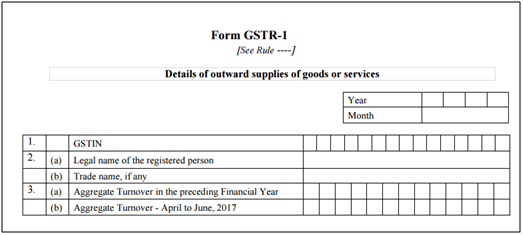

After GSTR 3B every registered tax payer in GST regime is looking forward for filling GSTR-1. According to the GST law, every registered taxable person is required to submit the details of outward supplies in the GSTR-1. This return is required to be filed within 10 days from the end of the tax period, or the transaction month

GSTR-1 has a total of 13 headings. However, the taxable person need not worry as most of these will be pre-filled. Before we dive deep into the various sections of this return, we need to understand certain terms. These are:

- GSTIN - Goods and Services Taxpayer Identification Number

- UID - Unique Identity Number for Embassies

- HSN - Harmonized System of Nomenclature for goods

- SAC - Services Accounting Code

- GDI - Government Department Unique ID where department does not have a GSTIN

- POS - Place of Supply of Goods or Services - State Code to be mentioned

2. Aggregate turnover of the taxpayer for the immediate preceding financial year and first quarter of the current financial year shall be reported in the preliminary information in Table 3. This information would be required to be submitted by the taxpayers only in the first year. Quarterly turnover information shall not be captured in subsequent returns. Aggregate turnover shall be auto-populated in subsequent years.

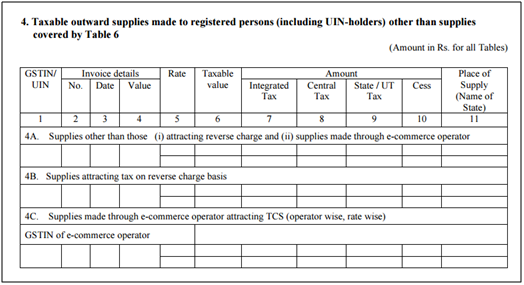

3. Invoice-level information pertaining to the tax period should be reported for all supplies as under:

(i) For all B to B supplies (whether inter-State or intra-State), invoice level details, rate-wise, should be uploaded in Table 4, including supplies attracting reverse charge and those effected through e-commerce operator. Outwards supply information in these categories are to be furnished separately in the Table.

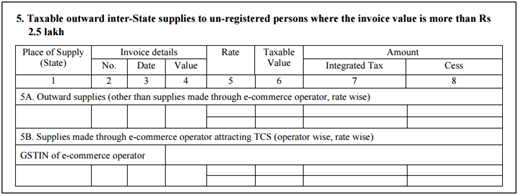

(ii) For all inter-State B to C supplies, where invoice value is more than Rs. 2,50,000/- (B to C Large) invoice level details, rate-wise, should be uploaded in Table 5; and

(iii) For all B to C supplies (whether inter-State or intra-State) where invoice value is up to Rs. 2,50,000/- State-wise summary of supplies, rate-wise, should be uploaded in Table 7.

4. Table 4 capturing information relating to B to B supplies should:

(i) be captured in:

a. Table 4A for supplies relating to other than reverse charge/ made through e-commerce operator, rate-wise;

b. Table 4B for supplies attracting reverse charge, rate-wise; and

c. Table 4C relating to supplies effected through e-commerce operator attracting collection of tax at source under section 52 of the Act, operator wise and rate-wise.

(ii) Capture Place of Supply (PoS) only if the same is different from the location of the recipient.

5. Table 5 to capture information of B to C Large invoices and other information shall be similar to Table 4. The Place of Supply (PoS) column is mandatory in this table.

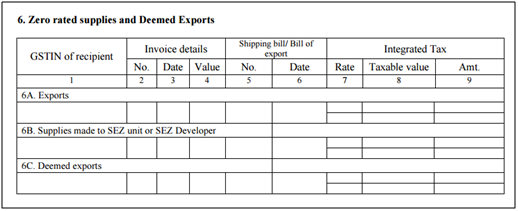

6. Table 6 to capture information related to:

- Exports out of India

- Supplies to SEZ unit/ and SEZ developer

- Deemed Exports

7. Table 6 needs to capture information about shipping bill and its date. However, if the shipping bill details are not available, Table 6 will still accept the information. The same can be updated through submission of information in relation to amendment Table 9 in the tax period in which the details are available but before claiming any refund / rebate related to the said invoice. The detail of Shipping Bill shall be furnished in 13 digits capturing port code (six digits) followed by number of shipping bill.

8. Any supply made by SEZ to DTA, without the cover of a bill of entry is required to be reported by SEZ unit in GSTR-1. The supplies made by SEZ on cover of a bill of entry shall be reported also by DTA unit in its GSTR-2 as imports in GSTR-2. The liability for payment of IGST in respect of supply of services would, be created from this Table.

9. In case of export transactions, GSTIN of recipient will not be there. Hence it will remain blank.

10. Export transactions effected without payment of IGST (under Bond/ Letter of Undertaking (LUT)) needs to be reported under “0” tax amount heading in Table 6A and 6B.

