Section 118 of the Companies Act, 2013 which contains provisions relating to minutes of Board, General and other meetings and resolutions passed by postal ballot, contains in sub-section 10 that “Every company shall observe secretarial standards with respect to general and Board meetings specified by the Institute of Company Secretaries of India constituted under section 3 of the Company Secretaries Act, 1980, and approved as such by the Central Government.”

By virtue of the above provision, the Institute of Companies Secretaries of India (ICSI) has issued two Secretarial Standards, namely

SS1 - Secretarial Standard on Meetings of the Board of Directors, and

SS2 - Secretarial Standard on General Meetings

This write-up analyses the provisions of Secretarial Standard on General Meetings (SS2). Provisions of the standard relating to detailed procedure of e-voting, postal ballot and poll are not elaborated in this write-up.

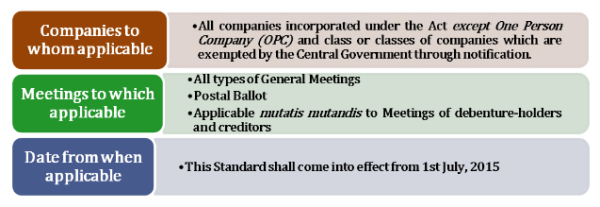

APPLICABILITY

PROVISIONS RELATING TO CONVENING A GENERAL MEETING

Who can call a general meeting?

A General Meeting shall be convened by or on the authority of the Board.

i. Board is required to convene an Annual General Meeting every year.

ii. EGM can be convened by the Board whenever it deems fit.

Meeting called on requisition of Members:

i. If the Board falls to convene an AGM, any Member of the company may approach the prescribed authority, which may then direct the calling of the Annual General Meeting of the company.

ii. In case of EGM, the Board shall on valid requisition made by members holding not less than 1/10th of the paid-up share capital carrying Voting Rights (Company having share capital) or not less than 1/10th of total voting power of the company (Company not having share capital) call an EGM.

To whom notice of a general meeting has to be served?

Notice in writing of every general meeting shall be given to

i. Every Member of the company.

ii. Directors of the company

iii. Auditors of the company,

iv. Secretarial Auditor,

v. Debenture Trustees, if any, and, wherever applicable or so required, to other specified persons.

What are the various permitted modes through which notice can be dispatched?

Notice shall be sent by

i. Hand,

ii. Ordinary post, except for postal ballot and where e-voting is provided

iii. Speed post,

iv. Registered post,

v. Courier,

vi. Facsimile,

viii. E-mail,

ix. Any other permitted electronic means

Contents of the notice

Notice shall specify the

i. day,

ii. date,

iii. time, and

iv. full address of the venue of the Meeting including route map and prominent land mark for easy location.

v. Nature of the meeting

vi. Business to be transacted at the meeting

vii. Resolution for each item of special business supported by explanatory statement

viii. Resolution for items of ordinary business which pertain to appointment of directors and auditors, other than those retiring

ix. Details relating to e-voting

Statement regarding appointment of Proxy

Notice shall prominently contain a statement that a Member entitled to attend and vote is entitled to appoint a Proxy, or where that is allowed, one or more proxies, to attend and vote instead of himself and that a Proxy need not be a Member.

In case of companies having a website, the Notice shall be hosted on the website along with the route map for venue of the meeting.

Contents of explanatory statement

As stated above, each item of special business in the notice of a general meeting has to be accompanied by an explanatory statement.

i. It shall set out all such facts as would enable a Member to understand the meaning, scope and implications of the item of business and to take a decision thereon.

ii. The nature of the concern or interest (financial or otherwise), if any, of the Directors and Manager, Other Key Managerial Personnel, and relatives of any of them, in any item of special business or in a proposed Resolution, shall be disclosed in the explanatory statement.

iii. Where the special business of a company relates to or affects any other company, then the extent of shareholding interest in the other company of every Promoter, Director, Manager, and of every other Key Managerial Personnel of the first mentioned company, being not less than 2%, shall be disclosed in the explanatory statement.

iv. Where reference is made to any document, contract, agreement, the Memorandum or Articles of Association, the explanatory statement shall state that such documents are available for inspection during specified business hours at the Registered Office of the company, at the Head Office as well as Corporate Office of the company, if any, if such office is situated elsewhere, and also at the Meeting.

Contents of explanatory statement contd….

Where any item of business relates to appointment/re-appointment of fixing of remuneration of any Director or Manager, explanatory statement to contain:

i. age,

ii. qualifications,

iii. experience,

iv. terms and conditions of appointment or re-appointment along with details of remuneration sought to be paid and the remuneration last drawn by such person, if applicable,

v. date of first appointment on the Board,

vi. shareholding in the company,

vii. relationship with other Directors, Manager and other Key Managerial Personnel of the company,

viii. the number of Meetings of the Board attended during the year

ix. other Directorships, Membership/ Chairmanship of Committees of other Boards.

