Dear Professional Colleagues,

No Service tax on free Pick-up/Home delivery of food, being ‘Sale’ in nature – Chandigarh Commissionerate

Background:

The Government vide Entry No. 19 of the Mega Exemption Notification No. 25/2012-ST dated June 20, 2012 (“the Mega Exemption Notification”) granted exemption from payment of Service tax to Restaurants, eating joint or a mess providing service in relation to food or beverages, other than those having:

- Facility of air-conditioning or central air-heating in any part of the establishment, at any time during the year, and

- License to serve alcoholic beverages.

Thus all AC Restaurants having license to serve liquor were exigible to Service tax.

Subsequently w.e.f April 1, 2013, Entry No. 19 of the Mega Exemption Notification was amended by Notification No. 3/2013-ST dated March 1, 2013 which deleted the point (ii) thereof. Accordingly, after such amendment, Service tax is levied even on the Restaurants which do not have a license to serve alcoholic beverages. This was a major change for the Industry as thousands of Restaurants and eating joints including small and medium came within the ambit of Service tax by such amendment.

However, questions were raised whether Take-away or Home delivery of food from Restaurants, such as McDonald’s, Domino’s, Pizza Hut etc., would also attract Service tax, as most of these have air-conditioned dining space and some of these outlets have dedicated counters outside air-conditioned halls for Take-away orders. A view was entertained that Take-away or Home-delivery Orders should not be taxed since no services, amenities etc. of the Restaurants were being offered to the customers in case of Take-away or Home delivery of food. But, in the absence of any clarification, the Restaurants continue to levy Service tax on the same.

Clarification by Chandigarh Commissionerate:

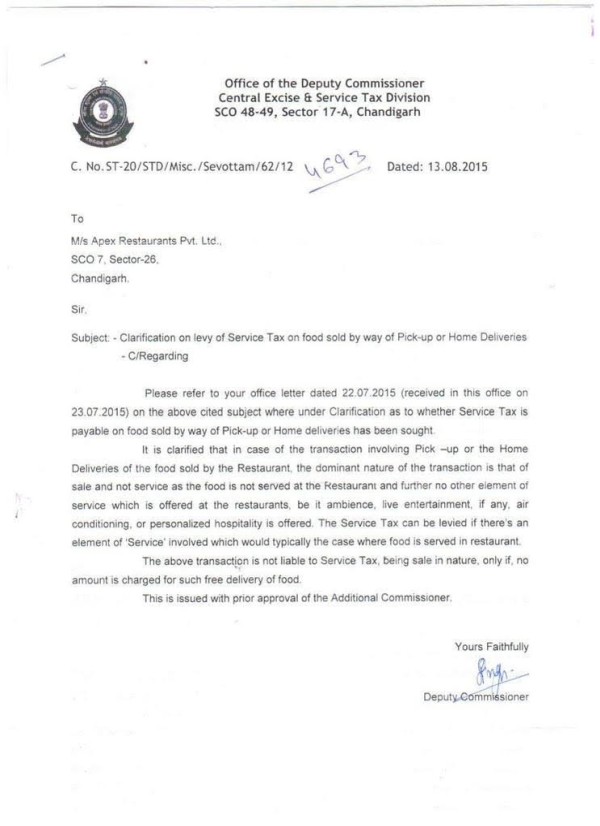

The Service Tax Department of Chandigarh vide its letter C.No. ST-20/STD/Misc./Sevottam/62/12/4693 dated August 13, 2015 (“the Clarification”) has clarified that free Home delivery/ Pick-up of food is not liable to Service tax.

The Department explained the matter further by stating that the dominant intention of such transaction is that of ‘Sale’ as food is not served at Restaurant and no other element of service such as ambience, live entertainment (if any), air conditioning or personalised hospitality is offered. It is further stated that Service tax can be levied if there’s an element of ‘Service’ involved which would typically be the case where food is served in Restaurant.

However, the Department has further clarified that the above transaction is not liable to Service tax, being sale in nature, only if no amount is charged for such free delivery of food.

Our Comments:

Similar Clarification on the stated matter is much needed from the Central Board of Excise and Customs (“CBEC”), so that it could be made applicable uniformly throughout, irrespective of the jurisdiction of particular Department.

Complete Clarification

Hope the information will assist you in your Professional endeavours. In case of any query/ information, please do not hesitate to write back to us.

Thanks & Best Regards,

Bimal Jain

FCA, FCS, LLB, B.Com (Hons)

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice or recommendation of firm. Neither the authors nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this document nor for any actions taken in reliance thereon.

Readers are advised to consult the professional for understanding applicability of this article in the respective scenarios. While due care has been taken in preparing this document, the existence of mistakes and omissions herein is not ruled out. No part of this document should be distributed or copied (except for personal, non-commercial use) without our written permission.

CAclubindia

CAclubindia