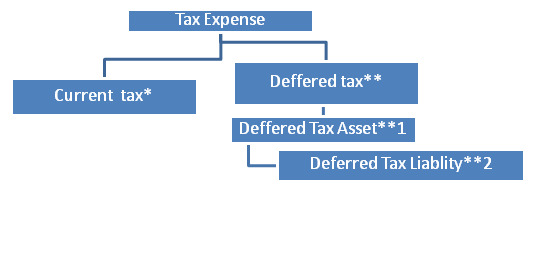

What is tax expense?

Tax expense (income) is the aggregate amount included for determination of profit and loss in respect of current tax and deferred Tax. Income tax relating to items charged or credited to other comprehensive income/equity is charged or credited accordingly to the respective equity. It is mapped out as follows.

*Current tax is the amount of tax payable (recoverable) computed in respect of taxable profit (tax loss) as per the per the applicable tax regime

** Deferred tax is recognised for the estimated future effects of temporary differences and tax loss carry forwards and recovered-- on undiscounted basis. Deferred tax liability/ Assetare classified as non- current in Balance Sheet.

**1 Deferred tax asset is recognised if it’s probable that it will be realised.

**2 Deferred Tax liabilities are the amounts of income tax payable in future periods in respect of taxable temporary differences.

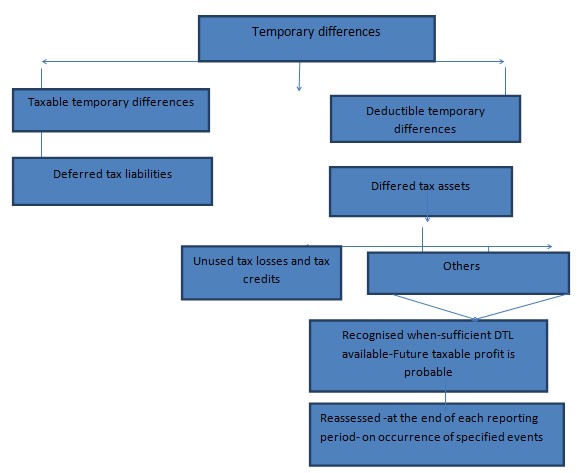

What are temporary differences?

Temporary differences are the differences between carrying amount of assets and liabilities in the statement of financial position and their corresponding tax bases. The tax base of an asset or liability is the amount accredited to corresponding tax bases. Temporary differences may be either

(a) taxable temporary differences, which are temporary differences that will result in taxable amounts in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled; or

(b) deductible temporary differences, which are temporary differences that will result in amounts that are deductible in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled.

By means of Chart, the same is illustrated below.

Whence Taxable temporary differences are not to be recognised?

A deferred tax liability shall be recognised for all taxable temporary differences. However, Ind.AS 12.15 forbids the recognition of deferred tax on taxable temporary differences that arise from:

- the initial recognition of goodwill, or

- the initial recognition of an asset or liability in a transaction which:

- is not a business combination, and

- at the time of the transaction, affects neither accounting profit nor taxable profit(tax loss).

Whence Deductible temporary differences are not to be recognised?

A deferred tax asset shall be recognised for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilised. However, Ind.AS 12.24 forbids the recognition of a deferred tax asset if that asset arises from the initial recognition of an asset or liability in a transaction that:

· is not a business combination, and

· at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

How temporary differences are measured and Accounted/ Presented in Financial Statements?

The temporary differences are measured at enacted or substantially enacted tax rates. Offset is possible when there is intention to settle net and legal right exist and entitled.

The deferred tax charge or credit for the year may arise from a number of sources as detailed hereunder--

- continuing operations within profit or loss

- discontinued operations within profit or loss

- other comprehensive income

- equity /goodwill

Accordingly, they are accounted and presented either in Profit and Loss or in Other Comprehensive Income or in Equity where the related transaction accounted, on undiscounted basis.

Deferred tax liability/Asset is classified as non- current in Balance Sheet.

How to determine whether offset is possible between deferred tax assets & liabilities?

As stated earlier, tax assets and liabilities must be recognised gross in the statement of financial position unless:

· the entity has a legally enforceable right to set off current tax assets against current tax liabilities, and

· the deferred tax assets and the deferred tax liabilities relate to income taxes levied by the same taxation authority on either:

a. the same taxable entity, or

b. different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realise the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities or assets are expected to be settled or recovered.

What’s the big difference between Ind.AS 12 on Income tax and AS 22?

While under the present Indian GAAP under As 22, recognition of tax consequences of differences between taxable income and accounting income is the basis to classify into permanent and timing differences, Ind. AS 12 requires recognition of tax consequences of differences between the carrying amounts of assets and liabilities and their tax base. This is the crux of the matter in the computation of differed tax under the new dispensation that may throw some challenges for accounting and auditing communities.

