Points to be noted:

1. Nil amount of return is not required to be filed as clarified by ICSI in it's webinar dated 17th June 2019.

2. Audited financial statements for the FY 2018-19 is not required.

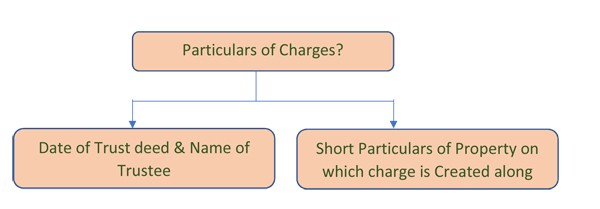

3. Copy of trust deed - Mandatory if company has trust deed and details of same are mentioned in the form.

4. Copy of instrument creating charge - Mandatory if company has trust deed and details of same are mentioned in the form.

5. List of depositors - List of deposits matured, cheques issued but not yet cleared to be shown separately - Mandatory if company has balance of deposits outstanding at the end of the year.

Amount to be considered as Deposits:

Accordingly, Rule 2(1)(c) of Companies (Acceptance of Deposit) Rules, 2014, excludes the following amount received by a Company from the ambit of Deposit and shall not be considered as deposits -

i. any amount received from the Central Government or a State Government or local authority or statutory authority, or any amount Whose repayment is guaranteed by the Central Government or a State Government;

ii. Any amount received from foreign Governments, foreign or international banks, foreign body corporates and foreign citizens, foreign authorities or persons resident outside India;

iii. Loans or facility from banks;

iv. Loans from Public Financial Institutions/ Insurance Companies;

v. any amount received against issue of commercial paper or any other instruments;

vi. Any amount received by a company from any other company;

vii. Any amount received through Public offer. However, if securities not allotted within 60 days and refund not made within 15 days then such amount will be treated as Deposit;

viii. Any amount received from the director of the company and in case of private company also from the relative of the director of the company subject to the condition that the amount has been given from own's fund and not from borrowings.

ix. Any amount raised by the issue of bonds or debentures secured by a first charge or a charge ranking pari passu with the first charge, compulsorily convertible within 10 years;

x. Any amount raised by issue of Unsecured Non-convertible debentures;

xi. Non-interest-bearing security deposit from employee of the company under the contract of employment to the extent not exceeding his annual salary;

xii. Any non-interest-bearing amount received and held in trust;

xiii. Any amount received in the course of business -

(a) As advance for supply of good or services provided that such goods or services are supplied within 365 days of the receipt of advance

(b) As advance in connection with consideration for an immovable property provided such advance is adjusted against such property in accordance with the terms of the agreement;

(c) As security deposit for the performance of the contract;

(d) As advance under long term projects for supply of capital goods;

Provided that if the amount received under (a), (b) & (d) becomes refundable due to lack of necessary permission or approval to deal in the concerned goods or services, then the amount received shall be deemed as deposit on the expiry of 15 days from the date they become due for refund.

(e) As advance towards consideration for future warranty or maintenance contract;

(f) As advance received which is allowed by any sectoral regulator?

(g) As advance for subscription towards publication;

xiv. Any amount of unsecured loan brought in by the promoter's subject to the fulfillment of the following conditions:

(a) The loan is brought in pursuance of the stipulation imposed by the lending institutions on the promoters to contribute such finance;

(b) The loan is provided by the promoters themselves or by their relatives or by both; and

(c) The exemption under this sub-clause shall be available only till the loans of financial institution or bank are repaid and not thereafter;

xv. Any amount accepted by a Nidhi Company;

xvi. Any amount received by way of subscription in respect of a chit under the Chit Fund Act, 1982;

xvii. Any amount received by the company under any collective investment scheme;

xviii. An amount of 25 lakh rupees or more received by a start-up company, by way of a convertible note (convertible into equity shares or repayable within a period not exceeding five years from the date of issue) in a single tranche, from a person;

xix. Any amount received by a company from registered Alternate Investment Funds, Domestic Venture Capital Funds, Infrastructure Investment Trusts and Mutual Funds.

CAclubindia

CAclubindia