This year Independence Day celebrations began in advance! With the approval of Companies Bill by Rajya Sabha (the Upper house of Parliament), Corporate India has found its true independence. Indian Corporate Sector which was reeling under the age old Companies Act, 1956 has got a fresh lease of life and the old legislation has got the much deserved adieu. Finally all the hype and speculation on the subject has been laid to rest and the gates to a new legislative era have been opened – an era for a more responsible democracy. As we all await the President’s assent for the bill to become an act, let us have a quick refresher on the main highlights of the Companies Bill.

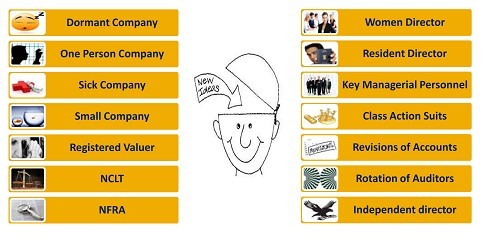

SOME NEW CONCEPTS INTRODUCED BY THE BILL IN THE COMPANIES ACT

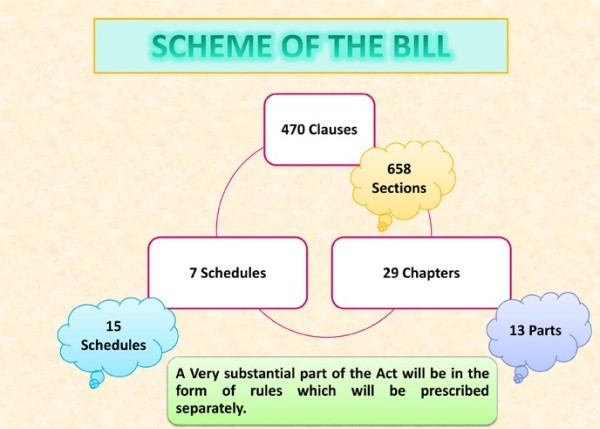

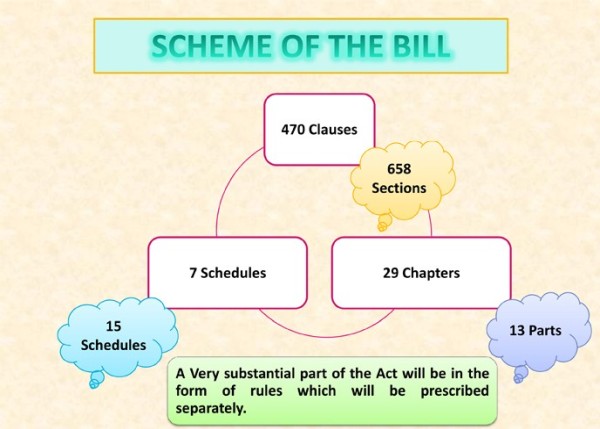

CHAPTER-WISE MAJOR HIGHLIGHTS

INCORPORATION

• Maximum number of members for private companies increased to 200

• Requirement of bifurcation of object clause of MOA removed

• Registered office address to be furnished within 15 days of incorporation.

• Verification of registered office made mandatory

• Commencement of business made applicable to all companies

SHARES AND SHARE CAPITAL

• Issue of shares at discount prohibited except in case of sweat equity

• Issue of preference shares, exceeding 20 years maturity, permitted for infrastructure projects.

• Specific provisions introduced for issue of shares on private placement, bonus shares and GDRs

• Consolidation and division which results in changes in the voting percentage of shareholders shall require approval of the Tribunal to be effective

BOARD MEETINGS

• All companies required to hold first board meeting within 30 days of incorporation.

• Length of notice for calling board meeting specified (at least 7 days notice to be given).

• Period between two board meetings not to exceed 120 days.

• Board Meeting through video conferencing permitted.

ANNUAL GENERAL MEETINGS

• Provision regarding holding AGM within 18 months of incorporation done away with.

• AGMs to be called during business hours on days other than national holidays.

• 21 days clear notice to be given for calling AGM by all companies (both physical and electronic form permitted)

• Quorum requirement for public company changed; quorum to be based on number of share holders in the company

No mention regarding holding of statutory meeting!

DIRECTORS / BOARD OF DIRECTORS

• Maximum number of directors that a company can have increased from 12 to 15.

• Maximum number of directorships a person can hold raised from 15 to 20 (maximum 10 of public companies). Limit to include private companies, alternate directorship etc.

• Concept of women director, independent director and resident director introduced.

• Directors’ responsibility statement enlarged.

• Disclosure in Board’s report to share holders made more widespread. S Dhanapal & Associates Practising Company Secretaries

FINANCIAL STATEMENTS / ACCOUNTS

• Consolidation of accounts made mandatory for all companies having subsidiaries. Subsidiary companies include Associate and Joint Ventures also.

• Financial statements can be signed by Chairman alone if so authorised by the Board.

• Financial year to end on 31st March every year for all companies. No explicit provision regarding extension of financial year is given.

• Provision introduced for revision and re-opening of books of accounts.

• Maintenance of accounts in electronic form permitted.

• Financial statements mean balance sheet, profit & loss and cash flow statement.

AUDITORS

Appointment:

• Listed Companies - Individual Auditor to retire every five years. Ten years in case of firm of Auditors

• Other Companies - Auditor to be appointed for a term of 5 years in each appointment. Appointment to be ratified in each AGM.