In case of appointment of Independent Directors, the justification for choosing the appointees and in case of re-appointment, performance evaluation report of such Director or summary thereof shall be included in the explanatory statement.

Notice Period (How many days before the meeting notice need to be sent?

i. Notice and accompanying documents shall be given at least 21 clear days in advance of the Meeting, excluding the day of sending the Notice and the day of Meeting.

ii. For sending notice by post or courier, an additional 2 days shall be provided for the service of Notice.

iii. If any special notice is received from any member, same has to be sent atleast 7 clear days in advance.

iv. Shorter notice can be given provided at least 95% of the Members entitled to vote at the Meeting give their consent in writing.

v. Amendments can be made to the notice provided the notice of amendment is given 21 clears days in advance.

Documents to be accompanied with the notice

i. Explanatory statement for each item of special business

ii. The request for consenting to shorter Notice, if required

iii. Attendance slip and a Proxy form with clear instructions for filling, stamping, signing and/or depositing the Proxy form

Time, Day and Venue of meeting

Time and day for holding meeting

Meetings shall be called during business hours, i.e., between 9 a.m. and 6 p.m. on a day that is not a National Holiday (“National Holiday” includes Republic Day, i.e., 26th January, Independence Day, i.e., 15th August, Gandhi Jayanti, i.e., 2nd October and such other day as may be declared as National Holiday by the Central Government.

Venue of Meeting:

AGM and meeting called by requisitionists - shall be held either at the registered office of the company or at some other place within the city, town or village in which the registered office of the company is situated.

Other General Meetings – may be held at any place within India

Frequency of holding AGM

i. One AGM to be held in every calendar year

ii. AGM to be held within 6 months of closure of the financial year or 15 months of previous AGM, whichever is earlier. This time can be further extended by 3 months with approval of ROC.

iii. First AGM to be held within 9 months of closure of first financial year and accordingly, holding an AGM in first calendar year of incorporation may not be required.

Quorum requirements

|

Public Company having:

|

5 members 15 members 30 members |

|

Private Company |

2 Members |

i. Quorum needs to be present throughout the meeting

ii. Member needs to be personally present and Proxy are not counted for purpose of quorum

iii. If articles provide a higher quorum, such higher requirement needs to be followed.

iv. Duly authorised representative of a body corporate or the representative of the President of India or the Governor of a State is deemed to be a Member personally present.

v. One person can be authorised representative for two or more bodies corporate and he will be counted as separate member for each body corporate he represents. However, for a valid meeting, atleast 2 individuals shall be present in person, both for public and private companies.

vi. Related parties, not entitled to vote on any specific item of business, are counted for purpose of quorum.

vii. Members who have already voted through remote e-voting are counted for purpose of quorum.

viii. For postal ballot, quorum requirements are not applicable.

Presence of Directors and Auditors

i. If any Director is unable to attend the Meeting, the Chairman shall explain such absence at the Meeting.

ii. Chairman of various mandatory committees under the Act, or some member of the committee authorised by the Chairman, is required attend all general meeting.

iii. Statutory Auditors, or their authorised representative, who is also qualified to be an auditor, shall attend all general meetings, unless exempted by the Company.

iv. Secretarial Auditors or their authorised representative, who is also qualified to be an auditor, shall attend Annual General Meeting, unless exempted by the Company. Other general meetings may be attended, if invited by the Chairman.

Chairman of General Meetings

i. Chairman of Board to chair the general meetings, failing which Directors to elect one among themselves as Chairman, failing which also, members to elect one among themselves as Chairman.

ii. Chairman to ensure that Meeting is duly constituted in accordance with the Act and the Articles or any other applicable laws, before it proceeds to transact business and to conduct the Meeting in a fair and impartial manner.

iii. The Chairman shall explain the objective and implications of the Resolutions before they are put to vote at the Meeting.

iv. Chairman not to conduct proceedings for items of business in which he is interested, in case of public companies.

Voting at a meeting

i. Every Resolution shall be proposed by a Member and seconded by another Member.

ii. Method of voting:

E-voting:

a. Mandatory for all equity listed companies and those having more than 1000 shareholders.

b. Facility of voting at the meeting (electronic or ballot paper) to be mandatorily provided in addition to remote e-voting for every item of business. Proxies can also vote.

c. Members who have already voted on remote e-voting can attend the meeting but cannot vote again.

d. Notice of meeting shall clearly state that person who is not a Member as on the cut-off date should treat the Notice for information purposes only.

e. E-voting facility is to be provided even for resolutions proposed to be passed through postal ballot.

Show of Hands:

Where remote e-voting is not applicable, every resolution to be first put to vote by show of hands, unless poll is demanded. Proxies cannot vote of show of hands.

