A. RATES OF INCOME-TAX

Rates of income-tax in respect of income liable to tax for the assessment year 2026-27 for the purposes of the Income-tax Act, 1961.

In respect of income of all categories of assessees liable to tax for the assessment year 2026-27, the rates of income-tax have either been specified in specific sections of the Income-tax Act, 1961 (like section 115BAA or 115BAB for domestic companies, section 115BAC for individual/Hindu undivided family (HUF)/Associations of Persons (AOP) (other than a co-operative society)/Body of Individuals (BOI)/Artificial Juridical Person (AJP) and section 115BAD or 115BAE for cooperative societies) or have been specified in Part I-A of the First Schedule to the Bill. There is no change proposed in tax rates either in these specific sections or in the First Schedule. The rates provided in sections 115BAA or 115BAB or 115BAC or 115BAD or 115BAE of the Act for the assessment year 2026-27 would be same as already enacted. Similarly, rates laid down in Part III of the First Schedule to the Finance Act, 2025, for the purposes of computation of “advance tax”, deduction of tax at source from “Salaries” and charging of tax payable in certain cases for the financial year 2025-26 would now become Part I of the First Schedule.

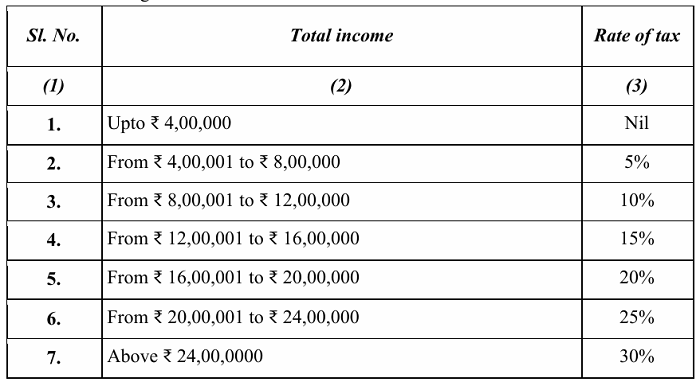

Tax rates under section 115BAC of the Income-tax Act, 1961

For assessment year 2026-27, as per the provisions of section 115BAC(1A) of the Income-tax Act, 1961, an individual or Hindu undivided family or association of persons [other than a co-operative society], or body of individuals, whether incorporated or not, or an artificial juridical person referred to in section 2(31)(vii), has to pay tax in respect of the total income at following rates:

The above-mentioned rates shall apply, unless an option is exercised as per provisions of section 115BAC(6). Thus, rates specified in section 115BAC(1A) are the default rates.

In respect of income chargeable to tax under section 115BAC(1A)(iii), the income tax for the assessment year 2026-27 shall be increased by a surcharge, for the purposes of the Union, computed, in the case of every individual or Hindu undivided family or association of persons, or body of individuals, whether incorporated or not, or every artificial juridical person referred to in section 2(31)(vii) of the Act,

(i) having a total income (including the dividend income or capital gains under the provisions of section 111A, section 112 and section 112A of the Income-tax Act, 1961)exceeding fifty lakh rupees but not exceeding one crore rupees, at the rate of 10% of such income-tax;

(ii) having a total income (including the dividend income or capital gains under the provisions of section 111A, section 112 and section 112A of the Income-tax Act, 1961) exceeding one crore rupees but not exceeding two crore rupees, at the rate of 15% of such income-tax;

(iii) having a total income (excluding the dividend income or capital gains under the provisions of section 111A, section 112 and section 112A of the Income-tax Act, 1961) exceeding two crore rupees, at the rate of 25% of such income-tax;

(iv) having a total income (including the dividend income or capital gains under the provisions of section 111A, section 112 and section 112A of the Income-tax Act, 1961) exceeding two crore rupees, but is not covered under clause (iii) above, at the rate of 15% of such income-tax;

3.1 In case where the provisions of section 115BAC(1A) are applicable and the total income includes any dividend income or capital gains under the provisions of section 111A, section 112 and section 112A of the Income-tax Act, 1961, the rate of surcharge on the income-tax in respect of that part of income shall not exceed 15%.

3.2 Further, in the case of an association of persons consisting of only companies as its members, and having its income chargeable to tax under section 115BAC(1A), the rate of surcharge on the income-tax shall not exceed 15%.

3.3 Marginal relief shall be provided in such cases.

For full details: click here

CAclubindia

CAclubindia