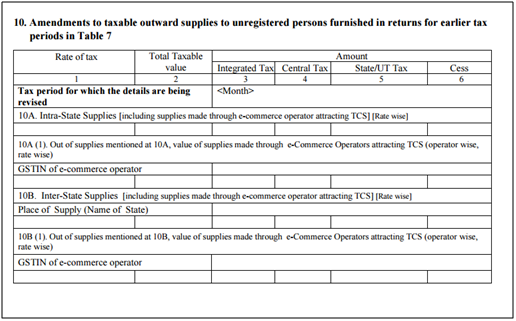

11. Table 7 to capture information in respect of taxable supply of:

(i) B to C supplies (whether inter-State or intra-State) with invoice value up to Rs 2,50,000;

(ii) Taxable value net of debit/ credit note raised in a particular tax period and information pertaining to previous tax periods which was not reported earlier, shall be reported in Table 10. Negative value can be mentioned in this table, if required;

(iii) Transactions effected through e-commerce operator attracting collection of tax at source under section 52 of the Act to be provided operator wise and rate wise;

(iv) Table 7A (1) to capture gross intra-State supplies, rate-wise, including supplies made through e-commerce operator attracting collection of tax at source and Table 7A (2) to capture supplies made through e-commerce operator attracting collection of tax at source out of gross supplies reported in Table 7A (1);

(v) Table 7B (1) to capture gross inter-State supplies including supplies made through e- commerce operator attracting collection of tax at source and Table 7B (2) to capture supplies made through e-commerce operator attracting collection of tax at source out of gross supplies reported in Table 7B (1); and

(vi) Table 7B to capture information State wise and rate wise.

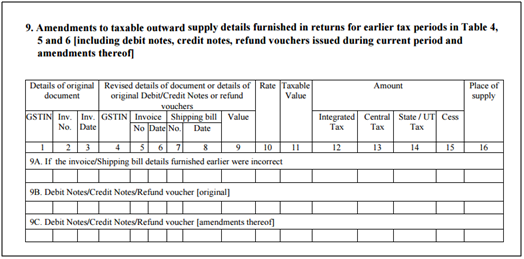

12. Table 9 to capture information of:

(i) Amendments of B to B supplies reported in Table 4, B to C Large supplies reported in Table 5 and Supplies involving exports/ SEZ unit or SEZ developer/ deemed exports reported in Table 6;

(ii) Information to be captured rate-wise;

(iii) It also captures original information of debit / credit note issued and amendment to it reported in earlier tax periods; While furnishing information the original debit note/credit note, the details of invoice shall be mentioned in the first three columns, while furnishing revision of a debit note/credit note, the details of original debit note/credit note shall be mentioned in the first three columns of this Table,

(iv) Place of Supply (PoS) only if the same is different from the location of the recipient;

(v) Any debit/ credit note pertaining to invoices issued before the appointed day under the existing law also to be reported in this table; and

(vi) Shipping bill to be provided only in case of exports transactions amendment.

13. Table 10 is similar to Table 9 but captures amendment information related to B to C supplies and reported in Table 7.

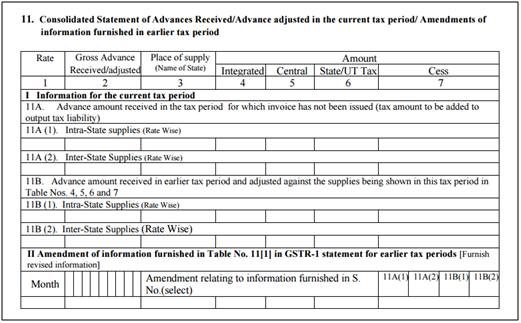

14. Table 11A captures information related to advances received, rate-wise, in the tax period and tax to be paid thereon along with the respective PoS. It also includes information in Table 11B for adjustment of tax paid on advance received and reported in earlier tax periods against invoices issued in the current tax period. The details of information relating to advances would be submitted only if the invoice has not been issued in the same tax period in which the advance was received.

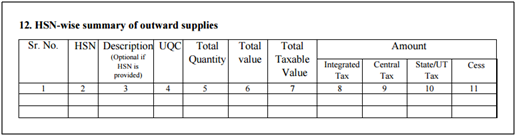

15. Summary of supplies effected against a particular HSN code to be reported only in summary table. It will be optional for taxpayers having annual turnover upto Rs. 1.50 Cr but they need to provide information about description of goods.

16. It will be mandatory to report HSN code at two digits level for taxpayers having annual turnover in the preceding year above Rs.1.50 Cr but upto Rs. 5.00 Cr and at four digits level for taxpayers having annual turnover above Rs. 5.00 Cr.

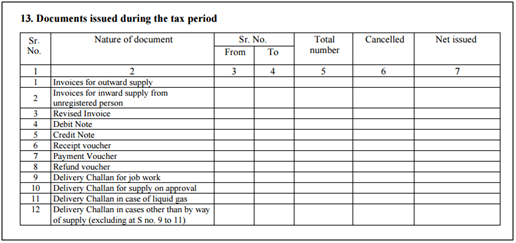

17. Documents issued during the tax period: This head will include details of all invoices issues in a tax period, any kind of revised invoice, debit notes, credit notes etc.

CAclubindia

CAclubindia