PROVISIONS CONTAINED IN COMPANIES ACT, 2013 READ WITH DRAFT RULES

Companies Act 2013 has tightened many of the lose ropes prevailing in the Companies Act of 1956. One such area where the provisions have been made more stringent is “Issue of shares with differential voting rights”. Under the Companies Act, 1956, conditions relating to issue of shares with differential voting rights were not applicable to private companies. In

other words, private companies were free to issue equity shares with differential voting rights in accordance with the provisions contained in their articles of association without having to comply with any additional requirements of the Act. However, there has been a change in the scenario now and under the Companies Act, 2013, the provisions and conditions relating to issue of shares with differential voting rights are applicable to both private and public companies. In the current write up, the provisions relating to issue of equity shares with differential voting rights, as contained in the Companies Act, 2013 read with the draft rules, have been given in a concise manner.

Definition of Share:

As per Section 2(84) “share” means a share in the share capital of a company and includes stock;

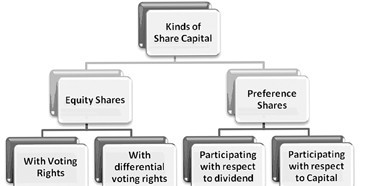

Kinds of Share Capital

As per Section 43, Share Capital in case of company limited by shares can be of following types:

1. Equity Share Capital - equity share capital, with reference to any company limited by shares, means all share capital which is not preference share capital.

Equity Share Capital can be further subdivided into:

- Equity Shares with Voting Rights, and

- Equity Shares with Differential Voting Rights as to dividend, voting or otherwise.

2. Preference Share Capital - preference share capital, with reference to any company limited by shares, means that part of the issued share capital of the company which carries a preferential right with respect to payment of dividend and repayment of capital.

Preference Share Capital may also have following rights:

- In respect of dividends, in addition to the preferential rights to dividend, a right to participate, whether fully or to a limited extent, with capital not entitled to the preferential right to dividend.

- In respect of capital, in addition to the preferential right to the repayment of capital on winding up, a right to participate, whether fully or to a limited extent, with capital not entitled to that preferential right in any surplus which may remain after the entire capital has been repaid.

PROVISIONS RELATING TO ISSUE OF EQUITY SHARES WITH DIFFERENTIAL VOTING RIGHTS

1. To issue equity shares with differential voting rights, following conditions must be complied with –

- The articles of association of the company authorizes the issue of shares with differential rights

- The issue of shares is authorized by a special resolution passed at a general meeting of the shareholders

- In case of listed companies, the issue of such shares shall be approved by the shareholders through postal ballot or a poll at a general meeting

- The shares with differential rights shall not exceed 25% of the total post-issue paid up equity share capital including equity shares with differential rights issued at any point of time

- The company has a track record of dividend payment of at least 10% for the last 3 financial years immediately preceding the financial year in which it is decided to issue such shares

- The company has not defaulted in filing financial statements and annual returns for 5 financial years immediately preceding the financial year in which it is decided to issue such shares

- The company has no subsisting default in the payment of a declared dividend to its shareholders or repayment of its matured deposits or redemption of its preference shares or debentures that have become due for redemption or payment of interest on such deposits or preference shares or debentures or repayment of any term loan from a public financial institution or State level financial institution or scheduled Bank that has become repayable or interest payable thereon or dues with respect to statutory payments relating to its employees to any authority

- The company has not been convicted of any offence under Reserve Bank of India Act, 1934, Securities and Exchange Board of India Act, 1992, Securities Contract Regulation Act, 1956, Foreign Exchange Management Act, 1999 or any other special Act.

2. Explanatory statement to be annexed to notice of general meeting or of a postal ballot must contain the following details:

- total number of shares to be issued with differential rights

- details of the differential rights

- percentage of the proposed issue of shares to the total post issue paid up equity share capital

- the reasons/justification for the issue

- price at which such shares are proposed to be issued

- basis on which the price has been arrived at

- in case of private placement or preferential issue - details of total number of shares proposed to be allotted to promoters, directors and key managerial personnel and details of total number of shares proposed to be allotted to persons other than promoters, directors and key managerial personnel and their relationship, if any, with any promoter, director or key managerial personnel

- in case of public issue - reservation, if any, for different classes of applicants including promoters, directors or key managerial personnel

- percentage of voting right which the equity share capital with differential voting right shall carry to the total voting right of the aggregate equity share capital

- scale or proportion in which the voting rights of such class or type of shares will vary

- change in control, if any, in the company that may occur consequent to the issue of equity shares with differential voting rights

- diluted Earning Per Share pursuant to the issue of such shares, calculated in accordance with the applicable accounting standards

- pre and post issue shareholding pattern along with voting rights in the format specified

3. The company shall not convert its existing equity share capital with voting rights into equity share capital carrying differential voting rights and vice–versa.

4. The Board of Directors shall, inter alia, disclose in the Board’s Report for the financial year in which the issue of equity shares with differential rights was completed, the following details:

- total number of shares allotted with differential rights and price at which these shares have been issued

- details of the differential rights relating to voting rights and dividends

- percentage of the issue of shares with differential rights to the total post issue equity capital and percentage of voting right which the equity share capital with differential voting right shall carry to the total voting right of the aggregate equity share capital

- particulars of promoters, directors or key managerial personnel to whom such shares are issued

- change in control, if any, in the company consequent to the issue of equity shares with differential voting rights

- diluted Earning Per Share pursuant to the issue of such shares, calculated in accordance with the applicable accounting standards.

- pre and post issue shareholding pattern along with voting rights in the format specified

5. The holders of the equity shares with differential rights shall enjoy all other rights such as bonus shares, rights shares etc., which the holders of equity shares are entitled to, subject to the differential rights with which such shares have been issued.

6. Where a company issues equity shares with differential rights, the Register of Members shall contain all the relevant particulars of the shares so issued along-with details of the shareholders.

CBDT Directive On Issue Of Refunds Without Adjustment Of Demand October 23rd, 2013

The Directorate of Income-tax (Systems) has issued a letter dated 22.10.2013 stating that pursuant to the decision of the full Board the process has been initiated to issue refunds without adjustment of demand as an interim measure in certain cases. The AOs have been requested to carry out necessary verification following the procedure prescribed in s. 245 of the Act.

Source: ITATONLINE.ORG

CBDT Directive Regarding Defective Returns For AY 2013-14 October 23rd, 2013

The Directorate of Income-tax (Systems) has issued a letter dated 22.10.2013 stating that about 1.46 lakh returns have been submitted for AY 2013-14 where the self-assessment tax was unpaid. It is stated that these returns are deemed defective under the law. The AOs have been requested to issue notices to the concerned assessees and follow-up to ensure that the unpaid self-assessment tax is deposited at the earliest.

Source: ITATONLINE.ORG

CS. S Dhanapal B.Com,B.A.B.L, F.C.S

Sr. Partner, S Dhanapal & Associates

Practising Company Secretaries, Chennai

(The author is a Chennai based Company Secretary. He can be reached at csdhanapal@gmail.com)

CAclubindia

CAclubindia