Also refer the earlier paragraphs on taxable/deductible temporary differences (Ind.As12.15/24)

What are the guide lines to utilise deferred tax assets for unused losses under Ind. AS--- any departure from the present GAAP in AS 22?

Again, it must be noted, that as per Ind. AS 12, deferred tax asset is recognised for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilised. The criteria for recognising deferred tax assets arising from the carry forward of unused tax losses and tax credits are the same that for recognising deferred tax assets arising from deductible temporary differences. However, the existence of unused tax losses is to be backed by strong evidence that future taxable profit may not be available. Therefore, when an entity has a history of recent losses, the entity recognises a deferred tax asset arising from unused tax losses or tax credits only to the extent that the entity has sufficient taxable temporary differences or there is convincing other evidence that sufficient taxable profit will be available against which the unused tax losses or unused tax credits can be utilised by the entity As per the existing AS 22, deferred tax assets are recognised and carried forward only to the extent that there is a reasonable certainty that sufficient future taxable income will be available against which such deferred tax assets can be realised. Where deferred tax asset is recognised against unabsorbed depreciation or carry forward of losses under tax laws, it is recognised only to the extent that there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which such deferred tax assets can be realised.

How to lever the deferred taxes on investments in subsidiaries, associates and in joint ventures?

A big question and hence challenge is to be met. Under the present GAAP, differed taxes are the arithmetical addition from the group companies. No adjustments are done in consolidation to this amount. But, aghast! How under Ind.AS? - A big challenge!

Under Ind. AS, deferred tax effect of intragroup eliminations is also recorded. For example, when unrealised profits are let off on unsold inventory purchased by a subsidiary from a parent, deferred taxes are recognised for the temporary difference that arise between the tax base (generally, the transaction value) and the carrying value in the consolidated financial statements (cost, after eliminating unrealised profits).

Likewise, under the present dispensation, deferred taxes are currently not recognised on the difference between the tax base of a parent or Investor’s investment in a subsidiary, joint venture or associate (generally, the cost of the investment) and the carrying value of the related investment in the parent’s consolidated financial statements. For example, the differences in tax base and carrying amount of investments issuing out of the existence of undistributed profits of a subsidiary, joint venture or associate, which affect the carrying amount of the investment but not itstax base. For example, when parent has control over the dividend policy of the subsidiary, but the intention is not to declare dividend, there may be no need to recognise DTL. But, take the case of an associate where parent does not control the dividend policy—there the investor may have to recognise DTL (Para 39 Ind.As12).

Regarding DTA, the investor in subsidiaries, branches and associates and interests in joint arrangements is permitted to recognise all deductible temporary differences only to the extent that, it is probable that: that the temporary difference will reverse in the foreseeable future and taxable profit will be available against which temporary differences can be utilised (Para 44 Ind. AS.12) based on the guidance given in Para 28 to 31 of the Ind. AS 12.

To sum up, Ind.AS, deferred taxes are also recognised on temporary differences arising from

- Elimination of profit and losses issuing out of intra-group transactions and

- With respect to undistributed profits of subsidiaries, associates and joint ventures

How to compute the amount of any deferred tax asset that can be recognised?

When there are sufficient taxable temporary differences relating to the same taxation authority and the same taxable entity which are expected to reverse: (a) in the same period as the expected reversal of the deductible temporary difference; or (b) in periods into which a tax loss arising from the deferred tax asset can be carried back or forward. In such circumstances, the deferred tax asset is recognised in the period in which the deductible temporary differences arise. Again, in evaluating whether it will have sufficient taxable profit in future periods, an entity ignores taxable amounts arising from deductible temporary differences that are expected to originate in future periods, because the deferred tax asset arising from these deductible temporary differences will itself require --future taxable profit in order to be utilised; or (b) tax planning opportunities are available to the entity that will create taxable profit in appropriate periods.

How to address the differed tax in a Business combination?

When tax base of the assets and liabilities acquired in business combination differ from the carrying amount—more so, when the identifiable assets and liabilities acquired are measured at fair value for initial recognition, differences may bound to arise especially when tax laws normally permit the recognition of an amount equal to the cost of the previous owner -taxable temporary difference arises which results in a deferred tax liability. The resulting deferred tax liability affects goodwill (see paragraph 66).

Many jurisdictions do not allow reductions in the carrying amount of goodwill as a deductible expense in determining taxable profit. Moreover, in such jurisdictions, the cost of goodwill is often not deductible when a subsidiary disposes of its underlying business. In such jurisdictions, goodwill has a tax base of nil. Any difference between the carrying amount of goodwill and its tax base of nil is a taxable temporary difference. However, Ind. AS 12.21 does not permit the recognition of the resulting deferred tax liability because goodwill is measured as a residual and the recognition of the deferred tax liability would increase the carrying amount of goodwill.