Poll:

Poll can be taken by chairman on his own motion or on demand by any member of proxy.

Modification, recession and withdrawal of resolution

i. Resolutions already put to vote by remote e-voting cannot be modified or withdrawn.

ii. Resolutions for items of business which are likely to affect the market price of the securities of the company cannot be withdrawn.

iii. A Resolution passed at a Meeting shall not be rescinded otherwise than by a Resolution passed at a subsequent Meeting.

iv. Grammatical, clerical, factual and typographical errors alone, if any, may be corrected as deemed fit by the Chairman. Modification which has the effect of, in any way, altering the substance of the Resolution as set out in the Notice cannot be made.

Minutes of general meetings – Method of recording and maintenance

i. The Company Secretary shall record the proceedings of the Meetings. Where there is no Company Secretary, any other person authorised by the Board or by the Chairman in this behalf shall record the proceedings.

ii. The Chairman has absolute discretion to exclude from the Minutes, matters which in his opinion are or could reasonably be regarded as defamatory of any person, irrelevant or immaterial to the proceedings or which are detrimental to the interests of the company.

iii. Minutes shall be written in clear, concise and plain language, in third person and past tense.

iv. Each item to be numbered.

v. Minutes need to be maintained in Minutes book.

vi. Separate book to be maintained for each type of meeting – members, creditors, etc.

vii. Resolutions passed by postal ballot shall be recorded in the Minutes book of General Meetings.

viii. Minutes may be maintained in electronic form or physical form, in the manner prescribed under the Act.

ix. Minutes maintained in electronic form must be maintained with time stamp.

x. The pages of the Minutes Books shall be consecutively numbered.

xi. Pages left blank to be scored out and signed by Chairman who signs the minutes.

xii. There shall be a proper locking device to ensure security and proper control to prevent removal or manipulation of the loose leaves.

xiii. Minutes Books shall be kept at the Registered Office of the company or at such other place, as may be approved by the Board and shall be preserved permanently in physical or in electronic form with Timestamp.

Minutes of general meetings – Contents of Minutes

Minutes shall state, at the beginning,

i. name of the company,

ii. day,

iii. date,

iv. venue, and

v. time of commencement and conclusion of the Meeting.

Minutes shall also state in alphabetical order or in any other logical manner, but in either case starting with the name of Chairperson, names of Director and Company Secretary present at the meeting.

In case of resolutions passed by e-voting or postal ballot, minutes to contain:

i. a brief report on the e-voting or postal ballot conducted including the

ii. Resolution proposed

iii. Result of voting

iv. Summary of scrutinizer report

Minutes of general meetings – Contents of Minutes contd….

Minutes shall also contain details about:

i. Election of Chairman, if any

ii. Documents, registers and reports available for inspection at meeting

iii. Presence of quorum

iv. Number of members present in person and proxy (including details of shares represented by them) including representatives.

v. Presence of chairman of various committees and auditors (statutory and secretarial)

vi. Summary of the opening remarks of the Chairman

vii. Reading of qualifications in the audit reports

viii. Summary of the clarifications provided on various Agenda Items.

ix. In respect of each Resolution, the type of the Resolution, the names of the persons who proposed and seconded and the majority with which such Resolution was passed.

x. In the case of poll, the names of scrutinizers appointed and the number of votes cast in favour and against the Resolution and invalid votes.

xi. If the Chairman vacates the Chair in respect of any specific item, the fact that he did so and in his place some other Director or Member took the Chair.

Minutes of general meetings – Entry in minutes book and signing

i. Minutes shall be entered in the Minutes Book within

ii. 30 days from the date of conclusion of the Meeting, which date shall be recorded by the Company Secretary or any other person authorised by the Board in the absence of Company Secretary.

iii. Minutes once entered in the books cannot be altered.

iv. Minutes of a General Meeting shall be signed and dated by the Chairman of the Meeting or in the event of death or inability of that Chairman, by any Director who was present in the Meeting and duly authorised by the Board for the purpose, within 30 days of the General Meeting.

v. The Chairman shall initial each page of the Minutes, sign the last page and append to such signature the date on which and the place where he has signed the Minutes.

vi. Any blank space in a page between the conclusion of the Minutes and signature of the Chairman shall be scored out.

Minutes of general meetings – Inspection and Extracts

i. Directors and Members are entitled to inspect the Minutes of all General Meetings including Resolutions passed by postal ballot.

ii. The Company Secretary in Practice appointed by the company, the Secretarial Auditor, the Statutory Auditor, the Cost Auditor or the Internal Auditor of the company can inspect the Minutes as he may consider necessary for the performance of his duties.

iii. Extract of the Minutes shall be given only after the Minutes have been duly signed else the resolution extracted has to be certified by the Chairman or any Director or the Company Secretary.

CAclubindia

CAclubindia