Financial Reporting (CA Final - Old Course)

Analysis of Financial Reporting Old syllabus by CA Sumit Sarda:

The paper has been lengthy and compared to the previous 2 attempts has been difficult. This time ICAI asked questions in which concepts related to 2 different questions were merged together

Weightage

1. Accounting Standards, Guidance notes and Financial Instruments: 64 marks

After a long time, ICAI asked questions on related party disclosures and Operating segments, which were relatively simple. Overall questions were not difficult and students could easily score there marks

2. Ind AS: 8 marks

Question was theory based and easy to answer on the basis of differences studied by students

3.Amalgamation: 16 marks

Question on cross-holding, though unexpected but question had no adjustments and easy to solve for those who had studied cross holding

4.Consolidation: 16 marks

Question on a different financial year ending date was asked, similar questions in ICAI module were even more difficult than asked in the exam, but there seem to be some typing error related to cash adjustments in the question

5. Valuation: 8 marks

Market valuation question was easy to solve but too lengthy and deserved more marks

6. Other chapters: 20 marks

Questions on VAS, Mutual fund, NBFC and CSR, directly from the book asked questions

Click hereto download CA Final Financial Reporting (FR) Old Course May 2019 Question Paper

To enroll for FR Fast Track (CA Final) subject of the author: Click here

Strategic Financial Management (CA Final - Old Course)

Analysis of Strategic Financial Management paper by Prof. Rahul Malkan:

- Mix of Some very new and some repeat questions

- Was Calculative and lengthy as compared to previous 2 attempts

- Mostly all questions were based on fundamental concepts

- Overall lengthy -but exemption was on the table

|

Q. No |

Chapter |

Marks |

Comments |

|

|

Q.1 |

A |

Economic Value Added |

8 Marks |

New Question - Medium Level |

|

B |

Equity Valuation |

8 Marks |

Similar - Easy |

|

|

C |

National Pension Scheme |

4 Marks |

Theory |

|

|

Q.2 |

A |

Mergers |

8 Marks |

Similar - Easy |

|

B |

Equity |

8 Marks |

New - Medium |

|

|

C |

VAR |

4 Marks |

Theory - From SM |

|

|

Q.3 |

A |

Portfolio |

8 Marks |

Similar - Medium |

|

B |

Options - Derivatives |

8 Marks |

Repeat - Easy |

|

|

C |

Securitization |

4 Marks |

Theory - From SM |

|

|

Q.4 |

A |

Mutual Funds |

8 Marks |

Repeat - Easy - Lengthy |

|

B |

Equity |

8 Marks |

Repeat - Easy |

|

|

C |

Start up finance |

4 Marks |

Theory - From SM |

|

|

Q.5 |

A |

Futures - Derivatives |

8 Marks |

New - Easy |

|

B |

Forex |

8 Marks |

New - Medium |

|

|

C |

SME |

4 Marks |

Theory |

|

|

Q.6 |

A |

Forex / Derivative Hedging |

8 Marks |

Similar - Easy |

|

B |

Forex |

8 Marks |

New - Difficult |

|

|

C |

IFC |

4 Marks |

Theory |

|

Note :

Question 1 - Compulsory

Question 2 to 6 - Any 4 questions

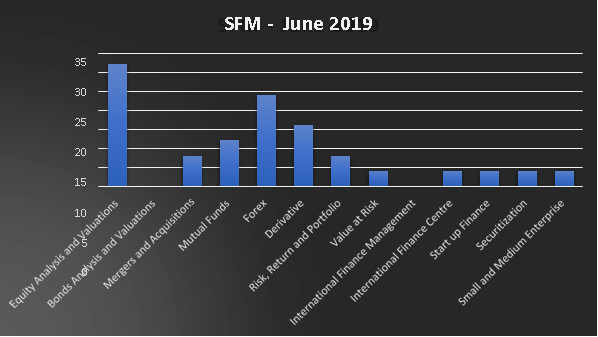

Chapter wise Marks Distribution

|

Sr No |

Chapter |

Marks |

|

1 |

Equity Analysis and Valuations |

32 Marks |

|

2 |

Bonds Analysis and Valuations |

Nil |

|

3 |

Mergers and Acquisitions |

8 Marks |

|

4 |

Mutual Funds |

12 Marks |

|

5 |

Forex |

24 Marks |

|

6 |

Derivative |

16 Marks |

|

7 |

Risk, Return and Portfolio |

8 Marks |

|

8 |

Value at Risk |

4 Marks |

|

9 |

International Finance Management |

Nil |

|

10 |

International Finance Centre |

4 Marks |

|

11 |

Start up Finance |

4 Marks |

|

12 |

Securitization |

4 Marks |

|

13 |

Small and Medium Enterprise |

4 Marks |

Click hereto download CA Final Strategic Financial Management (SFM) Paper Old Course May 2019

