Background on sustainability reporting

In 1987, the World Commission on Environment and Development set out an aspirational goal of sustainable development - describing it as "development which meets the needs of the present without compromising the ability of future generations to meet their own needs.' Through their activities and relationships, all organizations make positive and negative contributions toward the goal of sustainable development. Organizations therefore have a key role to play in achieving this goal.

Sustainability reporting is an organization's practice of reporting publicly on its economic, environmental, and social impacts, and hence its contributions - positive or negative -towards the goal of sustainable development. Sustainability reporting has become a mainstream business practice. Almost three-quarters of N100 companies now report on corporate responsibility, according to KPMG's 2015 Survey of Corporate Responsibility Reporting. Of the world's largest companies - the G250 - 92% produce sustainability reports, with 74% of these referring to the GRI Guidelines or Standards.

Globally-accepted standards, such as the GRI Sustainability Reporting Standards, provide a common language and credible set of disclosures for organizations to communicate about their impacts on the economy, the environment, and society.

Organizations can combine their use of such instruments to improve the quality and comparability of information they report publicly. This information enables better decision making by organizations and their stakeholders, helping to build the long-term trust that is essential for the functioning of markets.

A sustainability report is a report published by a company or organization about the economic, environmental and social impacts caused by its everyday activities. A sustainability report also presents the organization's values and governance model, and demonstrates the link between its strategy and its commitment to a sustainable global economy.

Sustainability reporting can help organizations to measure, understand and communicate their economic, environmental, social and governance performance, and then set goals, and manage change more effectively. A sustainability report is the key platform for communicating sustainability performance and impacts - whether positive or negative.

Sustainability reporting can be considered as synonymous with other terms for non-financial reporting; triple bottom line reporting, corporate social responsibility (CSR) reporting, and more. It is also an intrinsic element of integrated reporting; a more recent development that combines the analysis of financial and non-financial performance.

Sustainability reports are released by companies and organizations of all types, sizes and sectors, from every corner of the world.

Thousands of companies across all sectors have published reports that reference GRI's Sustainability Reporting Guidelines. Public authorities and non-profits are also big reporters. GRI's Sustainability Disclosure Database features all known GRI-based reports.

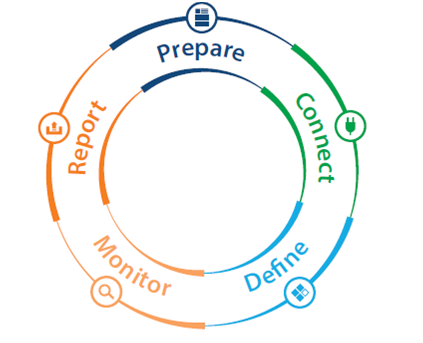

Model for Reporting Process

Major providers of sustainability reporting guidance include:

• GRI (GRI's Sustainability Reporting Standards)

• The Organisation for Economic Co-operation and Development (OECD Guidelines for Multinational Enterprises)

• The United Nations Global Compact (the Communication on Progress)

• The International Organization for Standardization (ISO 26000, International Standard for social responsibility)

Sustainability reporting is carried out by companies and organizations of all types, sizes and sectors. Of the world's largest 250 corporation, 93% report on their sustainability performance and 82% of these use GRI's Standards to do so. The GRI Sustainability Disclosure Database is a collection of all sustainability reports of which GRI is aware, and is available to all members of the public.

Internal benefits for companies and organizations can include:

• Increased understanding of risks and opportunities

• Emphasizing the link between financial and non-financial performance

• Influencing long term management strategy and policy, and business plans

• Streamlining processes, reducing costs and improving efficiency

• Benchmarking and assessing sustainability performance with respect to laws, norms, codes, performance standards, and voluntary initiatives

• Avoiding being implicated in publicized environmental, social and governance failures

• Comparing performance internally, and between organizations and sectors

External benefits of sustainability reporting can include:

• Mitigating - or reversing - negative environmental, social and governance impacts

• Improving reputation and brand loyalty

• Enabling external stakeholders to understand the organization's true value, and tangible and intangible assets

• Demonstrating how the organization influences, and is influenced by, expectations about sustainable development

GRI is an international, independent organization that helps businesses, governments and other organizations understand and communicate the impact of business on critical sustainability issues such as climate change, human rights, corruption and many others.

GRI produce the world's most trusted and widely used standards for sustainability reporting, the GRI Standards, which enable organizations to measure and understand their most critical impacts on the environment, society and the economy. Thousands of reporters in over 90 countries use GRI's Standards - a free public good - for their reporting.

GRI have strategic partnerships with international organizations including the OECD, the UN Global Compact, UNEP, and ISO. We advise governments, stock exchanges and market regulators in their policy development to help create a more conducive environment for sustainability reporting. In addition GRI collaborate with organizations in and outside of the reporting field to innovate new technologies and solutions, with the overall aim of embedding sustainability reporting into the decision-making process of organizations around the world.