Favourable Clauses:

• Internal audit may be made mandatory for prescribed companies

• The limit in respect of maximum number of companies in which a person may be appointed as auditor has been proposed as twenty companies

Restrictive Clauses:

• Auditors not to render other services like book keeping, accounting etc. directly or indirectly to the company or its holding company or subsidiary company

• Members of a company may resolve to provide that in the audit firm appointed by it, the auditing partner and his team shall be rotated at such intervals as may be resolved by members.

I. Auditors to attend all general meetings unless specifically exempted by the company.

II. Company to file intimation of appointment of auditor with Registrar within 15 days of meeting in which appointed.

III. On resignation, auditor to file statement with company and Registrar within 30 days.

INSPECTION, INQUIRY & INVESTIGATION

o Statutory status to SFIO proposed and SFIO is given wide powers

o SFIO’s report to be treated as report filed by Police Officer

o SFIO will have power to arrest in certain cases which attract punishment for Fraud and person accused of such offence shall be released on bail subject to conditions as mentioned in the relevant provisions of this bill.

o Protection of employees during investigation by the authority is provided

o During inquiry and investigation or on request of creditor having due of more than one lakh, the central government may by order direct that transfer, removal or disposal of funds, assets, properties of the company shall not take place during such period not exceeding three years or may put restrictions and conditions as deemed fit

o Foreign companies are also covered.

PREVENTION OF OPRESSION & MISMANAGEMENT

o Concept of class action suits introduced.

o Relief can be sought for past concluded acts also.

o Definition of “fraud” introduced for first time and stringent penalty prescribed where fraud is proved.

COMPROMISES AND ARRANGEMENTS

o Simplified procedure for compromise or arrangement between two or more small companies or between holding and wholly owned subsidiaries introduced.

o Cross border mergers permitted.

o New terminologies “merger by absorption” and “Merger by formation of a new company” introduced.

o A company registered under Section 8 of the New Act (non-profit companies) shall amalgamate only with another company registered under that section and having similar objects.

o Certificate from company secretary/chartered accountant/cost accountant in practice is required to be filed with Registrar in such form as to whether the scheme is being complied in accordance with the orders of tribunal or not.

o Objections to the compromise or arrangement shall be made only by persons holding not less than 10% of shareholding or having outstanding debt amounting to not less than 5% percent of total outstanding debt as per the latest audited financial statement.

o Auditor of the company shall confirm that, accounting treatment proposed in scheme of compromise or arrangement is in conformity with Accounting standards prescribed under section 133.The certificate needs to be filed with tribunal.

o The Central Government shall, by notification, constitute, a Tribunal to be known as National Company Law Tribunal and an Appellate Tribunal to be known as National Company law Appellate Tribunal.

SECRETARIAL AUDIT AND CSR

Secretarial Audit

• Secretarial Audit mandated for all listed companies and certain other class of companies.

• Board to respond to qualifications contained in Secretarial Audit by means of explanation in Board’s report.

Corporate Social Responsibility

• Followings Companies Shall constitute a CSR Committee:

a. Net worth of rupees five hundred crore or more, or

b. Turnover of rupees one thousand crore or more, or

c. Net profit of rupees five crore or more

• Committee to consist of at least three directors out of which at least one should be independent director

• Board to ensure that at least 2% of the average net profits of last 3 years is spent by the company on CSR activities every financial year, else reasons for not spending to be specified in the Board’s report.

RECAP FOR PROFESSIONALS

(Chartered Accountants, Company Secretaries and Cost Accountants)

AUDITORS

Maximum tenure of appointment in case of listed companies specified. Five years for Individual auditors and ten years for firm of auditors

For unlisted companies, each appointment is made for a term of 5 years subject to annual ratification by members. Same audior can be re-appointed.

Maximum number of companies which an auditor can audit has been kept at 20.

Internal audit mandatory for certain class of companies to be specified.

Auditors to attend all AGMs unless specifically exempted by company.

Auditors cannot render other services like book keeping etc. to the company which they are auditing.

Bill provides for establishment of NFRA.

Procedure for appointment and resignation of auditors rationalised.

COMPANY SECRETARIES

Company Secretary included within the definition of Key Managerial Personnel.

Certain Companies , as may be prescribed, to mandatorily appoint company secretary

For all the companies (except one person companies and small companies), whether private or public, listed or unlisted, the annual return has to be signed by either a company secretary in employment or by a company secretary in practice.

Listed companies to annex secretarial audit report obtained from a Practising Company Secretary to the Board's report.

Secretarial Standards introduced and provided statutory recognition for the first time.

Company Secretary to ensure that the company complies with the applicable Secretarial Standards.

Functions of company secretary defined in the bill.

COST ACCOUNTANTS

Cost auditing standards’ have been mandated.

Central Government may direct that the audit of cost records of class of companies, which are required to maintain cost records and which have a net worth of such amount as may be prescribed or a turnover of such amount as may be prescribed, shall be conducted in the manner specified in the order.

The Central Government after consultation with regulatory body may direct class of companies engaged in production of such goods or providing such services as may be prescribed to include in the books of accounts particulars relating to utilisation of material or labour or to such other items of cost.

S Dhanapal & Associates

Practising Company Secretaries

Suite No.103, First Floor, Kaveri Complex,

96/104, Nungambakkam High Road,

(Next to Ganpat Hotel & ICICI Bank),

Nungambakkam, Chennai - 600 034

Email Id. csdhanapal@gmail.com

CAclubindia

CAclubindia