Introduction

Input Tax Credit is the backbone of this whole GST mechanism. GST is nothing but a value added tax on goods & services combined. It is the provisions of Input Tax Credit that make GST a value added tax i.e. collection of tax at all points after allowing credit for the inputs. As per the Revised Model GST Law dated 25-11-2016, “Input Tax Credit” has been defined in Section 2(56). It means Credit of “Input Tax” as defined in section 2 (55). As per section 2(55) of the Act, 'Input Tax' in relation to a taxable person, means the IGST, including that on import of goods, CGST and SGST charged on any supply of goods or services to him and includes the tax payable under sub-section (3) of section 8, but does not include the tax paid under section 9.

Section 8(3) levies tax on goods and/or services on reverse charge. Therefore, Input Tax is the tax paid by a taxable person under the Act whether under forward charge or reverse charge for the use of such goods and/or services in course or furtherance of his business.

Section 9 levies tax under composition scheme and the tax paid under composition scheme shall not be eligible for input tax.

Provisions relating to Input Tax Credit

Provisions relating to Input tax credit have been prescribed under Chapter V of the GST Act which is explained as under:

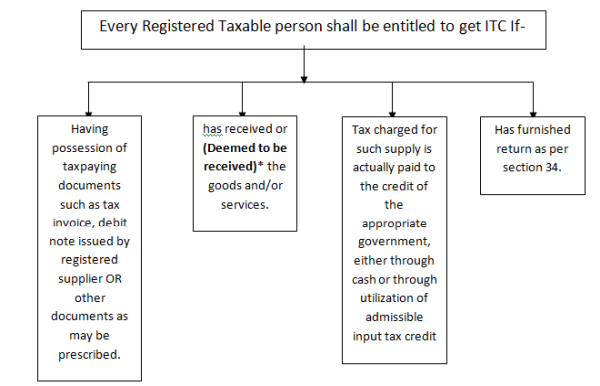

Section 16: Eligibility and conditions for taking input tax credit:

Every registered taxable person (subject to section 44) shall be entitled to take credit of input tax charged on any supply of goods or services to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger* of such person.

- An Input tax credit ledger in electronic form to be in the manner as may be prescribed in this behalf.

Proportionate credit of Input Tax- Credit of input tax in respect of pipelines and telecommunication tower fixed to earth by foundation or structural support including foundation and structural support thereto shall not exceed -

- 1st Year- One third of the total Input tax credit in the year of receipt of goods;

- 2nd Year- Two-third of the total input tax credit including the credit availed in the first financial year.

- The balance of the amount of credit in any subsequent year.

Conditions for availing Input Tax Credit

* Deemed to be received -when goods are delivered by supplier to recipient or other person as per the direction of taxable person or his agent by way of transfer of documents of title of goods or otherwise.

- If Goods received in lots/ installments, credit shall be allowed on receipt of last installment.

- Recipient of service is required to make payment to supplier within 3 months, otherwise ITC availed by the recipient shall be added to his output tax liability.

No ITC allowable on the tax component of the cost of capital goods on which depreciation has been claimed under the provisions of the Income Tax Act, 1961.

No ITC allowable for any invoice/debit note after furnishing return under section 34 for the month of September following the end of financial year to which the invoice/ debit note relates; or furnishing of annual return, whichever is earlier.

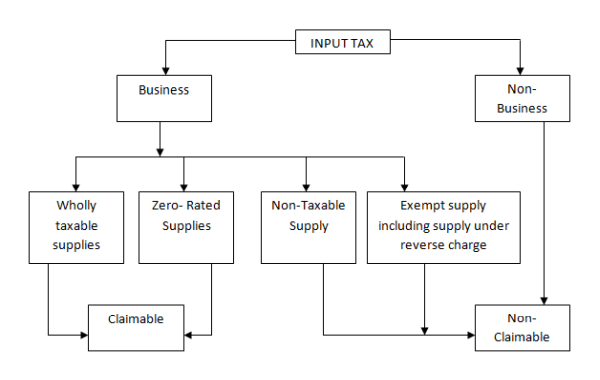

Section 17: Apportionment of credit and blocked credits

Apportionment of Credit- The goods and/or services are used by a registered taxable person partly for business and partly for non-business; he is eligible to take the input tax credit of goods and/or services attributable to the purposes of business.

Similarly, when the goods and/or services are used partly for effecting taxable supplies (Plus Zero-rated supplies) and partly for exempt supplies; he is eligible for credit attributable to the taxable supplies including Zero-rated supplies.

Same has been explained in the following chart:

Banking company or Financial Institution or NBFC (engaged in accepting deposits, extending loans or advances) has optional scheme - Either may avail 50 percent of eligible credit on input tax or may avail only proportionate credit as mentioned above(i.e. sub section 2 of this section). Option not to be withdrawn during the financial year.