GRI's Secretariat is located in Amsterdam, the Netherlands, with Regional Hubs in Africa, China, North America, Oceania, Latin America, South Asia and South East Asia.

These Regional Hubs advance reporting at the country level, respond to the needs of local stakeholders, build capacity and value, and encourage the flow of knowledge and participation from the regions into GRI's global network and activity.

Sustainable Reporting in India

Ministry of Corporate Affairs, Government of India, in July 2011, came out with the 'National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business'. These guidelines contain comprehensive principles to be adopted by companies as part of their business practices and a structured business responsibility reporting format requiring certain specified disclosures, demonstrating the steps taken by companies to implement the said principles. SEBI had introduced requirements with respect to BRR vide circular No. CIR/CFD/DIL/8/2012 dated August 13, 2012.

Ministry of Corporate Affairs, Government of India, in July 2011, came out with the 'National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business'. These guidelines contain comprehensive principles to be adopted by companies as part of their business practices and a structured business responsibility reporting format requiring certain specified disclosures, demonstrating the steps taken by companies to implement the said principles.

In line with the above Guidelines and considering the larger interest of public disclosure regarding steps taken by listed entities from a Environmental, Social and Governance ("ESG”) perspective, it has been decided to mandate inclusion of Business Responsibility Reports ("BR reports”) as part of the Annual Reports for listed entities. Therefore, in line with the objective to enhance the quality of disclosures made by listed entities, certain listing conditions are hereby specified by way of inserting Clause 55 in the equity Listing Agreement as given in Annexure-1.

Pursuant to notification of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 ("Listing Regulations”), the aforesaid circular dated August 13, 2012 was rescinded. As per clause (f) of sub regulation (2) of regulation 34 of Listing Regulations, the annual report shall contain a business responsibility report(BRR)describing the initiatives taken by the listed entity from an environmental, social and governance perspective, in the format as specified by the Board. Accordingly, listed entities shall be guided by the format as per Annexure I.

Annexure I -Suggested Format for Business Responsibility Report

It consist of various details which are divided in 6 sections as under :

- Section A: General information about the company

- Section B: Financial details of the company

- Section C: Other details

- Section D: Business Responsibility information

- Section E: Principle-wise performance

Certain key principles to assess the fulfillment of listed entities and a description of the core elements under these principles are detailed at Annexure II.

Annexure II - Principles to assess compliance with environmental, Social and governance norms

Applicability

The requirement to include BR Reports as part of the Annual Reports shall be mandatory for top 100 listed entities based on market capitalisation at BSE and NSE as on March 31, 2012. BSE and NSE shall independently draw up a list of listed entities to whom the circular would be applicable based on the said criteria and disseminate the same in their websites respectively. Other listed entities may voluntarily disclose BR Reports as part of their Annual Reports.

Those listed entities which have been submitting sustainability reports to overseas regulatory agencies/stakeholders based on internationally accepted reporting frameworks need not prepare a separate report for the purpose of these guidelines but only furnish the same to their stakeholders along with the details of the framework under which their BR Report has been prepared and a mapping of the principles contained in these guidelines to the disclosures made in their sustainability reports.

Linking GRI standards with BRR Framework

The GRI Standards relate to many other reporting frameworks and sustainability initiatives. GRI's linkage documents are designed to highlight these connections and enable organizations to fulfil multiple reporting requirements. This linkage document is designed to show companies how requirements under the SEBI BRR Framework correspond to the GRI Standards and disclosures. The linkage table shows the GRI Standards and disclosures that relate to each requirement in the SEBI BRR Framework. This linkage document by jointly released by GRI and BSE on 14th February 2017. The information collected for these disclosures allows companies to create a sustainability report based on the GRI Standards at the same time as complying with the SEBI BRR Framework, without duplicating effort.

Note that the disclosures in the GRI Standards can have additional reporting requirements, recommendations, and/or guidance that relate to each disclosure. In order to claim that a sustainability report has been prepared in accordance with the GRI Standards, an organization is required to comply with all requirements that relate to the disclosures reported. See GRI 101: Foundation for more information.

By making use of both the GRI Standards and the SEBI BRR Framework, a company can meet the growing demand for sustainability information, and be more transparent and accountable to its stakeholders, thereby increasing trust.

CMAs being having Techno commercial background can help organisations to achieve Sustainability. There is ample of scope to assist corporates for growing reporting requirements not limiting to financials but non financials reporting like Sustainable reporting. The business needs to look at the Business Model from all point of views of different stakeholders.

References :

- https://www.globalreporting.org

- Ready to Report ? - publication by GRI

- Linking the GRI Standards and the SEBI BRR Framework , Linkage document

- SEBI Notifications on BRR

CAclubindia

CAclubindia