Deferred tax liabilities for taxable temporary differences relating to goodwill are, however, recognised to the extent they do not arise from the initial recognition of goodwill (Para 21B).

How an entity shall recognise acquired deferred tax benefits that it realises after the business combination? (Para 67)

(a) Acquired deferred tax benefits recognised within the measurement period that result from new information about facts and circumstances that existed at the acquisition date shall be applied to reduce the carrying amount of any goodwill related to that acquisition. If the carrying amount of that goodwill is zero, any remaining deferred tax benefits shall be recognised in other comprehensive income and accumulated in equity as capital reserve or recognised directly in capital reserve, depending on whether paragraph 34 or paragraph 36A of Ind. AS 103, would have applied had the measurement period adjustments been known on the date of acquisition itself.

(b) All other acquired deferred tax benefits realised shall be recognised in profit or loss (or, if this Standard so requires, outside profit or loss).

How to address Compound Deferred taxes on compound financial instruments?

Under Ind. AS, in case of compound financial instruments which have a dual component- to be precise-liability and an equity component (take the case of a convertible/preference shares/debentures) the interest cost in the financial statements would be different from the tax deductible interest (based on contractual terms of the instrument). This difference is temporary in nature and will lead to the recognition of deferred taxes which are initially recognised through equity and subsequently reversed through the profit and loss account over the maturity/conversion period.

What tax rate is used in measuring the deferred tax liability or asset related to a non- depreciable asset?

As per Ind.AS 12.51B, “If a deferred tax liability or deferred tax asset arises from a non-depreciable asset measured using the revaluation model in Ind. AS 16, the measurement of the deferred tax liability or deferred tax asset shall reflect the tax consequences of recovering the carrying amount of the non-depreciable asset through sale, regardless of the basis of measuring the carrying amount of that asset. Accordingly, if the tax law specifies a tax rate applicable to the taxable amount derived from the sale of an asset that differs from the tax rate applicable to the taxable amount derived from using an asset, the former rate is applied in measuring the deferred tax liability or asset related to a non-depreciable asset.”.

How to present current /deferred tax in financial statements?

According to Ind.As12.61A, current tax and deferred tax shall be recognised outside profit or loss if the tax relates to items that are recognised, in the same or a different period, outside profit or loss. Therefore, current tax and deferred tax that relates to items that are recognised, in the same or a different period:

(a) in other comprehensive income, shall be recognised in other comprehensive income (see paragraph 62).

(b) directly in equity, shall be recognised directly in equity (see paragraph 62A).

Indian Accounting Standards require or permit particular items to be recognised in other comprehensive income. Examples of such items as per Para 62 of Ind. AS 12 are:

(a) a change in carrying amount arising from the revaluation of property, plant and equipment (see Ind. AS 16); and

(b) exchange differences arising on the translation of the financial statements of a foreign operation (see Ind. AS 21).

Indian Accounting Standards require or permit particular items to be credited or charged directly to equity. Examples of such items as per Ind. AS 12.66 are:

(a) an adjustment to the opening balance of retained earnings resulting from either a change in accounting policy that is applied retrospectively or the correction of an error (see Ind. AS 8, Accounting Policies, Changes in Accounting Estimates and Errors); and

(b) amounts arising on initial recognition of the equity component of a compound financial instrument (see paragraph 23)

What about share based payments?

As regards transactions concerning payments of remuneration in the form of shares, share-options or by other equity instruments, the timing of allowable deduction of recognised expenses by tax laws of the concerned jurisdiction will determine whether or not deferred taxes will arise. In case tax authorities allow deduction of recognized expenses only when employees exercise share options that will result in recognition of DFA till the period employees will exercise their options or when shares are issued. In other words, tax laws of the concerned jurisdiction will determine the course of action.

Exchange differences on deferred foreign tax liabilities or assets(Para 78)

Ind. AS 21.78 requires certain exchange differences to be recognised as income or expense but does not specify where such differences should be presented in the statement of profit and loss. Accordingly, where exchange differences on deferred foreign tax liabilities or assets are recognised in the statement of profit and loss, such differences may be classified as deferred tax expense (income) if that presentation is considered to be the most useful to financial statement users.

A broad outline as to how to arrive at the tax base under Ind.AS 12 for each classification:

An attempt is made to give a broad outline as to how to arrive at the tax base under Ind.AS 12 for each classification( for details refer the standard). However, especially when there are entities under different tax regimes, an expert advice may have to be sought so as to decipher the correct line of approach to arrive at the tax base. Driven by the Ind. AS compliant Schedule III requirements, an attempt has been made to chart out in the tables below under each item on the face of the Balance Sheet. Since the tax rules, particularly for financial instruments are intricate, more often than not, it is always advisable to consult tax advisors before a final call is taken especially when different tax regimes are involved in a group as indicated earlier.