To enroll Strategic Financial Management (CA Final) subject of the author: Click here

Advanced Auditing & Professional Ethics (CA Final - Old Course)

Analysis of Audit Paper by CA Ravi Taori

INDEPTH SOURCE & COVERAGE ANALYSIS MAY 19 CA FINAL AUDIT (OLD SYLLABUS)

Hello everyone! As a professor it's very important to understand what material is being used for drafting papers, understand the trend so that I can make students hit bulls eye. So we worked for many hours to give you accurate and path breaking analysis. So this time ICAI has drafted much easier paper. Majority of the questions were either from the PM or the recent past papers or the MTPs/RTPs.

You will be surprised to see many of below facts. (Paper was of 118 marks of which 30 were covered by MCQs, So he have around 88 Marks descriptive questions)

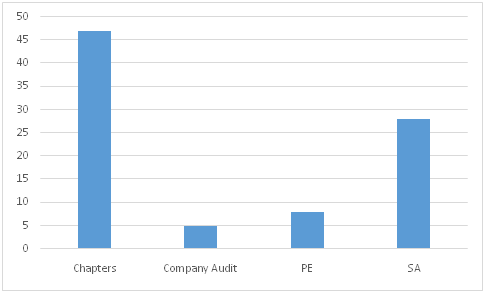

Coverage of Various Topics

1. Standards on Auditing covered 28 Marks. (32%)

2. Professional Ethics covered merely 8 Marks. (10%)

3. Company Audit covered just 5 Marks. (5%)

4. Other Chapters had the majority weightage of around 47 Marks. (53%)

Source of Paper

(Don't add up below marks there is overlapping of the source)

1. PM contributed to 31 Marks of the paper. (35%)

2. If we consider the recent past papers, it contributes around 40 Marks. (45%, 5 Years)

3. Considering the MTPs/RTPs, they contribute to around 33 Marks of the paper.(38%, 2 Years)

4. Around 34 Marks of the paper constituted of new questions which were not covered in the PM, Past papers or MTPs/RTPs. Such questions required conceptual clarity. Therefore, it is very important for the students to understand that depending solely on the question bank would not suffice.(39%)

5. Considering the Tax Audit Area, ICAI targeted the GST Audit area which covered 10 Marks. There were no questions on the Income Tax Audit.

6. SA 500 series held a lot of importance in this paper. It carried around 23 marks.

Strategy

1. Solely relying on Company Audit & PE was not a wise decision considering the current paper.(Only 13 marks in descriptive)

2. Descriptive & MCQs combined coverage of SAs is also good, its worth to spend more time on them.

3. There were some direct questions asked from the other chapters & hence was the easy scoring area.

4. Because of whooping 30 marks MCQs, importance conceptual clarity and coverage all concepts hasincreased many fold.

Curious Questions

Q2(c) - Question on Insolvency Professional was covered in Nov 18 RTP , It is allowed to use Insolvency Professional as it is title recognised by central government.

Q4(a) - Question on relative holding shares, Limit of 1,00,000 is for all relatives taken together. Daughter & her Husband are covered in definition of relative. Holding was reduced to zero after correction time was over. So auditor stands disqualified. Market Value is to be ignored.

Q4(c)-- This answer originally when provided by ICAI in suggested of NOV 18 (New) was not correct but later on Board of Studies changed the answer after discussion with the us.

Ultimate authority on consolidation is AS / Ind AS as prescribed by law and if they give some exemption it should be followed. If out of exemption some subsidiaries are not consolidated, then list should be disclosed in notes to accounts with reason.

ANALYSIS ON THE BASIS OF MARKS DISTRIBUTION:

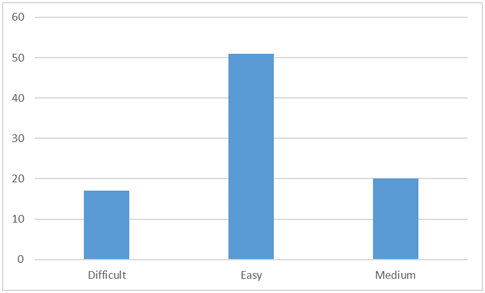

ANALYSIS ON THE BASIS OF DIFFICULTY:

To enroll CA Final Audit (Old Syllabus) subject of the author: Click here

To view / download CA Final Audit - Old Syllabus Question Paper - May'19: Click here

To view / download Suggested answers of CA Final Audit (Old) Syllabus - May'19: /Click here

Correction of Suggested Answer of CA Final Audit - Old Course May 19 Exams by CA Ravi Taori

Stay tuned to check the analysis of the other subjects.

CAclubindia

CAclubindia