inspiring on reduced fiscal deficit at 4.1% of GDP in 2014-15, 3.6% in 2015-16 and 3% in 2016-17.

Further, the focus on rural infrastructure, agriculture infrastructure, urban infrastructure, manufacturing revival, tourism, education, banking and finance and foreign direct investments would go a long way to rejuvenate the economic growth, going forward. Focus on GST implementation and discussions with State Governments are also encouraging.

HIGHLIGHTS OF CHANGES IN INDIRECT TAXES:

We are presenting you detailed analyses of changes made in Indirect Taxes viz. Service Tax, Excise and Customs vide the Union Budget, 2014.

UNION BUDGET 2014: CHANGES IN SERVICE TAX:

After the introduction of the Negative List based Service tax regime in July, 2012, the emphasis has been to ensure stability and continuity. The main focus in service tax at the present juncture is to widen the tax base and enhance compliance.

The changes being made by amendments in Notifications and Rules can be categorized into two broad categories based on when they would come into effect:

(i) changes which will have immediate effect; and

(ii) changes which are proposed to be given effect to only from 1st October, so as to coincide with the Service Tax Return cycle.

As far as statutory amendments are concerned, they would come into effect only from the date on which the Bill receives the assent of the President.

A. Changes In Chapter V of the Finance Act, 1994 (Will Come Into Force When the Finance Bill (No.2), 2014 is enacted):-

I. Changes in relation to the Negative list:-

• To broaden the tax base in Service tax, Sale of space or time for advertisements in broadcast media, namely radio or television, extended to cover such sales on other segments like online and mobile advertising, etc. Sale of space for advertisements in print media however would remain excluded from Service tax.

• Service provided by radio-taxis brought under the Service tax. The abatement presently available to rent-a-cab service would also be made available to radio taxi service, to bring them on par.

II. Other Important Changes in the Finance Act, 1994:-

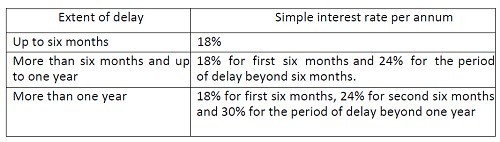

1. Variable Rates of Interest for Delayed Payment of Service Tax Prescribed By Notification No. 12/2014-ST Dated 11-7-2014:-

• To encourage prompt payment of Service tax, new interest rates on delayed payments under Section 75 of the Finance Act, 1994, which would vary as per the extent of delay has been prescribed as under:

This new interest rate regime will become operational from October 1, 2014 up to which the rate of interest of 18%, as presently applicable, will continue to apply.

E.g. Assume a case, where service tax became due, say, on the 6th of July, 2012 and the assessee pays the dues on 6th of December, 2014. In such a case, the interest to be charged would be as below:

(i) 18% simple interest upto September, 30th, 2014.

(ii) For the period from 1st October, 2014 to 6th December, 2014, the rate of interest will be 30% since the period of delay is beyond one year.

As specified in the proviso to section 75, three per cent concession on the applicable rate of interest will continue to be available to the small service providers, whose value of taxable services provided in a financial year does not exceed Sixty lakh rupees during any of the financial years covered by the notice or during the last preceding financial year, as the case may be.

2. Changes in Advance Ruling Under Section 96A(b)(iii) of The Finance Act, 1994 Vide Notification No. 15/2014-ST Dated 11-7-2014 (Effective From July 11, 2014):-

• The Resident Private Limited Company has also been included as a class of persons eligible to make an application for Advance Ruling in Service tax.

3. Other Changes:

• Changes in Section 67A of the Finance Act, 1994:

Section 67A is amended enabling Government to prescribe rules for determination of rate of exchange for calculation of taxable value in respect of certain services. Rules will be prescribed in due course, after the Bill receives the assent.

• Changes in Section 73 of the Finance Act, 1994:

Section 73 is amended providing time limits for completion of adjudication already existing in Central Excise which are to be followed, as far as possible.

• Changes in Section 80 of the Finance Act, 1994:-

Section 80 is amended excluding reference of first proviso to Section 78 wherein power was granted to waive the 50% penalty imposable in cases where Service tax has not been levied, not paid or short levied or short paid on account of suppression of facts or willful misstatement but details of transactions are available in the specified record. The said power has now been removed.

• Changes in Section 82 of the Finance Act, 1994:-

Section 82(1) is amended along with Section 12F(1) of the Central Excise Act 1944, whereby the Joint Commissioner or Additional Commissioner or any other officer notified by the Board can authorize any Central Excise Officer to search and seize.

• Changes in Section 86(6A) of the Finance Act, 1994:-

Section 86(6A) is amended to provide that every application made before the Appellate Tribunal in an appeal for rectification of mistake or for any other purpose or for restoration of an appeal or an application only shall be accompanied by a fee of five hundred rupees. However, earlier the appeal for grant of stay was also to be accompanied by a fee of five hundred rupees.

• Changes in Section 87 of the Finance Act, 1994:-

Section 87 is amended by incorporating power to recover dues of a predecessor from the assets of a successor purchased from the predecessor on the same line as it is provided under Section 11 of the Central Excise Act, 1944.

To read the full article: Click Here

CAclubindia

CAclubindia