A on Non-Current Assets:

|

SR. No |

Non-Current Assets |

Tax base |

|

1a |

Property, Plant and machinery |

The land element always be assumed to be recovered through sale and therefore the tax base should be the indexed cost of the land. But, as per, Ind. AS 12. 51B, where the tax deduction available on sale of a property exceeds the accounting base (book value), the tax base should be restricted to the higher of original cost of the property and its accounting base. |

|

1b |

Plant and machinery |

Equal to the tax written down value of the assets. |

|

2 |

Investment property |

The land element to be always assumed to be recovered through sale and therefore the tax base should be the indexed cost of the land |

|

3a |

Goodwill |

Goodwill arising only on consolidation, ie not through an acquisition of trade and assets, will have a tax base of nil as no deductions will ever be allowed for this goodwill. except where there is tax relief for goodwill, the tax base will usually be equal to the accounting base. |

|

3b |

Other Intangible Assets. Software |

If there is accelerated tax relief for the software and the tax base of that item may, as a result be lower than the accounting base. |

|

3c |

Capitalised research and development |

Enhanced tax relief given for qualifying R&D expenditure when the cost is incurred rather than when it is expensed in the financial statements. Therefore, if tax relief has already been given, the tax base for the capitalised amount is nil. |

|

4 |

Financial Assets (i) Non-current investments (ii) Long-term loans and advances (iii) Others |

The tax base will depend on the nature of each item and hence to be worked out accordingly. Many financial instruments are accounted for on a fair value basis, where, as per tax law/ rules, tax gains and losses arise only on a sale subject to capital gains tax with a concessional rate, unless the company has chosen to elect out of these rules. Regarding instruments under amortised cost, tax base depends on actual interest paid under tax regime and the loan outstanding. |

B on Current Assets:

|

Sr. No |

Current Assets |

Tax base |

Remarks |

|

1 |

Inventories |

Same as carrying amount in the financial statements |

For any provision for doubtful tax base is Nil |

|

2 |

Trade and other receivables |

Same as carrying amount in the financial statements |

For any provision for doubtful tax base is Nil |

|

3 |

Current financial assets |

Depends on the nature of the item. |

More or less similar to non- current financial assets |

|

4 |

Cash and cash equivalents |

Equal to its carrying amount in the statement of financial position |

-------- |

C- on Current/ Non- current liabilities;

|

Sr. No |

Current/ Non- current liabilities Liabilities |

Tax base/ Remarks |

|

1 |

Trade and other Payables(Current liabilities) |

Generally same as the carrying value except where the expenditure is deductible only when paid |

|

2 |

· Short-term borrowings and current portion of · long-term borrowings(current) & · Long term borrowings(Non-current) |

Same as the accounting base. Where there are interest payments which are deductible in the future when they are paid, the tax base is arrived at by deducting the amount deductible in the future from the accounting base. |

|

3 |

· Short-term provisions(current) & · Long term Provisions(Non-Current) |

Equal to the accounting base provided does not relate to an item of disallowable expenditure. |

Disclosure requirements:

Extensive disclosures regarding deferred tax are required as spelt out in Para 79to 85 of Ind. As12. Ind. AS.79 requires the major components of tax expense (income) to be disclosed separately.

As per Ind. AS 12.80, the major components of tax expense may include -current tax expense; prior period tax adjustments; deferred tax relating to the origination and reversal of temporary differences; deferred tax expense relating to changes in tax rates or the imposition of new taxes; the amount of benefit arising from a previously unrecognised tax loss, tax credit or temporary difference of a prior period that is used to reduce current tax expense/ deferred tax; deferred tax expense arising from the write-down, or reversal of a previous write-down, of a deferred tax asset in accordance with paragraph 56; and the amount of tax expense/income relating to those changes in accounting policies and errors that are included in profit or loss in accordance with Ind. AS 8, because they cannot be accounted for retrospectively.

Besides, enormous additional disclosures are called for as per Ind.AS 12.81 to 85. The requirements of these paragraphs are to be tailored for necessarily disclosures and proper compliance. In the interest brevity, these requirements are referred to the standard

Sum up:

- In sum up, to successfully calculate the deferred tax as per Ind. AS 12, one has to go through the following stepladders step wise:

- Compute the accounting base of the asset or liability.

- Next step, to work out the tax base of the asset or liability.

- If there is no difference between tax and accounting base, no deferred tax is required.

- The next step forward is to Identify and calculate any exempt temporary differences.

- The ensuing onward step is to fix the relevant tax rate and apply this to calculate deferred tax Ind. As 12.51A

- Calculate the amount of any deferred tax asset that can be recognised

- Determine whether to offset deferred tax assets and liabilities

CAclubindia

CAclubindia