The Central Government has issued Exemption Notification No. 8/2017-CT(Rate) dated 28-06-2017 giving relaxation to Registered Persons under GST from major (and draconian) compliance required under section 9(4) of the CGST Act, 2017.

As per Section 9(4), every registered person (including composition dealer u/s 10) is required to pay GST on every inward supply (purchase) of goods or services from any unregistered person. The implication of this provision is that even if a registered person book expense of Rs. 10 say for tea/snacks in his accounts, he is required to pay tax on the same under reverse charge mechanism. The entire trade & industry has been vehemently protesting against this provision because of enormous compliance burden which had the potential to stop buying goods or procuring services from unregistered persons who may be a very small local vendor!!

To overcome this difficulty, the above notification issued u/s 11(1) exempts intra-State supplies of goods or services or both received by a registered person from any supplier, who is not registered, from the whole of the Central Tax leviable thereon under sub-section (4) of section 9 of the Central Goods and Services Tax Act, 2017.

The said exemption which shall be applicable from the date of roll out of GST i.e. from 1st July, 2017 restricts the exemption for value upto Rs. 5000 per day where the aggregate value of such supplies of goods or service or both received by a registered person from any or all the suppliers, who is or are not registered, exceeds five thousand rupees in a day.

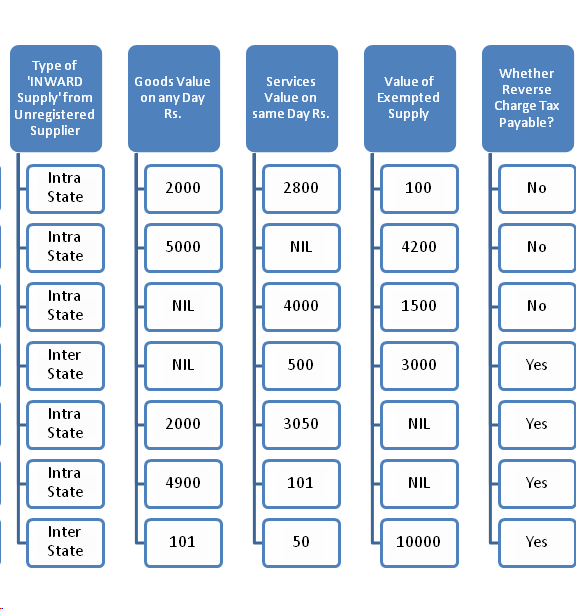

In simple words, if the total value of inward supply of goods or services or both in a single day from unregistered persons exceed Rs. 5000, then the registered person has to pay tax on total value under reverse charge. It is pertinent to note that the limit is not per supplier but from all such suppliers during the day. That means, if the value of inward supply from unregistered persons in a day is say Rs. 5100, then tax is payable on total Rs. 5100 and not on the excess i.e. Rs. 100.

There may be a situation when such inward supply include both exempted goods/services and taxable goods/services. In such cases, the value of exempted goods or services shall be ignored for calculating the aggregate value of Rs. 5000 per day. Irrespective of Value, no tax under reverse charge is payable for inward supply of any goods or services which is exempted u/s 11.

The author is of the view that the limit of Rs. 5,000 per day is very low and the government should had exempted atleast Rs. 10,000 per day as suggested in the exemption schedule released by it. Though small registered taxpayers would be immensely benefited by this exemption, the same won’t be able to provide much relief to the medium & large size assessee's who require to pay much more than Rs. 5000 for day-to-day expenses to small vendors/suppliers.

Also, similar notification must be issued by every State Governments so that the parallel relief is available for State Tax (SGST) which is most likely to be issued very soon. Unless, similar notification is issued by States, there won’t be any relaxation in compliance for the taxpayer.

Assuming that States also exempt State Tax by issuing parallel notification u/s 11, the various scenarios under which the said exemption shall be eligible is shown in the below chart for easy understanding:-

Disclaimer: This article is the property of the author. No one shall publish, copy or reproduce it in any manner, for any purposes without the written permission of the author provided that it can be shared with due credit to the author. The author shall not be responsible or liable for anything done or omitted to be done on the basis of this article, which is solely for information purpose.

CAclubindia

CAclubindia