Pre-GST law for Educational Institutions

'Educational Institution' means an institution providing pre-school education and education up to higher secondary school or equivalent.

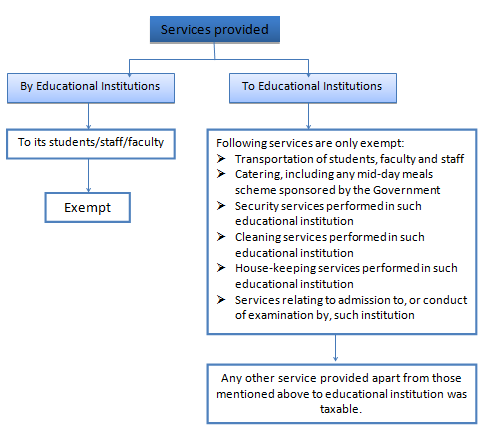

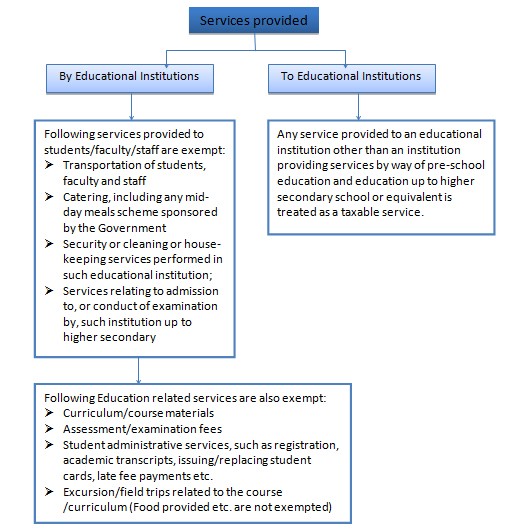

Any service provided to an institution other than Institution providing pre-school education and education up to higher secondary school or equivalent was taxable.

GST on Educational Institutions

Meaning of Educational Institution

Under GST, 'Educational Institution' is defined as an institution providing services by way of:

- Pre-school education and education up to higher secondary school or equivalent;

- Education as a part of a curriculum for obtaining a qualification recognized by any law for the time being in force;

- Education as a part of an approved vocational education course;

Taxability of Educational Services

Taxable supply means a supply of goods or services or both which is leviable to tax under GST

Exemptions available to Educational Institutions

Income from education is wholly exempt from GST if a charitable trust is running a school, college or education institution for abandoned, orphans, homeless children, physically or mentally abused persons, prisoners or persons over the age of 65 years or above residing in a rural area.

Government or local authority or governmental authority carrying on the activity of education is exempted from GST as this is not included in the ambit of supply of services. For Example – Government schools / Municipal schools.

Education provided by below are also Exempted Under GST:

- National skill development corporation set up by the Indian government

- National skill development corporation approved sector skill councils

- National skill development corporation approved assessment agencies

- The national skill development programs approved by NSDC Vocational skill development program approved under national skill certification and monetary reward scheme

- Any scheme implemented by NSDC with training partners

Exemption has also been granted to the services provided by the IIM

- 2 year full-time residential PG programs in Management for Post Graduate Diploma in Management, admission in which is granted via CAT

- Fellowship programs in Management

- 5 Year Integrated Programs in management studies (but excludes the Executive Development Program).

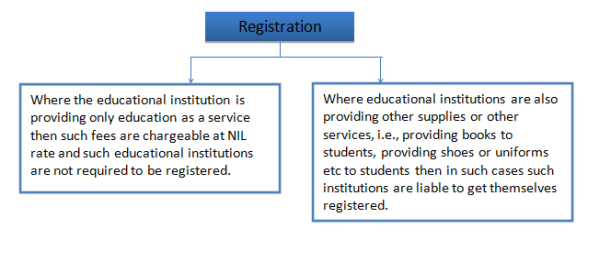

Registration of Educational Institutions

Services provided to higher educational institutions are taxable. While services provided by an educational institution are out of the GST ambit, the same is not the case with services provided to an educational institution.

The GST exemption on procurements is available only to schools (from pre-school up to higher secondary school or its equivalent). Hence, the ‘input’ or supply of services such as transportation, catering, housekeeping, services relating to admission or conduct of examination to higher educational institutions will bear GST levy. This will have to be borne by the higher educational institution.

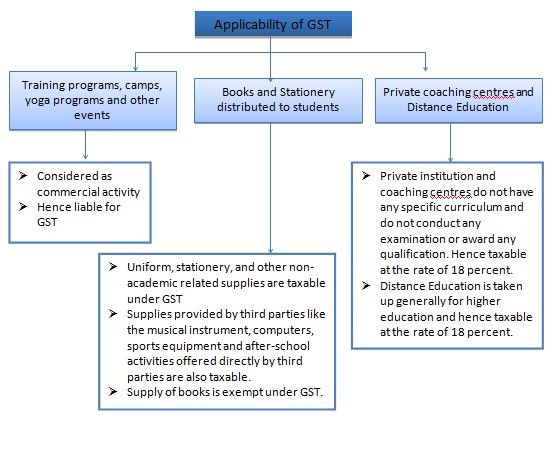

GST in different scenarios

CAclubindia

CAclubindia