Introduction: -

After introduction of VAT, a large quantum of refund application have been filled. The Department under going transition due to which business process have undergone many changes. As result, a number of circular were issued from time to time to lay down the procedure for the granting of refund. As a further step towards E-Governance, the refund applications are now taken electronically and Mahavikas module for refund is now operational. The entire processing of refunds has now shifted on electronic platform. Further, section 51 of MVAT Act is amended to provide for grant of part refunds. Of late, some irregularities are noticed in granting of refunds at Palghar. Due to all these changes, it becomes necessary to review the process of grant of refunds so as to speed up the process of disbursement of refunds after proper scrutiny. Also, due to the existence of number of circulars, it sometime becomes difficult for dealers as well as departmental officers to keep a track of the circulars. Here, I have tried to simplify consolidate various articles & circulars on the Refund Process,so that we all can understood the same in an easiest way.

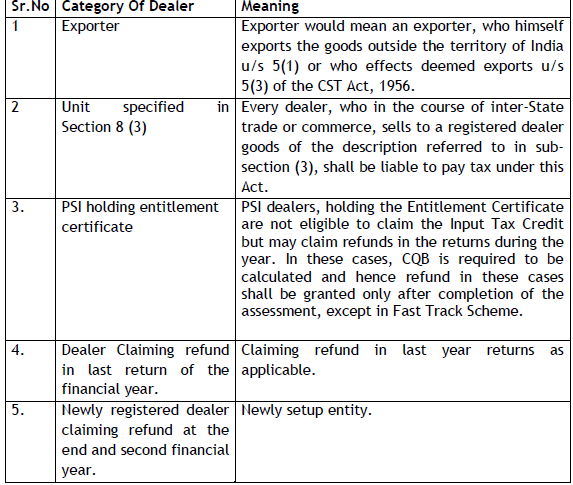

Eligibility for Grant Of Refund:-

The registered dealer may after the end of the year to which refund relates make an application in prescribed format to commissioner after receiving such application he may call any information required by him within 1 month. If we do not adjust the refund in return the commissioner shall on an application made by dealer under the subjective rules & provisions of MVAT Act grant refund of such amount to said dealer.

Interest on amount of refund: -

Where refund of any tax becomes due to a registered dealer, he shall, subject to rules, if any, be entitled to receive, in addition to the refund, simple interest at the prescribed rate on the amount of refund for the period commencing on the date next following the last date of the period to which the refund relates and ending on the date of the order sanctioning the refund or for a period of ‘Twenty Four’ months, whichever is less by virtue of the provisions contained in section 51 or by virtue of an order passed under any other provision of this Act, is not so refunded to him within ninety days of the end of the respective period provided in section 51 or, as the case may be, of the date of the said order, the Commissioner shall pay such person simple interest at the prescribed rate on the said amount from the date immediately following the expiry of the period of ninety days to the date of the refund.

The applicant dealer or person may supply to the said officer a certified copy of such order and if the copy is so furnished, interest shall become payable after the expiry of Period of ninety days from the date of such supply of copy of order.

Time Limit For Application: -

The said dealer may apply to commissioner at any time after the end of said succeeding year to which refund relates, provided where any return has been filled at any time after date prescribed for filing the last return of the said year then refund shall be granted within 18 months of date of filing of such belated return.

Procedure For Filing Form 501: -

The template of new form 501 available on the web www.mahavat.gov.in at DOWNLODES-FORMS-FORM 501. The said template is in the form of an Excel Work Book. The dealer should download it and fill offline data entry.

Form 501: -

To claim a refund under MVAT Act dealer has to fill the Form 501 which is available on department’s website. As Per the Trade Circular No. 28T of 2009, dated 15.10.2009, it has been made mandatory for all the dealers, who desire to file refund application in Form 501 as per section 51 to file Form 50 electronically only.

Time Limit For Filing 501: -

The Filling shall be done within stipulated time limit of 18 months from the end of the financial year to which refund claim relates.

Guide to fill Form 501: -

The Form 501 is consist of four excel sheets namely Annexure A, B, C, & D.

Afterwards dealer has to furnish weather he is willing to furnish bank guarantee. If yes then under this scheme, the dealer can claim refund before refund audit. Henceforth, procedure for the same is hereunder: -

a) Legal provision: - as per provision of section 51(3)/b of the MVAT Act, 2002. Bank guarantee can be obtained from a dealer before granting refund. In case, the applicant dealer furnishes the bank guarantee, then the refund shall be granted within one month.

b) Bank:- Bank guarantee should be form any branch of a bank notified as a government treasury

c) Period: - Bank guarantee can be obtained for a maximum period of 36 months.

d) Amount: - Following parameters will be applied to the dealers willing to submit bank guarantee for refund.

To read the full article: Click Here

CAclubindia

CAclubindia