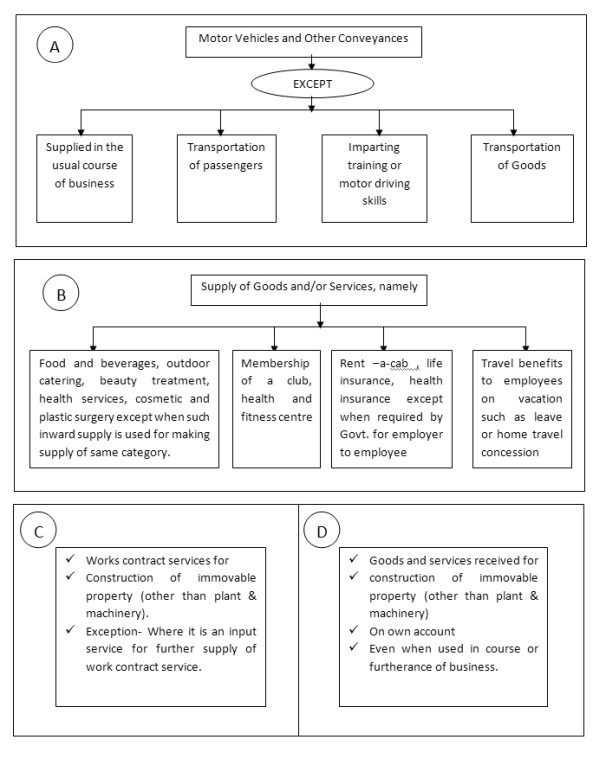

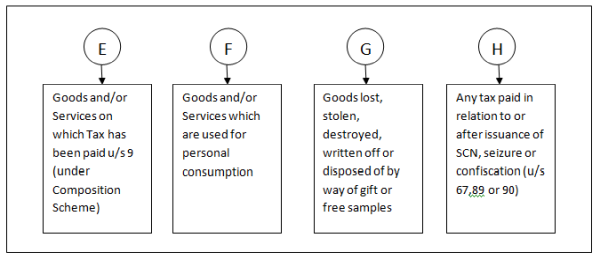

Blocked credits- There are some ineligible credits under GST which are explained in the following diagram:

Section 18: Availability of credit in special circumstances

The credit on inputs held in stock and inputs contained in semi-finished goods and finished goods held in stock is available in the following manner:

|

S.N. |

Eligible persons |

Credit entitled |

As on |

Restriction/conditions |

|

1 |

Person applied for registration within 30 days from the date of liability to pay tax, register and registered |

Inputs held in stock and inputs contained in semi-finished or finished goods held in stock |

The day immediately preceding the date from which he becomes liable to pay tax |

Cannot avail credit of goods and / or services after 1 year from tax invoice date The amount of credit calculated as per prescribed manner. The credit on capital goods shall be reduced by such percentage as may be prescribed. |

|

2 |

Person applied for registration after 30 days from the date of liability to pay tax, register and registered |

Nil |

NA |

|

|

3 |

Person who is not required to register, but obtains voluntary registration |

Inputs held in stock and inputs contained in semi-finished or finished goods held in stock and on capital goods |

The day immediately preceding the date of grant of registration |

|

|

4 |

Person ceases to pay composition tax |

Inputs held in stock and inputs contained in semi-finished or finished goods held in stock and on capital goods. |

The day immediately preceding the date from which he becomes liable to pay tax under regular scheme |

|

|

5 |

Exempt supply of goods or services by a registered taxable person becomes a taxable supply |

Inputs held in stock and inputs contained in semi-finished or finished goods held in stock relatable to such exempt supply and on capital goods exclusively used for such exempt supply |

The day immediately preceding the date from which such supply becomes taxable. |

In short, the credit of input tax can be taken as and when the person applies for the registration but the entitlement of credit of inputs would be from the day liability to tax arises.

Change in constitution of a taxable person due to sale merger, demerger, amalgamation, lease or transfer of business with provision for transfer of liabilities- the registered taxable person is allowed to transfer the input tax credit remaining unutilized in the books of accounts of such sold, merged, demerged, amalgamated, leased or transferred business

Reversal of credit on switching over to composition scheme / on goods becoming absolutely exempt- Credit to be reversed on inputs held in stock, inputs contained in semi finished goods or finished goods held in stock and on capital goods (reduced by prescribed percentage points) on the day immediately preceding the date of such switch over.

- Balance credit to lapse

- Computation method to be prescribed

Section 19: Recovery of Input Tax Credit and Interest thereon

Where credit has been taken wrongly, the same shall be recovered from the registered taxable person in accordance with the provisions of the Act.

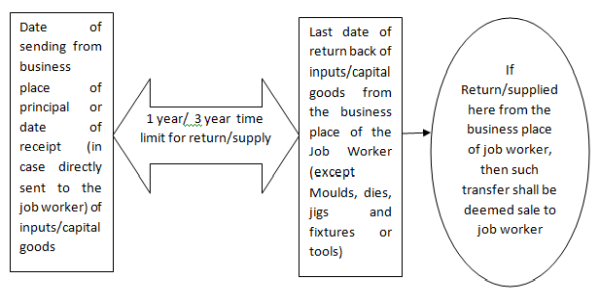

Section 20: Taking input tax credit in respect of inputs sent for job work

The principal can avail credit of input tax on goods sent to job worker subject to such conditions as may be prescribed.

However, the norms relating to input tax credit on inputs or capital goods sent for job work are given under GST which can be easily understood by the diagram as presented below:

CAclubindia

CAclubindia